How Julius Baer Mixes Quantitative Investment Strategies

Related to multiple strategies, mainly to Carry, Volatility Selling and Trend-Following strategies …

Authors: Sepp

Title: Diversifying Cyclicality Risk of Quantitative Investment Strategies (Presentation Slides)

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2980708

Abstract:

What is the most significant contributing factor to the performance of a quantitative fund: its signal generators or its risk allocators? Can we still succeed if we have good signal generators but poor risk management?

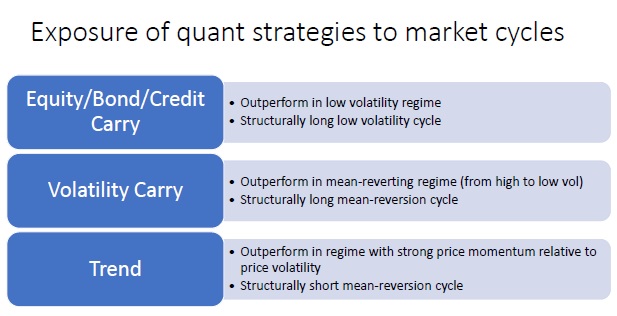

We consider the risk of the skewness and the cyclicality of the key quantitative strategies:

1. Carry strategies

2. Volatility strategies

3. Trend-following strategies

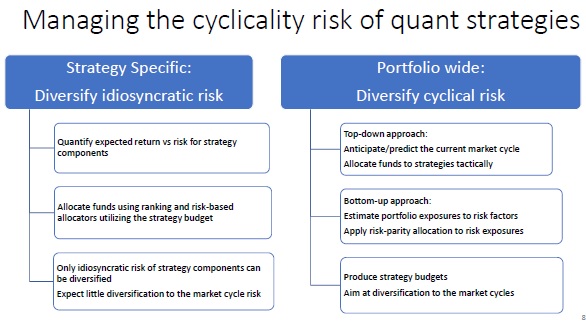

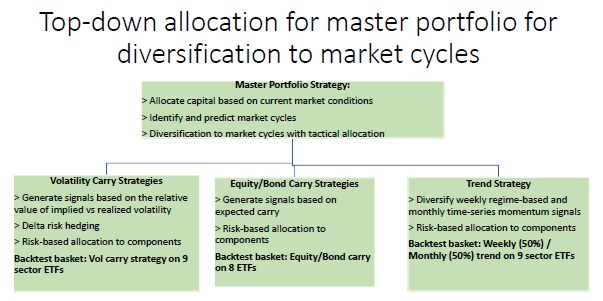

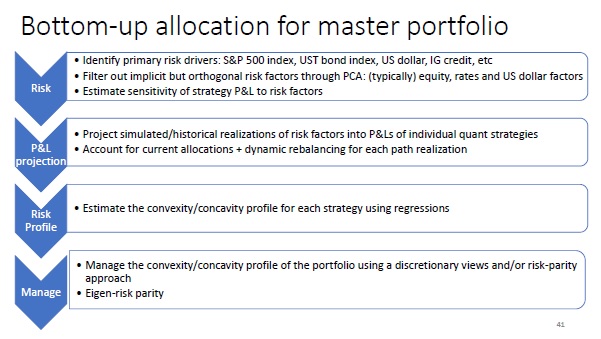

We then present the two approaches for diversification of the cyclicality risk for a master portfolio of these strategies using:

1. Top-down allocation

2. Bottom-up allocation

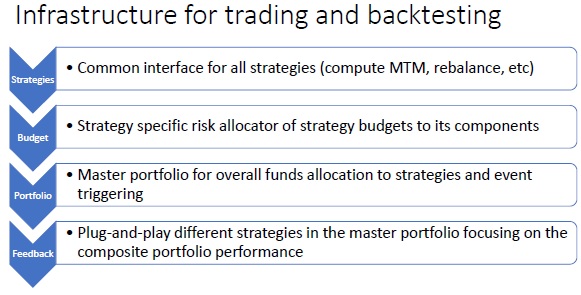

We illustrate a few examples using back-tested data using systematic quantitative strategies with risk-based allocators.

Notable quotations from the academic research paper:

"

"

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend