Impact of 1987 Black Monday on Trading Behavior of Stock Investors

Explanatory research paper for all short term contrarian strategies:

Title: Black Monday, Globalization and Trading Behavior of Stock Investors

Author: Kim

Link: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2798536

Abstract:

Using a simple sign test, we report new empirical evidence, taken from both the US and the German stock markets, showing that trading behavior substantially changed around Black Monday in 1987. It turned out that before Black Monday investors behaved more as in the momentum strategy; and after Black Monday more as in the contrarian strategy. We argue that crashes, in general, themselves are merely a manifestation of uncertainty on stock markets and the high uncertainty due to globalization is mainly responsible for this change.

Notable quotations from the academic research paper:

"Research question:

The paper tests whether systematic trading behaviors on stock markets have changed over the long-term. In doing so, the two different trading strategies, momentum and contrarian, serve as the systematic trading strategies. For the empirical part, the daily returns of two sets of stock market data (Deutscher Aktienindex and Dow Jones Index) since 1959 are used. The focus of the analysis is on the distributional property of increases and decreases in returns, especially sequences of the sign. The empirical probability of sequences of the sign is tested by the theoretical distribution resulting from the assumption of the martingale process of return series implying absence of systematic trading strategies.

Results:

The empirical results show that the probabilities of sequences of the same sign (both positive and negative) before Black Monday are significantly higher than those of the theoretical distribution. This means that the investors preferred the momentum strategy. After Black Monday, however, the probabilities of sequences of the same sign are significantly lower than those of theoretical distribution. This means that the investors are tending to trade according to the contrarian strategy.

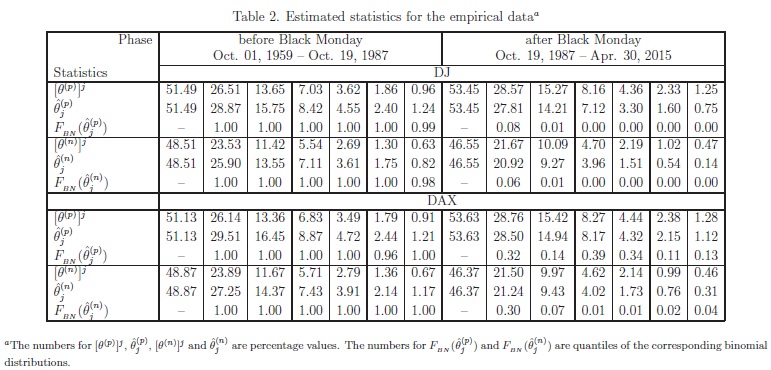

Table 2 shows the following:

• Results for the DJ

– Before Black Monday, the empirical probabilities of sequences of the same sign for both the positive and negative signs (as given in the second and fifth rows of the first block in the upper panel) are significantly higher than those of the theoretical values (as given in the first and fourth rows of the first block in the upper panel) for all six cases (i.e. two-day to seven-day sequences) for both the DJ and the DAX. The percentage values of the cumulative binomial distribution, evaluated at the number of the corresponding sequences, are equal to or higher than 99% except in one case, namely the seven-day negative sequence (98%).

– After Black Monday, the empirical probabilities of sequences of the same sign for both the positive and negative signs (as given in the second and fifth rows of the second block in the upper panel) are significantly lower than those of the theoretical values (as given in the first and fourth rows of the first block in the upper panel) for all six cases (i.e. two-day to seven-day sequences). The percentage values of the cumulative binomial distribution, evaluated at the number of the corresponding sequences, are equal to or lower than 1% except in two cases, namely the one-day positive sequence (8%) and the oneday negative sequence (6%).

• Results for the DAX

– Before Black Monday, the results for the DAX are almost the same as those of the DJ up to a small difference (no meaning to the main results) in the six-day positive sequence and seven-day negative sequence.

– After Black Monday, the empirical numbers of sequences of the same sign for both the positive and negative signs (as given in the second and fifth rows of the second block in the lower panel) are smaller than those of the theoretical values (as given in the first and fourth rows of the first block in the lower panel). The empirical probabilities in terms of the p-values for the positive sign sequences are weaker than the DJ with a range of significance level from 11% to 39%. The negative sign sequences are still highly significant up to the one-day negative sequence (30%).

From these empirical results, we could draw the conclusion that Black Monday has changed trading behavior on stock markets. Before Black Monday, investors tended to buy when the stock return was positive and to sell when the stock return was negative (a day-to-day momentum strategy) while after Black Monday they tended to buy when the stock return was negative and to sell when the stock return was positive (a day-to-day contrarian strategy)."

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend