Implied Equity Duration as a Measure of Pandemic Shutdown Risk

Some companies have relatively more of their value in near-term cash flow (for ex. General Motors Corporation). Others (for ex. Tesla), are growth stocks, with a greater proportion of their market value based on long-term expected future cash flow. It seems that coronavirus pandemic has hit mainly the first group, the “low equity duration” companies. A new academic research paper written by Dechow, Erhard, Sloan, and Soliman explains how the equity duration factor can be used to assess how are companies exposed to short-term unexpected macroeconomic events (like COVID-19 pandemic), and how equity duration sensitivity can also explain relative underperformance of value vs growth stocks during the last bear market.

Authors: Dechow, Patricia and Erhard, Ryan and Sloan, Richard G. and Soliman, Mark T.

Title: Implied Equity Duration: A Measure of Pandemic Shutdown Risk

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3623588

Abstract:

Implied equity duration was originally developed to analyze the sensitivity of equity prices to discount rate changes. We demonstrate that implied equity duration is also useful for analyzing the sensitivity of equity prices to pandemic shutdowns. Pandemic shutdowns primarily impact short-term cash flows and thus have a greater impact on low duration equities. We show that implied equity duration has a strong positive relation to US equity returns during the onset of the 2020 coronavirus lockdown. Our analysis also demonstrates that the underperformance of ‘value’ stocks during this period is a rational response to their lower durations.

Notable quotations from the academic research paper:

“Bond duration is a common summary measure of interest rate risk for fixed income securities. Dechow, Sloan, and Soliman (2004) adapt this measure to equity securities. They develop a simple algorithm for predicting the amount and timing of future cash flows and then apply the standard duration formula to compute a measure of implied equity duration. They show that their measure of implied equity duration provides an effective measure of discount rate risk in equity securities.

In this paper, we demonstrate that implied equity duration is also effective in measuring the risk of equity securities to unexpected macroeconomic events that disproportionately impact short run cash flows. Speci fically, if an unexpected event causes the near-term cash flows of fi rms to be severely curtailed but has relatively little impact on the longer-term cash flows, then stocks with most of their expected future cash flows concentrated in the near-term (i.e., lower duration equities) will suff er the greatest loss in value.

| What about Data? Look at Quantpedia’s Algo Trading Discounts. |

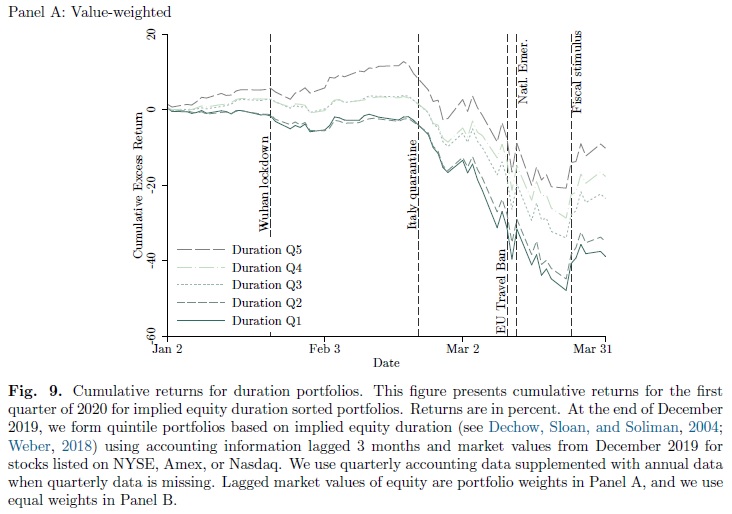

We examine the ability of implied equity duration to explain US stock price behavior during the onset of the pandemic and fi nd that it is e ffective in explaining both the magnitude and variability of equity returns. Over the three months between January 1, 2020 and March 31, 2020, we fi nd that the returns from a hedge portfolio going long in the highest duration quintile (stocks with cash flows further into the future) and short in the lowest duration quintile exceeds 36% (144% on an annualized basis). Low duration equities also exhibit higher risk in the form of both higher market betas and higher stock return volatility over this period.

We also extend our analysis to show how the concept of implied equity duration can explain the poor performance of `value’ strategies over this time period. The value strategies that we consider are based on trailing earnings-to-price ratios and trailing book-to-market ratios measured at the onset of the pandemic. Dechow, Sloan, and Soliman (2004) show that these ratios are negatively correlated with implied equity duration. In particular, stocks with high earnings-to-price ratios and high book-to-market ratios tend to be stocks for which earnings and cash flows are in secular decline. Consequently, a greater proportion of their value is represented by near-term cash flows. Consistent with this explanation, we fi nd that value stocks signi ficantly underperform the market between January 1, 2020 and March 31, 2020. An implication of our analysis is that if the pandemic plays out as expected, curtailing cash flows for the next 12 to 24 months, then value stocks should suff er relatively greater permanent losses in value.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend