Market Makers and Extreme Price Movements

Often, this blog provides novel research that may not include the straightforward trading strategy, yet it is an interesting insight for portfolio managers, risk managers, investors or traders. Novel research of Brogaard et al. (2020) examines the crucial role of market makers during extreme price movements. According to the authors and the past literature, there are two competing theories of how the extreme price movements end, and both are related to the market makers. It is the constrained liquidity provision theory and the strategic liquidity provision. This research tests and explains these competing theories, with findings that are in line with the strategic liquidity provision. The results can be found particularly interesting during extreme price movements because the paper has shown that firstly, liquidity providers scale back and only interfere later. Market makers utilize price pressures in stressful times in a profitable way, since they profit from subsequent reversals.

Authors: Jonathan Brogaard, Konstantin Sokolov and Jiang Zhang

Title: How do Extreme Price Movements End?

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3700218

Abstract:

We test competing theories on liquidity dynamics during extreme price movements (EPMs). Our findings indicate that market makers strategically allow for price pressures and earn compensation from pricing errors. As a result, liquidity provision intensifies towards the end of an average EPM. This goes counter to a widespread concern that market making constraints cause the deterioration of liquidity as EPMs develop. Finally, we demonstrate that limit order book dynamics during EPMs is in line with a socially beneficial equilibrium.

As usually, the paper includes many interesting figures and tables:

Notable quotations from the academic research paper:

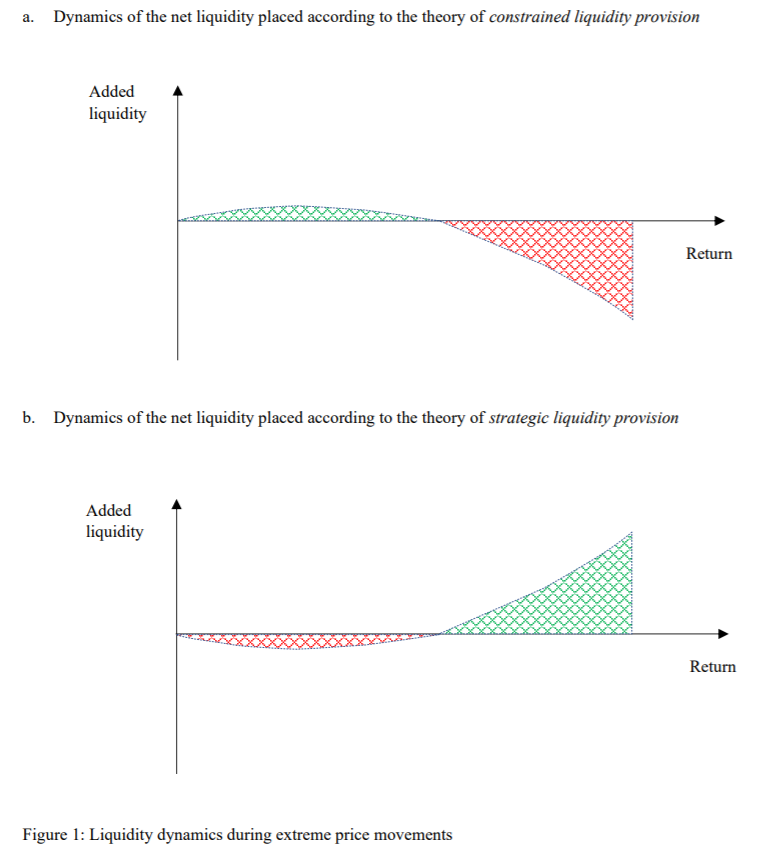

“There are two main theoretical frameworks of liquidity provision in stressful times. The first emphasizes the risks and constraints of market making (Amihud and Mendelson, 1980; Ho and Stoll, 1981; Madhavan and Sofianos, 1998; Kondor, 2009). According to this literature when liquidity demand spikes market makers’ inventory constraints bind and the market makers start canceling standing limit orders that are in the way of a price movement. There are two implications. First, more standing limit order depth is cancelled than placed in the direction of the EPM. Second, EPMs end when liquidity takers exhaust their demand, not because liquidity supply increases. We refer to this theory of literature provision as constrained liquidity provision. Figure 1.a illustrates the dynamics of the net limit order book depth according to the constrained liquidity provision theory.

The second theoretical framework suggests that market makers strategically allow for price pressures (Avramov, Chordia, and Goyal, 2006; Hendershott and Seasholes, 2007; Nagel 2012; Hendershott and Menkveld, 2014). According to this literature liquidity providers may be reluctant to replenish the limit order book caused by moderate liquidity demand. However, they are willing to intensify their participation during EPMs due to the higher expected compensation. The implications in this strand of literature differ from the first strand. First, more standing limit order depth is placed than cancelled in the opposite direction of the EPM. Second, EPMs end when liquidity suppliers step in and saturate the market. We refer to this theory of liquidity provision as strategic liquidity provision.

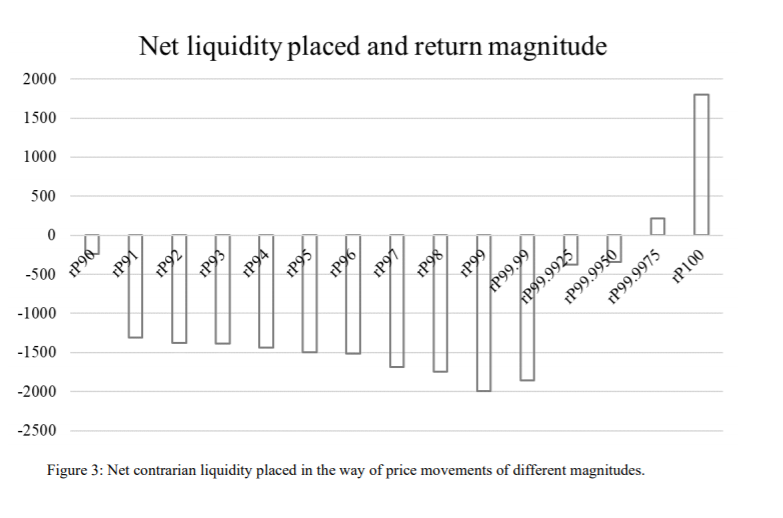

This paper analyzes limit order book depth dynamics around EPMs. We rely on the comprehensive TotalView-ITCH data covering all limit order placements, adjustments, and cancellations on NASDAQ. Following Brogaard et al. (2018), we sort all 10-second returns by magnitude and identify returns exceeding the 99.99th percentile as EPMs. We focus on the limit order placement and cancellation dynamics during such EPMs and find results supporting the strategic liquidity provision theory. Results indicate that liquidity providers scale back initially, but step in later and mitigate a typical EPM. The incentive to provide more liquidity during EPMs comes from the uninformed nature of liquidity demand that typically drives such events. This result is in line with the predictions of Nagel (2012) and Hendershott and Menkveld (2014), who suggest that liquidity providers allow for price pressures in stressful times and benefit from subsequent reversals. The findings suggest that modern market makers dynamically place limit orders consistently with the theory of strategic liquidity provision.

Strategic liquidity provision implies that market makers have incentives to cancel standing depth at the onset of EPMs and resume liquidity provision after the price significantly moves away from the fundamental value. According to Weill (2007), such strategy leads to a socially beneficial equilibrium, because liquidity providers are more likely to have enough resources to counteract EPMs. Empirically, this equilibrium suggests that the limit order depth is cancelled at the onset of an EPM and placed towards its end. This prevents the price from a free fall or surge.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend