Overview of Different Short Volatility Strategies

The expected return on the “variance factor” known as variance risk premium (VRP) is nothing new to options markets. For any investor interested in benefitting from this phenomenon, we present the study of Dörries et al. (2021), which provides a clear overview of different VRP-earning strategies.

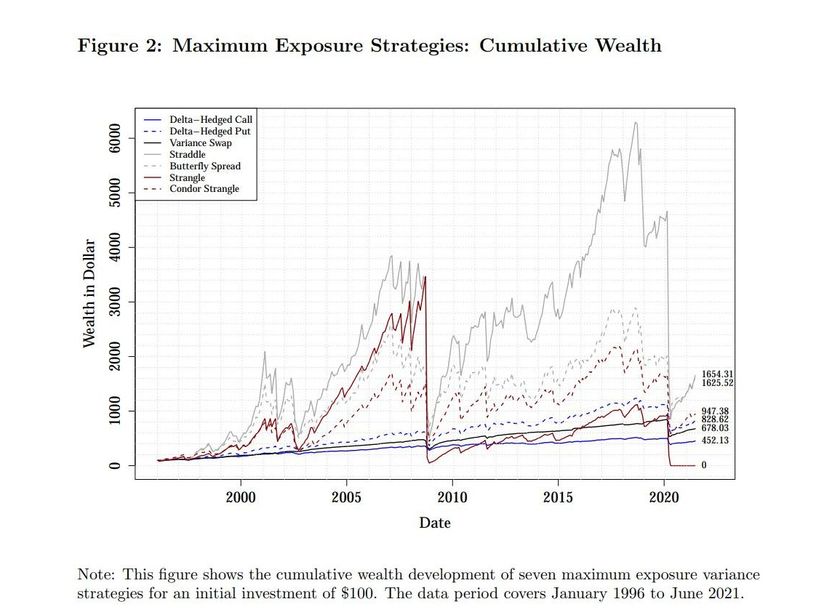

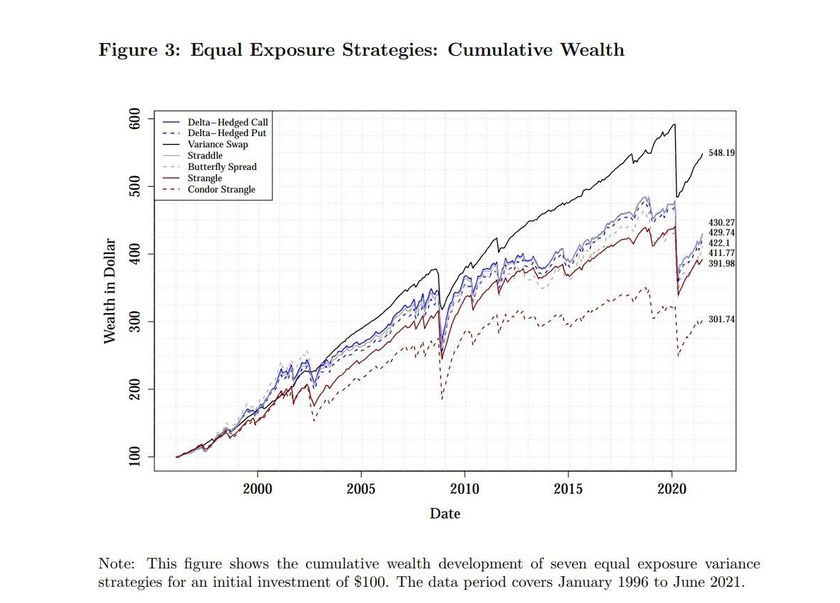

In their study, seven portfolios with potential to earn VRPs are created, namely straddle, strangle, butterfly spread, condor strangle, delta-hedged call, delta-hedged put, and variance swap. While designing long-term strategies, authors address three major problems. First, the payoff problem, i.e. what instruments to use to create suitable payoff profiles. Second, the leverage problem related to determining the right level of risk exposure. Finally, finite maturity problem associated with the choice of appropriate maturities of derivatives. Authors construct maximum and equal exposure strategies and then analyze their performance by using S&P 500 options with maturity of one month over the period from 1996 to 2021, covering the two most significant stock market crashes in past decades. Strategies are compared to each other as well as to other factor strategies.

To summarize the conclusions of present study: variance strategies differ greatly in some crucial aspects of risk and return, their correlation with the market is significantly positive, and unlike other factor strategies, they recover quickly from crashes and continue to earn premiums consistently.

Authors: Julian Dörries, Olaf Korn, Gabriel Power

Title: How Should the Long-term Investor Harvest Variance Risk Premiums?

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3989529

Abstract:

Derivatives strategies that aim to earn variance risk premiums are exposed to sharp price declines during market crises, calling into question their suitability for the long-term investor. Our paper defines, analyzes and proposes potential solutions to three problems (payoff, leverage and finite maturity) linked to designing suitable variance-based investment strategies. We conduct an empirical study of such strategies for the S&P 500 index options market, and find strong effects of certain design elements on risk and return. Overall, our results show that variance strategies can be attractive to the long-term investor if properly designed.

Notable quotations from the academic research paper:

Formally, the VRP is the deviation between the expected (physical) variance realized over the life of the option and the option implied (risk-neutral) variance.

Overall, we select seven portfolios: Straddle, strangle, butterfly spread, condor strangle, delta-hedged call, delta-hedged put, and variance swap. All offer convex payoff structures, so selling these portfolios has the potential to earn VRPs. We further target differences in their designs to get insights on trade-offs for variance exposure, downside risk, transaction costs, capital requirements, and margins.

We use data on European S&P 500 index options obtained from OptionMetrics IvyDB (U.S.). This database provides historical closing quotes from the CBOE, as well as implied volatilities (IV), interest rates, underlying spot prices, and implied dividend yields. Our sample period starts in January 1996 and ends in June 2021, covering 305 months.

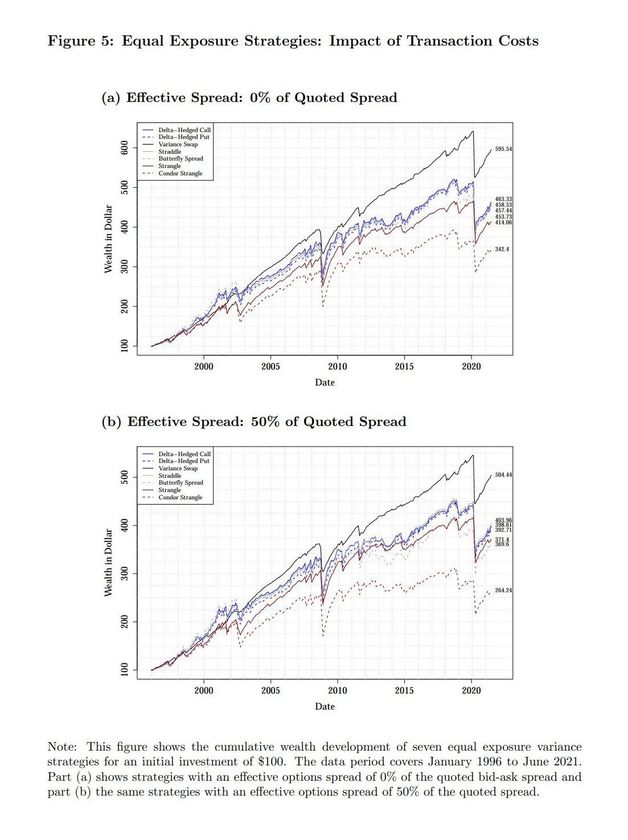

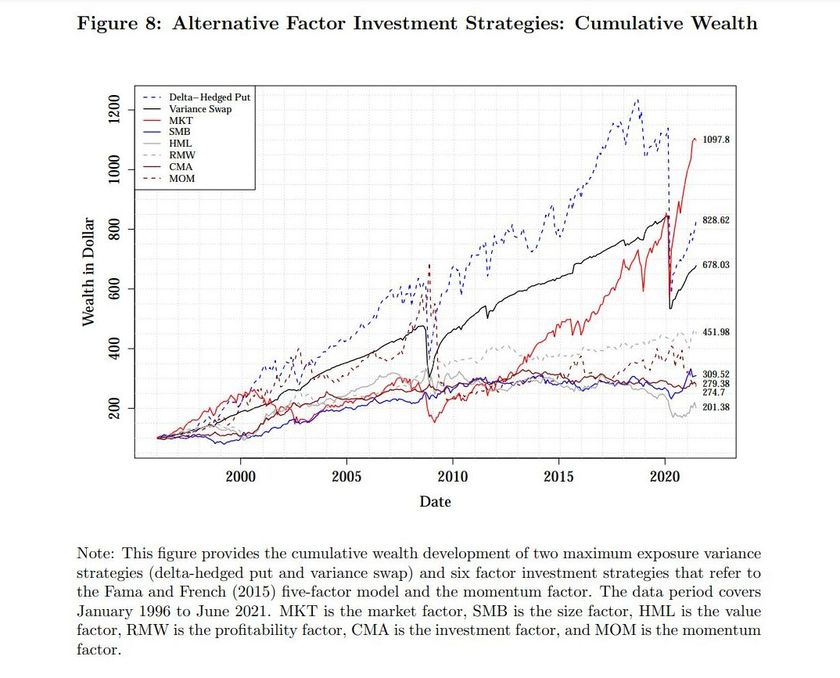

As we use approximately one-month maturity S&P 500 options and hold them until expiration, we have to open new positions every month. Positions are established every Monday after the third Friday of the month. We index each strategy to a level of 100 as of January 1996 and then determine the cumulative wealth level through the end of our data sample in June 2021.

We calculate the maximum possible exposure of trading strategies by levering the positions until the capital is fully used to buy long positions and provide margins on short positions. For equal exposure strategies, we lever the positions until each strategy has the same factor exposure. In each period, we select the strategy with the lowest gamma when it is fully levered under maximum exposure. All other strategies are then scaled down to this exposure and the remaining capital is invested risk-free.

Maximum exposure strategies differ greatly in terms of their return and risk profile. Some strategies exhibit risk levels that most investors would find excessive. Equal exposure strategies also differ from each other, but much less than maximum exposure strategies. Remaining differences are due to the different instruments on which the strategies are based, resulting in different payoff profiles and transaction costs.

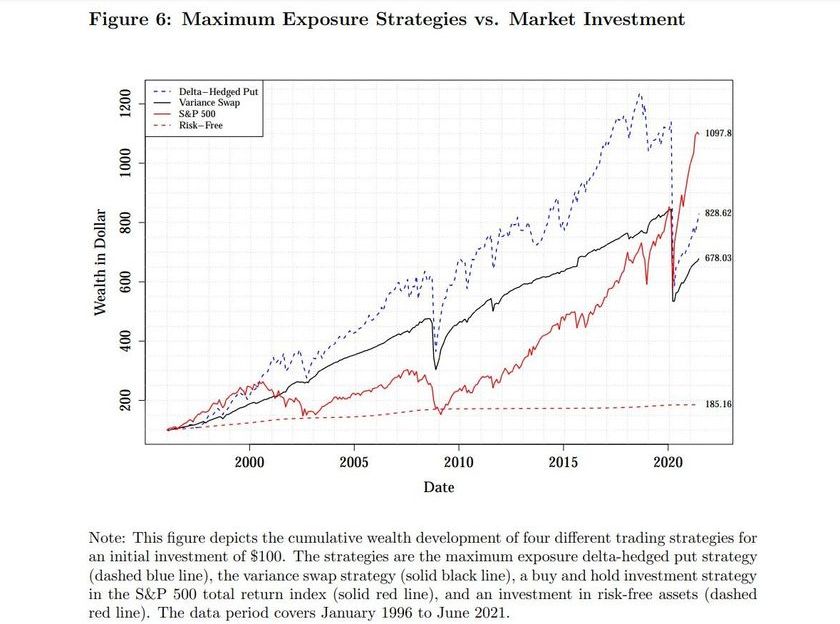

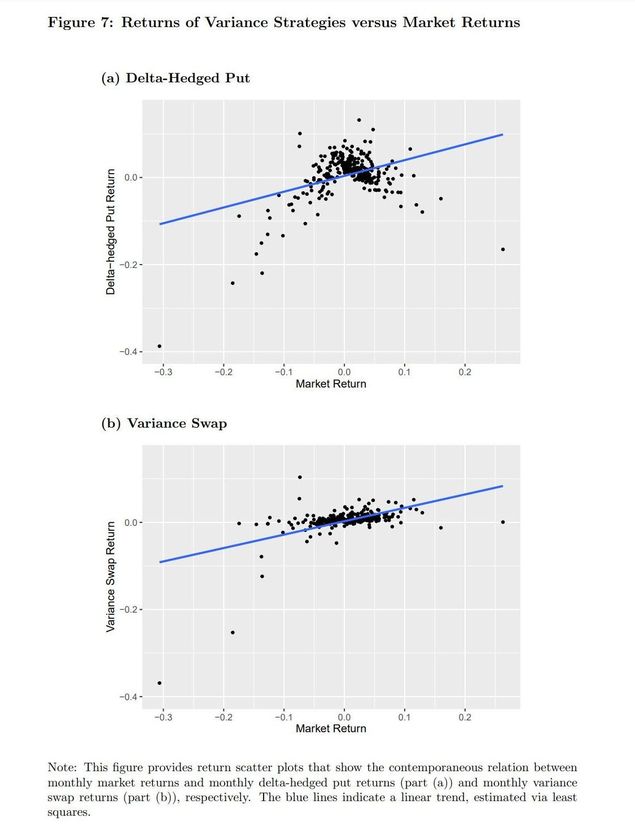

For all variance strategies, correlation with the market is significantly positive, but varies across strategies due to different payoff profiles.

Most of the time, the variance strategies generate a cumulative wealth above the wealth level of the market investment. What is more, the variance swap has lower downside risk than the market according to all measures except for maximum loss. While variance strategies do occasionally experience extreme losses, their magnitude is similar to the market’s. Moreover, variance strategies recover from previous losses relatively quickly, i.e., they generate strong upside movements in a fairly short period of time. This feature is especially clear after the 2008 financial crisis and after the low point of the Covid-19 pandemic.

Variance strategies consistently earn premiums throughout the whole sample period. This is in stark contrast with strategies based on the Fama-French (2015) factors or the momentum factor, which have not shown a significant upward trend since 2008.

Overall, the results suggest that variance strategies (including calendar option strategies) are attractive factor strategies for long-term investors. These strategies can provide valuable alternatives to a market investment, with a similar overall performance but clearly different downside risk characteristics. They can also be useful complements to a market investment by providing diversification benefits and significant alpha.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend