Hello all,

Let’s first very quickly recapitulate Quantpedia Premium development in the previous month: Ten new Quantpedia Premium strategies have been added to our database, and ten new related research papers have been included in existing Premium strategies during the last month. Additionally, we have produced 11 new backtests written in QuantConnect code. Our database currently contains over 440 strategies with out-of-sample backtests/codes.

And now, let’s move to our Quantpedia Pro subscription offering news.

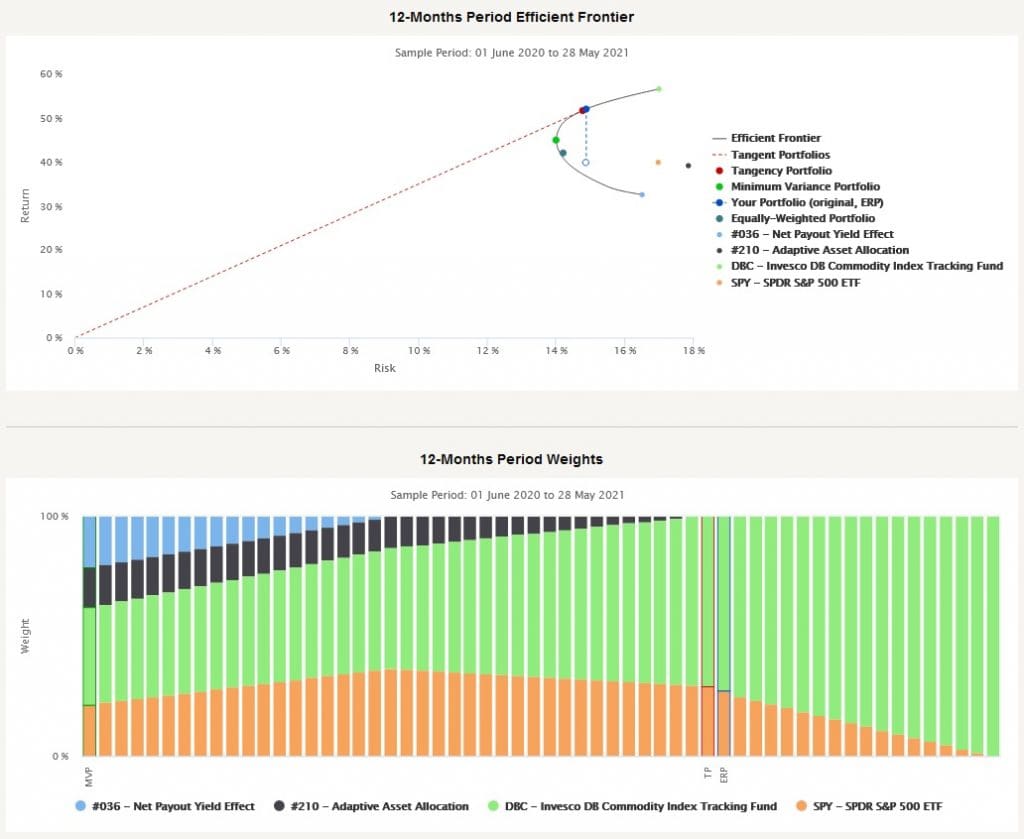

Our clients often mentioned one particular report as something they would love to see in the Quantpedia Pro – it’s the Markowitz Portfolio Optimization, and we are really happy that we can announce that it’s ready 🙂

What does it offer? It allows you to see classical risk vs. return charts that display how your selected Model Portfolio performs in comparison to other optimal portfolios built from the same individual components. You can review Tangency portfolio – the so-called optimal portfolio that realizes the highest possible Sharpe ratio, Minimum Variance portfolio – portfolio with the lowest risk and Maximum Return portfolio, the Efficient Frontier (a hyperbola representing portfolios with all the different combinations of assets that result into efficient portfolios), and Capital Market Line – that represents a portfolios of different combinations of a risk-free asset and a Tangency Portfolio. Additionally, our report shows portfolio weights along the Efficient Frontier.

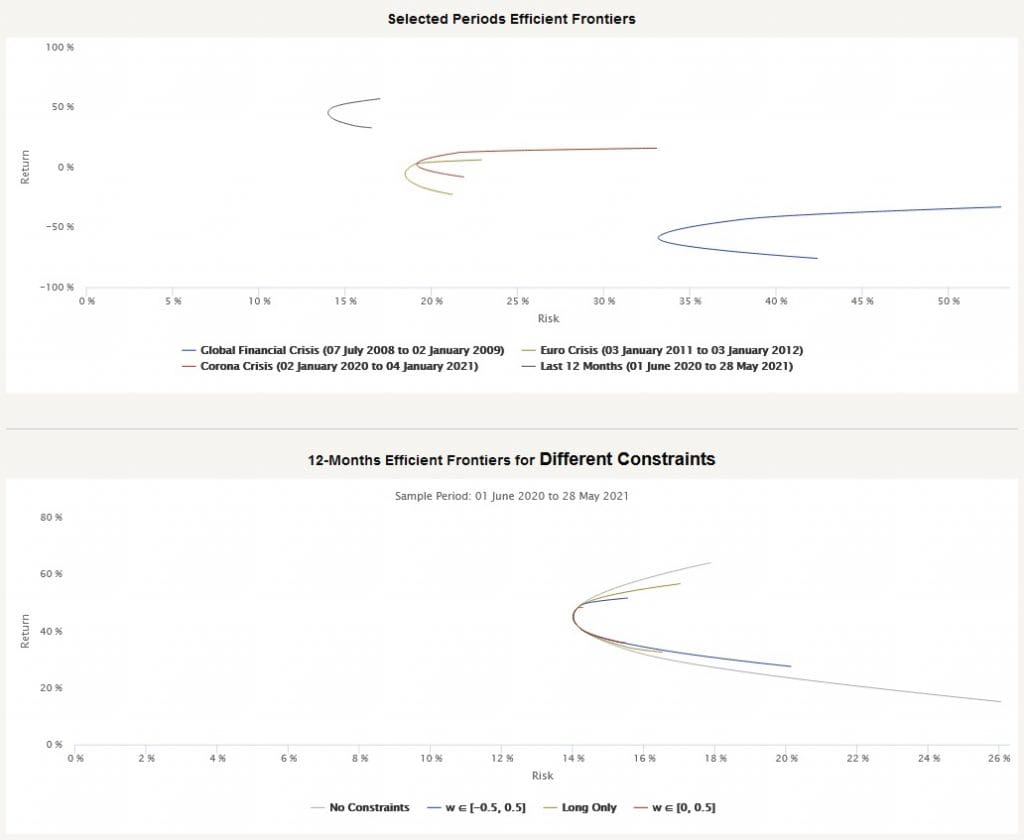

The Markowitz Portfolio Optimization report charts are displayed for various periods (actual 12-months period, the longest available period, and periods that contain various significant market drawdowns) and for various constraints (long-only portfolio, 0% to 50% weights, -50 to 50% weights and no constraints). We will again publish a short article about all of the math & methods behind this report in a few days.

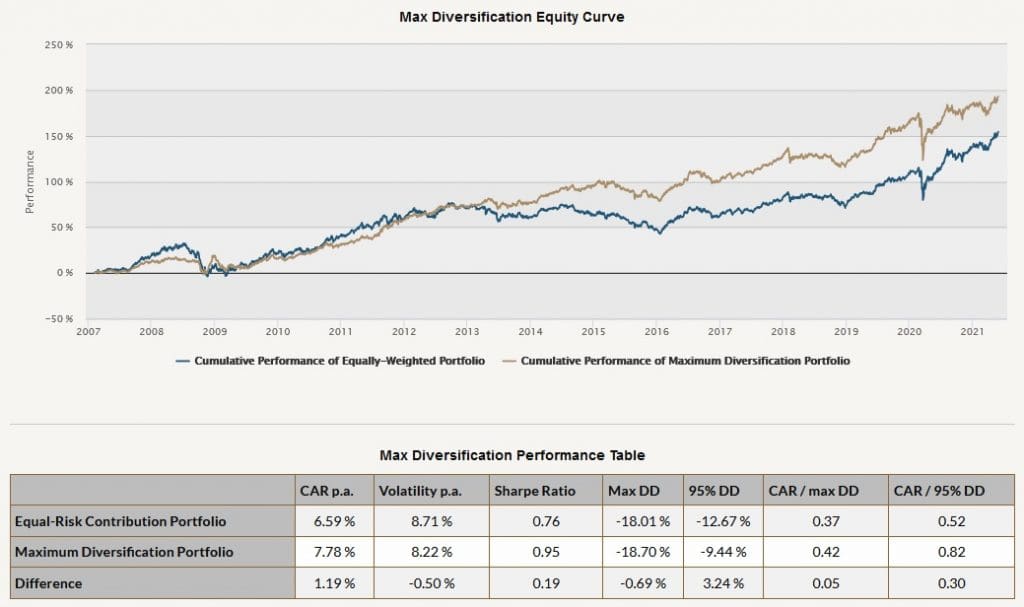

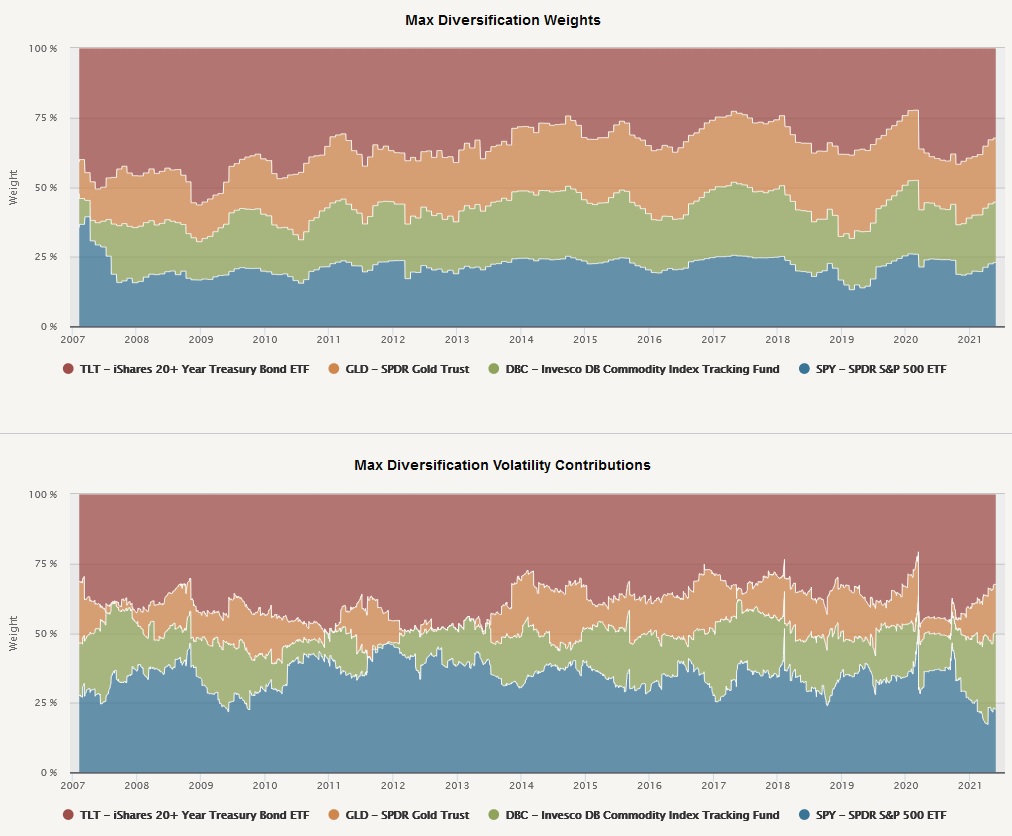

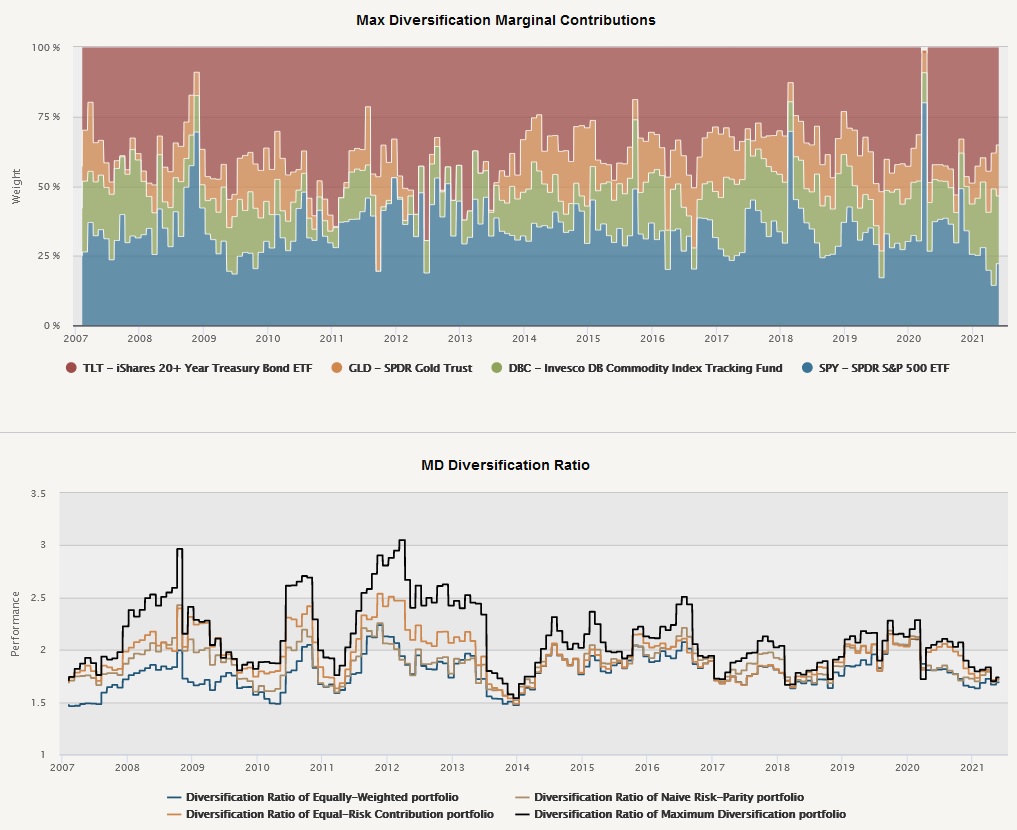

Plus, two new additional Quantpedia Pro reports are again related to the Risk Parity portfolio allocation strategies. In April, we implemented the Naive Risk Parity method and May was dedicated to the implementation of Equal Risk Contribution and Maximum Diversification methods. All Risk Parity methods contain similar charts (equity curves, performance table, risk contributions, volatility contributions), plus we have added two new charts – marginal risk contribution and diversification ratio over time.

And finally, four new blog posts that you may find interesting have been published on our Quantpedia blog in the previous month:

Measuring Financial Investors Presence in Commodities

Authors: Zeno Adams, Solene Collot and Davide Rossi

Titles: Measuring Financial Investor Presence through Term Structure Anomalies

Pump and Dump in Cryptocurrencies

Authors: Anirudh Dhawan and Tālis J. Putniņš & Tao Li, Donghwa Shin and Baolian Wang & Jiahua Xu and Benjamin Livshits

Title: A New Wolf in Town? Pump-and-Dump Manipulation in Cryptocurrency Markets & Cryptocurrency Pump-and-Dump Schemes & The Anatomy of a Cryptocurrency Pump-and-Dump Scheme

ESG Incidents and Shareholder Value

Author: Simon Glossner

Title: ESG Incidents and Shareholder Value

Risk Parity Asset Allocation

Author: Daniela Hanicova

Title: Risk Parity Asset Allocation

Stay safe …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend