Quantpedia in October 2022 – the 100-Year Portfolio Analysis Report

Hello all,

I am glad that I can finally present the new Quantpedia Pro report that I have been looking forward to for the past few months – the 100-Year Portfolio Analysis. We spent the last few months gathering data – be it our historical analysis of the US Dollar, US Treasuries, commodities, or trend-following strategies. But the main goal of those articles was always to prepare the ground for the tool that gives our users the opportunity to review the hypothetical performance of any model portfolio (any trading strategy, portfolio of ETFs, or custom equity curves) during a very long historical period – since 1926. The article with a complete methodology was published a few days ago, so the natural question is: How does the real report look like?

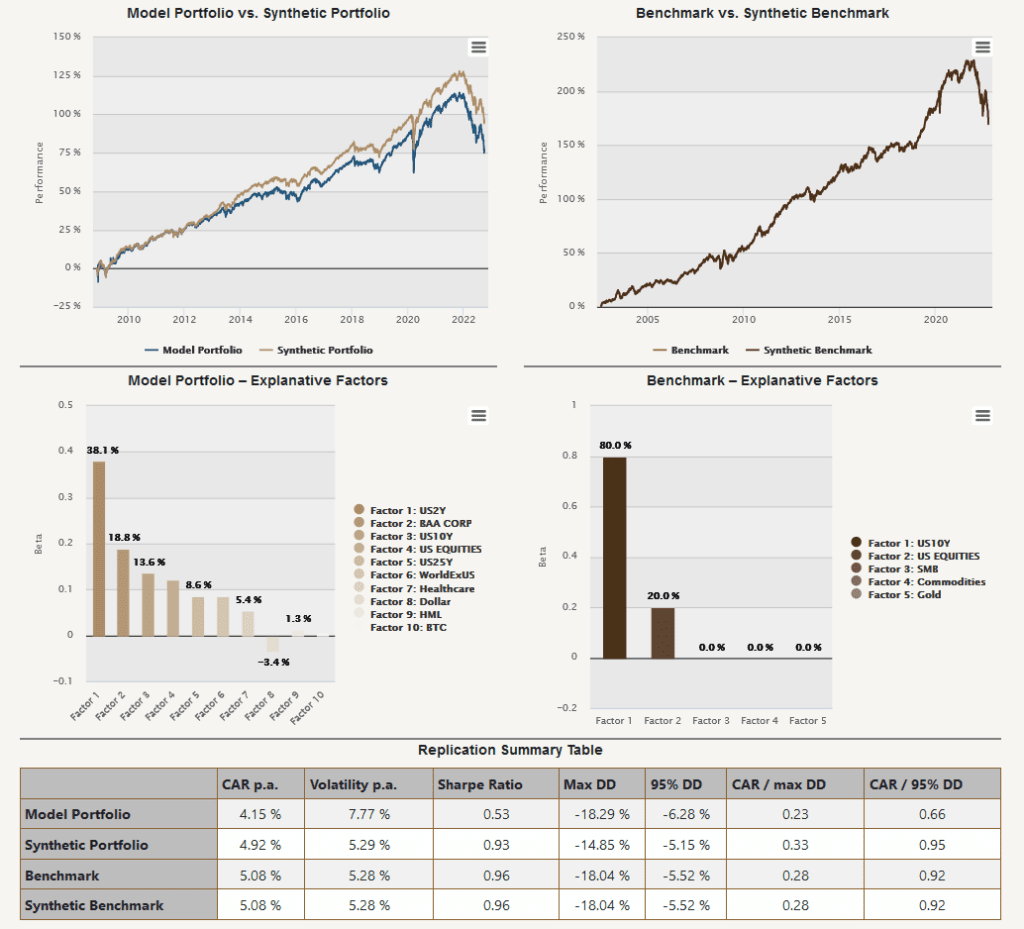

In the first step, we use the multi-factor regression to build a synthetic portfolio and benchmark and let users review the in-sample match.

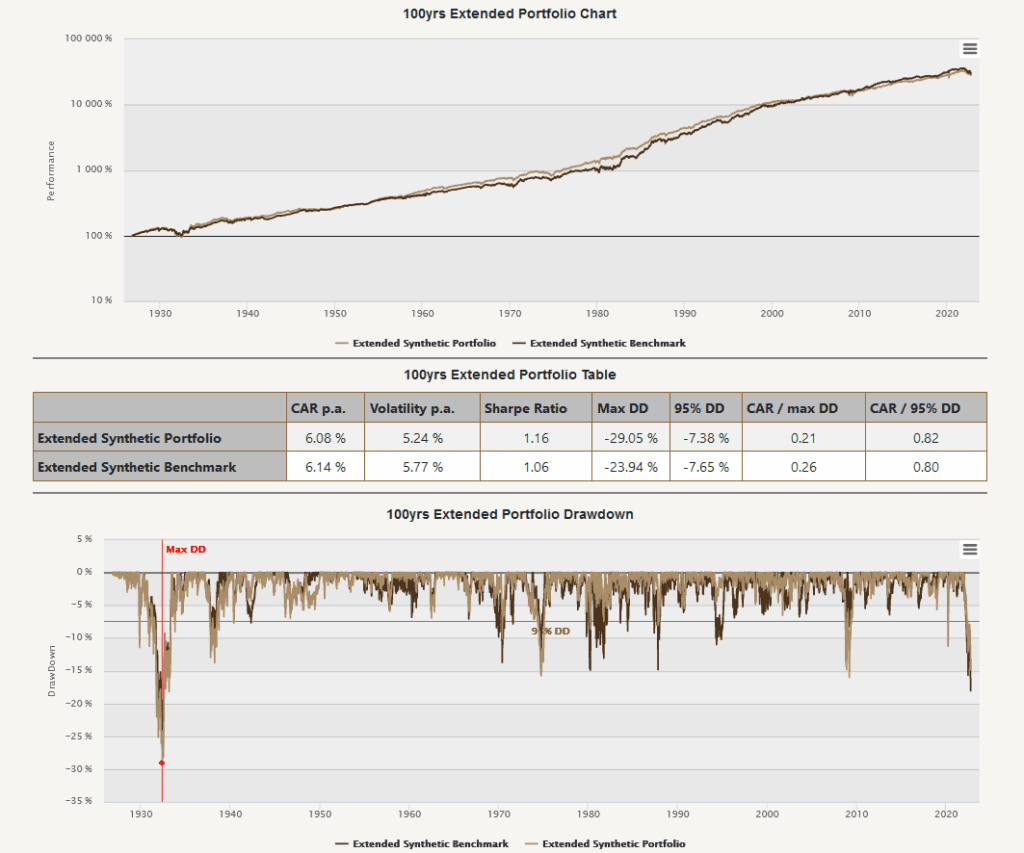

Afterward, we extend the history of a model portfolio & benchmark to nearly 100 years by modeling an input portfolio & benchmark via 18 factors with rich data history.

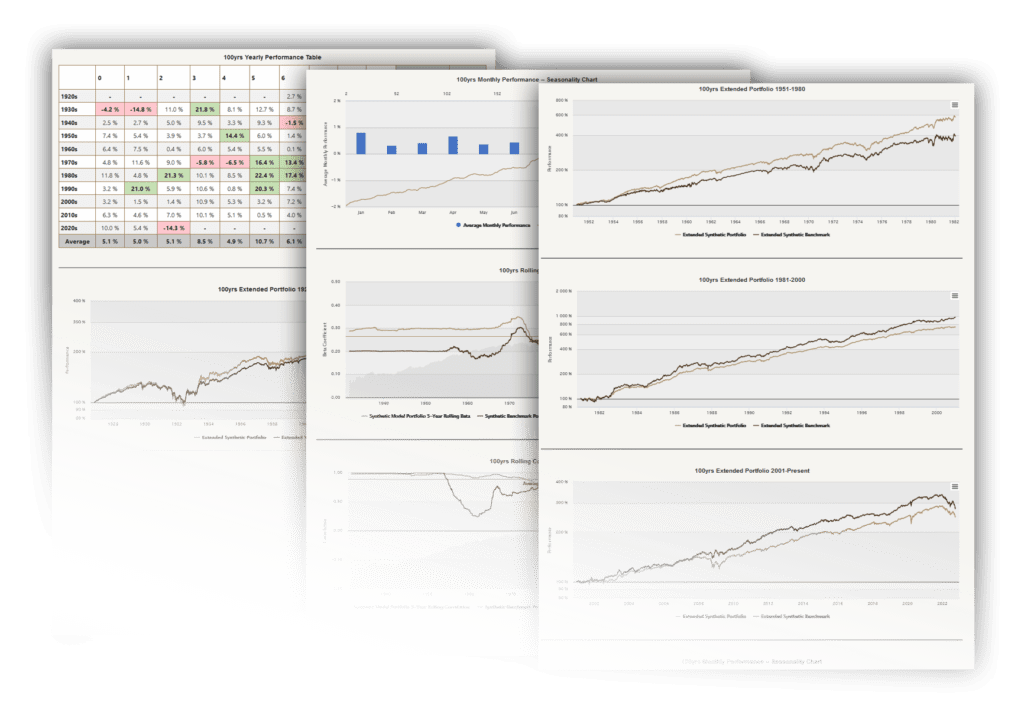

Users can then review synthetic portfolio and benchmark performance over an extended period, check performance in four sub-periods on a year-by-year basis, and monthly seasonality in synthetic portfolio performance. At the end are charts showing rolling correlation and beta to the US equities.

Let’s also quickly recapitulate Quantpedia Premium development:

- 11 new Quantpedia Premium strategies have been added to our database

- 11 new related research papers have been included in existing Premium strategies during the last month

- 9 new backtests were written in QuantConnect code. Our database currently contains over 600 strategies with out-of-sample backtests/codes.

Additionally, 6 new articles were published on the Quantpedia blog in the previous month, 3x analysis of academic research papers and 3x Quantpedia study:

- How to Replicate Any Portfolio

- Introducing Quantpedia Answers

- How to Improve Post-Earnings Announcement Drift with NLP Analysis

Analysis of research papers:

The Role of Interest Rates in Factor Discovery

Authors: Jules H. van Binsbergen, Liang Ma, and Michael Schwert

Title: The Factor Multiverse: The Role of Interest Rates in Factor Discovery

Stock-Bond Correlation, an In-Depth Look

Authors: Noah Weisberger and Xiang Xu

Title: Stock-Bond Correlation: A Global Perspective

&

Authors: Junying Shen and Noah Weisberger

Title: US Stock-Bond Correlation: What are the Macroeconomic Drivers?

Are FOMC Announcements Really Informative?

Authors: Oliver Boguth, Vincent Gregoire, and Charles Martineau

Title: Noisy FOMC Returns

Yours …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend