Quant’s Look on ESG Investing Strategies

ESG Investing (sometimes called Socially Responsible Investing) is becoming a current trend, and its proponents characterize it as a modern, sustainable, and responsible way of investing. Some people love it, others see it as just another fad that will soon be forgotten. We at Quantpedia have decided to immerse in academic research related to this trend to understand it better. How are ESG scores measured? What are the common problems in ESG data? Are there any systematic ESG factor strategies that offer outperformance? These are some of the areas we wanted to explore, and we invite you on this journey with us …

Introduction to ESG Investing

ESG scores and data problems

Companies, investors or academics are usually focused on the ESG scores of companies in the context of the responsibility, where E stands for environmental, S for social and G for governance qualities of firms. The scores should measure the quality and responsibility of the firm’s behavior in each of the categories.

- Various environmental practices are in the scope of the environmental score – for example, environmental management systems, pollution, carbon emissions, low resource consumption and product innovations aiming at improving environmental protection.

- The social score is focused on human rights, safety standards for workers, cash donations, protection of public health, business ethics, respect to the diversity of the workforce, etc.

- The governance dimension is a measure of behavior concerning the board of directors, shareholder rights and the integration of financial and non-financial goals of the company.

Although the ESG scores can be easily understood, there is a problem with the ESG data.

If we look at more traditional financial factors/metrics/indicators, there is only one way how to measure the book to market ratio. However, the world of ESG scores is different. Several data providers have ESG score databases. The problem is that each dimension of the ESG score can be measured differently; for example, for the environmental score, two data providers can measure different aspects of a firm to obtain the final score. Moreover, the numerical measurement of each element could be different across data providers, and the various features could form the final score with different weights. Therefore, there is no consent in a way how to measure ESG scores. As a result, ESG scores for the same company can widely vary across data providers.

The aforementioned complicates the world of sustainable investing for market practitioners, academics interested in the research and even the companies that cannot correctly evaluate their activities to become more sustainable and attractive. We would dive deeper into problems with ESG data in the later section since this is one of a key issue with ESG investing.

Mixed opinion of academic research

Despite the blurred ESG scores, this topic is in the scope of academic papers. Research is not only interested in the difference of the ESG scores, but also in the relationship of the ESG scores and the financial performance. One branch of literature is interested in the applicable strategies based on ESG scores and examining whether such addition is performance-enhancing, performance detrimental or has no effect. The enhancement of the performance would be attractive for the largest group since it would mean that the ESG scores could be utilized as factors and used in practice. Even the no effect of ESG on the performance would be interesting for everyone who seeks sustainable investing. Lastly, the focus on the ESG scores could lead to investing in unprofitable firms or reducing the investment universe in a way that it would not be diversified.

There is plenty of literature that supports each of the hypotheses mentioned above what can cause overall confusion.

On the positive note, Gabriel Huppé in “Alpha’s Tale: The Economic Value of CSR”[8] suggests that corporate social investing alpha arose because investors have continuously underestimated information about social responsibility. However, omitting such relevant information leads to a surprise of the performance of the corporate social responsibility leaders and the re-evaluation of their decisions. Research by Clark, Feiner and Viehs[3] meta-studied more than 200 different sources and found a correlation between sustainable business practice and economic performance. In the paper, 88% of reviewed sources state that sustainability practices are translated into better cashflows, where the mechanism is simply a better operational performance. Additionally, 80% of sources report that sustainable practices are also positively related to investment performance. Therefore, these results indicate that good investing practices and returns at the same time are not impossible.

Some papers are mixed, according to Fulton, Kahn and Sharples[5], firms with high ESG ratings can better finance their activities, since such firms have a lower cost of the capital. Stocks of such firms also have a lower risk than others. However, the paper also states that “88% of studies of actual SRI fund returns show neutral or mixed results“ and “we have found that SRI fund managers have struggled to capture outperformance in the broad SRI category, but they have, at least, not lost money in the attempt.“

Statman and Glushkov[11] have negative opinion on ESG, they have found that exclusion of sin stocks hamper returns.

For each opinion about the ESG and the performance, there is a paper that supports it. There can be found articles about the positive effects, no effect, and negative effects. However, as we plan to show later, these results should not be generalized and in our opinion, mostly emerge from the significant dispersion in ESG databases and from differences in ESG measurement.

Interest in ESG is growing

Socially responsible investing is gaining popularity, a number of published academic papers and worldwide coverage in the news. Such attention could be explained by mainly two factors.

- Firstly, there might be a non-financial motivation. This could be caused by religion, for example, stock screening criteria based on Christian values. Such an approach would exclude sectors like the armament industry, alcohol or gambling. Additionally, there is also literature about Islamic investments, Shariah-compliant investments. Such investment funds are not making any investments in industries such as gambling, alcohol, pork, and companies providing financial services on interest.

- Apart from religion, there could be a philanthropic point of view that seeks green, socially responsible investments. Companies that have high ESG score can be seen as a superior in the eyes of investors.

However, the literature offers also a different view on this topic. Some branch of the literature suggests that high ESG firms should outperform the low ESG firms in the long run. The reason is simple; firms with better governance should outperform those with worse, environmental sustainability can prevent government fines and make the company more attractive among customers. The social aspect also influences the popularity of the company and the favorable workplace benefits workforce. The reputation and good image of the company reflected by the ESG score can be seen as the additional expense, but this can cause that customers will pay more for the product. To sum it up, according to the one branch of literature, the high ESG stocks should outperform the low ESG stocks.

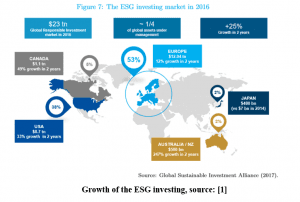

Either because of the responsible investing or the seek for profit, the ESG investing is becoming more and more popular. The following picture from the paper written by Bennani, Le Guenedal, Lepetit, Ly, Mortier, Roncalli and Sekine[1] shows the status of the ESG investing market in 2016. Assets under management in the ESG related strategies are significant, and Europe is leading this trend.

The problem(s) with ESG

As we have previously mentioned, the usage of ESG is not that straightforward, and in this section, we would like to dive deeper into problems that are recognized by various academic papers.

Firstly, there is a problem with a lack of commonality across various papers that study ESG scores. Some papers examine only ecological aspects, some ignore governance and other papers are focused on social responsibility. However, this problem is not that determining in the whole process of examination of the ESG scores. There is a growing number of researches that are focused on the entire dimension of ESG.

Secondly, there is a big problem with the data of the ESG scores; the scores can be very different across data providers. Berg, Kölbel and Rigobon[2] examine data from five different rating agencies (KLD, Sustainalytics, Vigeo-Eiris, Asset4, and RobecoSAM). The paper has found out that the average correlation between scores is 0.61 and that this value ranges from 0.42 to 0.73.

No doubt, there is a significant dispersion among the data, which makes it difficult for practitioners, companies, and academics as well. This makes it hard or sometimes even impossible to price ESG scores in the market correctly. Moreover, it is hard for the companies to improve their image and sustainability, since according to the one ESG score, the company could be one of the better firms, while the other ESG score can indicate something very different. As a result, any study on the relation of the scores and performance is influenced by choice of the data set.

This research identifies three major sources of the aforementioned variability in the datasets. The authors identify a scope divergence of attributes, which mean that there are different aspects across providers that together form ESG score. Secondly, there is a different numerical measurement of all the aspects and finally, an aggregation rule that combines all the chosen and measured aspects into the final score. According to the paper: “We find that 53 percent of the difference of the ratings stems from measurement divergence, while scope divergence explains 44 percent, and weight divergence another 3 percent. In other words, 53 percent of the discrepancy comes from the fact that the rating agencies are measuring the same categories differently, and 47 percent of the discrepancy stems from aggregating common data using different rules. This means that for users of this data – financial institutions for instance – a sizable proportion of the discrepancy could be resolved by sharing the data on the indicator level and having a common procedure for aggregation.”

Therefore, it might be practical to use data from the broader set of ESG rating agencies, and build a model that will extract the needed information or aggregate scores into one. For example, some dimension reduction approach could be used.

Additionally, the paper has identified a “rater effect“, where the effect implies that the judgments or ratings are correlated among indicators. If one indicator of the company is viewed positively (negatively), it is likely that also other indicators would be viewed positively (negatively). Finally, the paper has identified that the divergence is most pronounced for KLD data. However, this is the data set on which most of the academic research is based. Therefore, it may cause problems with the results and their interpretation.

Study by Gibson, Krueger, Riand and Schmidt[6] also concludes that ESG scores widely differ across the datasets (Asset 4, Sustainalytics, Inrate, Bloomberg, MSCI KLD and MSCI IVA). In this research, the average correlation between ESG ratings is even lower at 0.46. The average is lowest for the governance score, while for the environment is the average highest. The paper identifies that the most significant differences are in the social and governance ratings and tries to identify the reason. Research hypothesize that there are major differences in the stakeholder-centric model of the firm typical for the civil law countries and shareholder-centric model of the firm that is typical for the common law countries. The results support this hypothesis. While civil law is dominant in Europe, the common law is prevailing in the US. This is particularly interesting since the ESG is most spread in Europe and the United States. Social issues are more important in civil law countries and therefore, data providers from such countries (Europe) are better in identifying social issues relevant to the financial world. On the other hand, governance is more important in common law countries (U.S.) with a shareholder centered view. Therefore, providers based in the common law countries are better in the understanding of governance. However, these phenomena are reflected by the dispersion in the ESG scores. That is a crucial problem since a lot of studies are based on a global investment universe like MSCI World, where the civil and common law countries are mixed.

The results of the previous papers indicate that it might be reasonable to examine trading strategies and their investment universes with caution because there could be different results when different datasets are used.

Relationship of ESG and performance

This section is closely related to the previous parts, firstly, as we have previously mentioned, the motivation to invest in socially responsible stocks is rising. As a result, more and more money is invested in ESG related strategies. However, this means that papers may have different results that could be related to their period.

Nextly, the results of academic papers would be affected by choice of the dataset. Therefore, we would always specify a provider of the data.

Finally, there could also be a problem with the lack of commonality, for example, excluding worst-performing stocks by some ESG score. Naturally, two different approaches would probably lead to different results. For example, excluding worst governance stocks may be largely profitable while excluding the worst social stocks may not.

In the following sections, we would categorize several ESG strategies and compare them across various academic papers.

Negative screening

Probably the easiest way how to incorporate ESG scores into trading portfolios is by doing some negative screening. The investor excludes the worst scorers and reduces the investment universe.

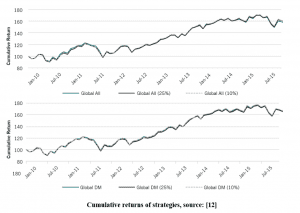

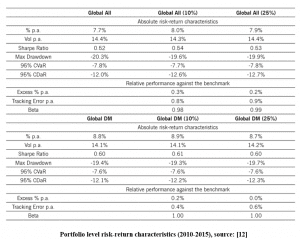

In the paper written by Verheyden, Eccles and Feiner[12], authors tested the exclusion of worst-performing ESG stocks or filtering the investment universe. Paper has analyzed either “Global All” universe or “Global Developed Markets (DM)”. The first consists of large and mid-cap stocks in 23 developed and 23 emerging markets and the second one consists of large and mid-cap stocks of developed markets. The simple strategy was to exclude either bottom 10% or 25% of stocks, sorted by overall ESG scores. The benchmark is either Global All or Global DM. Strategies are marked by the percent of stocks that are excluded – either (10%) or (25%). The data provider is Sustainalytics, this dataset is one of the most correlated with others, while the only exception is KLD (see the correlation table in the section “Problems with ESG”).

This paper partly addresses hypothesis whether the exclusion of stocks would reduce the profitability of the strategy. Clearly, the strategies are not less profitable than benchmarks, in fact the performance is better; therefore, one could conclude that the exclusion of the worst ESG performers leads to slightly better performance. This could be characterized as doing well by doing good. Moreover, from the quant’s point of view, the paper also summarizes the resulting numbers and metrics in the following table.

We can directly compare the results of this paper, to the results of paper written by Statman and Glushkov[11]. This research has analyzed returns from 1992 to 2007 of stocks rated on social responsibility by KLD. This is absolutely related to the aforementioned problems with ESG, the backtesting period is not consistent and the source of the data is KLD – data provider that is least consistent with others. The difference is also in the investment universe. This paper uses data of stocks that are measured by the KLD – components of S&P500, Domini 400 Social Index, Russell 1000 Index and Russell 3000 Index. Paper agrees that the tilt for the responsible stocks can provide a return advantage relative to common stocks, but according to the study, such investors also shun stocks of companies in the business of tobacco, alcohol, gambling, firearms, military, and nuclear operations. The results indicate that shunning does not seem to be profitable because such action leads to a return disadvantage relative to conventional investors. As a result, the return advantage of highly socially responsible stocks is largely offset by the return advantage related to the exclusion filter.

ESG “level” strategies

Another possibility is not to throw away the lowest ESG stocks from the investment universe, but to tilt towards better-rated stocks. Nagy, Kassam and Lee[9] analyzed such strategy, using the stocks of the MSCI World index during 2007-2015. ESG ratings were obtained from the MSCI (IVA scores). The strategy was profitable, but the performance was only 1.06%.

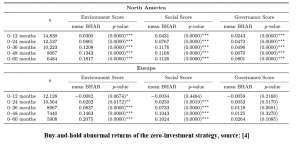

A slightly different approach is used in the work of Dorfleitner, Utz and Wimmer[4], a source paper of ESG Factor Investing Strategy in the Quantpedia’s Screener. This paper uses data from the Asset4 and stocks that are scored by this firm in the various regions (North America, Europe, Japan and Asia Pacific). The period is from 2002 to 2011. Investment strategy consists of ranking stocks each month according to their E, S and G scores. The research goes long top 20% stocks of each score and shorts the bottom 20% stocks of each score. Therefore, the paper examines an individual strategy for each score. The most promising results are for the North America and Europe region, but that is not a surprise since the ESG investing is most spread there. The theory expects that in the short term, firms with high ESG scores would have abnormal returns of zero, but in the long run, theory expects positive abnormal returns. On the other hand, firms with low ESG scores are expected to have negative abnormal returns. Additionally, results indicate that financial markets are inefficient in terms of ESG scores and are not capable of adequately pricing different levels of corporate social performance in the short run and particularly in the long run.

ESG Momentum

Paper by Nagy, Kassam and Lee [9] has examined the ESG Factor Momentum Strategy. Authors suggest that a firm which has improved the ESG the most is expected to outperform. Although, the advantages of a better-rated ESG portfolio are expected to be apparent only in the long term, for example, because of increased cash flows, etc. According to the paper, it is likely that the market could react to a change in rating in a relatively short period. Given the rise of the ESG investing, we may see a reducement in the reaction period. We hope that this topic would be revisited. Therefore, the strategy is to overweight, relative to the MSCI World Index, companies that increased their ESG ratings most during the recent past and underweight those with decreased ESG ratings. Lastly, the strategy is profitable, but the profit is low (2.23%).

Positive stock‘s characteristics

Ignorance of ESG risk was examined in the paper written by Simon Gloßner[7]. By using a risk metric from RepRisk that measures ESG risk exposure of a firm by quantifying past ESG incidents (for example leaking pipeline, explosion, etc.). A portfolio that is formed by controversial firms that are known for having ESG incidents has significantly negative long-run returns both in Europe and in the United States. Results are significant even when one controls for risk factors, industries and firm characteristics; the alpha is negative. There are several takeaways from this paper.

- Firstly, the market seems to be unable to fully incorporate ESG risks into investment decisions, which affects performance.

- Secondly, market practitioners do not pay enough attention to ESG information.

- Lastly, according to the paper, an ESG screen may positively impact investment performance. The exclusion of the most controversial firms from a portfolio makes it more socially responsible and may also positively affect the performance.

The result is related to the previous papers about negative screening, but this paper examines the ESG incidents, not the scores, which makes it different.

Conclusion

The popularity gaining ESG scores can be suitable for profitable investing or lowering the risk of the portfolio. However, there are some flaws with the ESG scoring and strategies. Firstly, the ESG data are not consistent, which means that the reproduction of some approach proposed by any academical reasearch will lead to different results if the same dataset is not used. A possible solution would be to work with as many datasets as it is possible and build a model that will handle all the information possible or filter it. Secondly, the studies often examine the same phenomena during different periods and with different investment universes. Additionally, there could be a problem of understanding two distinct approaches as one, for example, negative screening. This can lead to dangerous generalizations, where, according to one paper, negative screening is wrong, while others find benefits of such strategy.

However, we believe that we presented some possible usages of ESG scores from the quantitative point of view. Either for a profit-enhancing properties or simply for producing more socially responsible strategies.

References

[1] Bennani, Leila and Le Guenedal, Théo and Lepetit, Frédéric and Ly, Lai and Mortier, Vincent and Roncalli, Thierry and Sekine, Takaya, How ESG Investing Has Impacted the Asset Pricing in the Equity Market (November 27, 2018). Available at SSRN: https://ssrn.com/abstract=3316862 or http://dx.doi.org/10.2139/ssrn.3316862

[2] Berg, Florian and Kölbel, Julian and Rigobon, Roberto, Aggregate Confusion: The Divergence of ESG Ratings (August 17, 2019). MIT Sloan Research Paper No. 5822-19. Available at SSRN: https://ssrn.com/abstract=3438533 or http://dx.doi.org/10.2139/ssrn.3438533

[3] Clark, Gordon L. and Feiner, Andreas and Viehs, Michael, From the Stockholder to the Stakeholder: How Sustainability Can Drive Financial Outperformance (March 5, 2015). Available at SSRN: https://ssrn.com/abstract=2508281 or http://dx.doi.org/10.2139/ssrn.2508281

[4] Dorfleitner, Gregor and Utz, Sebastian and Wimmer, Maximilian, Where and When Does It Pay to Be Good? A Global Long-Term Analysis of ESG Investing (October 7, 2013). 26th Australasian Finance and Banking Conference 2013. Available at SSRN: https://ssrn.com/abstract=2311281 or http://dx.doi.org/10.2139/ssrn.2311281

[5] Fulton, Mark and Kahn, Bruce and Sharples, Camilla, Sustainable Investing: Establishing Long-Term Value and Performance (June 12, 2012). Available at SSRN: https://ssrn.com/abstract=2222740 or http://dx.doi.org/10.2139/ssrn.2222740

[6] Gibson, Rajna and Krueger, Philipp and Riand, Nadine and Schmidt, Peter Steffen, ESG Rating Disagreement and Stock Returns (August 6, 2019). Available at SSRN: https://ssrn.com/abstract=3433728 or http://dx.doi.org/10.2139/ssrn.3433728

[7] Gloßner, Simon, The Price of Ignoring ESG Risks (May 18, 2018). Available at SSRN: https://ssrn.com/abstract=3004689 or http://dx.doi.org/10.2139/ssrn.3004689

[8] Huppé, Gabriel A., Alpha’s Tale: The Economic Value of CSR (July 30, 2011). Principles for Responsible Investment Academic Conference, September 2011. Available at SSRN: https://ssrn.com/abstract=1969583 or http://dx.doi.org/10.2139/ssrn.1969583

[9] Nagy, Zoltán and Kassam, Altaf and Lee, Linda-Eling, Can ESG Add Alpha? An Analysis of ESG Tilt and Momentum Strategies (2016). Available at: https://www.semanticscholar.org/paper/Can-ESG-Add-Alpha-An-Analysis-of-ESG-Tilt-and-Nagy-Kassam/64f77da4f8ce5906a73ffe4e9eec7c49c0960acc

[10] Sjöström, Emma, The Performance of Socially Responsible Investment – A Review of Scholarly Studies Published 2008-2010 (October 17, 2011). Available at SSRN: https://ssrn.com/abstract=1948169 or http://dx.doi.org/10.2139/ssrn.1948169

[11] Statman, Meir and Glushkov, Denys, The Wages of Social Responsibility (December 26, 2008). Available at SSRN: https://ssrn.com/abstract=1372848 or http://dx.doi.org/10.2139/ssrn.1372848

[12] Verheyden, Tim and Eccles, Robert G. and Feiner, Andreas, ESG for All? The Impact of ESG Screening on Return, Risk and Diversification (2016). Journal of Applied Corporate Finance, 28(2), 47-55. Available at SSRN: https://ssrn.com/abstract=2834790

Authors:

Radovan Vojtko, CEO, Quantpedia.com

Matus Padyšák, Analyst, Quantpedia.com

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend