Takeover Factor Explains the Size Effect

The size effect assumes a negative relationship between average stock returns and firm size. In other words, it states that low capitalization stocks outperform stocks with large capitalization. Academics propose several possible explanations why this happens, including greater flexibility of small firms, more space for them to grow and higher inside innovation.

Although generally accepted, the size effect keeps being challenged. Researchers have been asking how important the firm size characteristic actually is, and whether it is possible to replace the traditional size factor of Fama and French asset pricing model (1993) with more accurate factor. Recently, one potential challenger has emerged – so-called takeover factor, employed by Easterwood et al. (2022). In their study, they work on the assumption that small firms are often targets of takeovers, which gives us a different perspective on merger and acquisition news in regards to size effect. Their results show that M&A component of average returns explains the size premium entirely; returns on takeover factor are in correlation with SMB returns, and finally, while takeover factor models are able to estimate the size factor, it does not work the other way around.

To sum it all up, according to research of Easterwood et al. (2022), takeover factor should replace the conventional size factor in benchmark asset pricing models as merger announcement component of returns drives the entire measured size premium.

Authors: Sara Easterwood, Jeffry Netter, Bradley Paye, Michael Stegemoller

Title: Taking Over the Size Effect: Asset Pricing Implications of Merger Activity

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4055513

Abstract:

We show that merger announcement returns account for virtually all of the measured size premium. An empirical proxy for ex ante takeover exposure positively and robustly relates to cross-sectional expected returns. The relation between size and expected returns becomes positive or insignificant, rather than negative, conditional on this takeover characteristic. Asset pricing models that include a factor based on the takeover characteristic outperform otherwise similar models that include the conventional size factor. We conclude that the takeover factor should replace the conventional size factor in benchmark asset pricing models.

Notable quotations from the academic research paper:

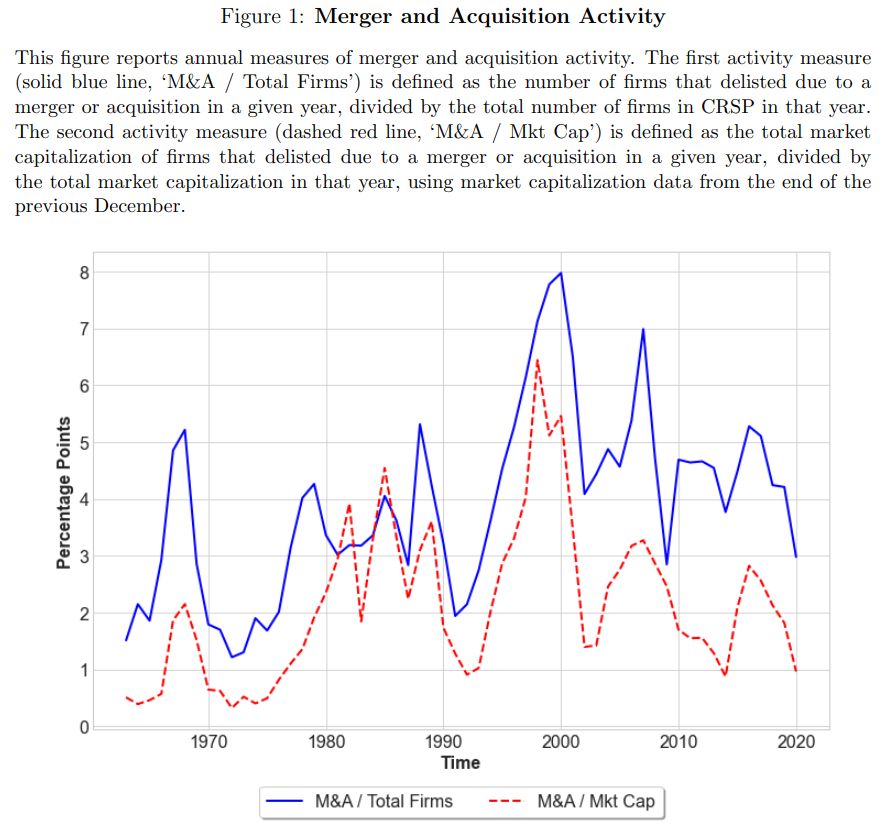

“Not surprisingly, target firms tend to be members of small capitalization portfolios. Nearly 50% of takeovers of public firms occur for firms in the smallest size decile portfolio, and nearly two-thirds of takeovers involve targets in the smallest size quintile portfolio.

Following Cremers et al. (2009), we construct a “takeover factor” as a long-short portfolio based on extreme takeover likelihood quintiles or deciles.

The first portion of our study decomposes ex post average returns for the size factor and other anomaly portfolios into a component associated with realized M&A news and a residual.

…we find that the size premium is entirely driven by the M&A component of returns. For example, the annualized average return for a long-short portfolio based on size quintiles is approximately 1% over our sample period. We show that around 1.6% of this premium – over 100% of the premium – is attributable to the realized M&A component of returns. The ‘residual’ size premium is negative, such that small firms earn lower average returns relative to large firms after removing the M&A return component.

The second portion of our paper shifts to an ex ante perspective. We measure differences in exposure to takeover activity via the estimated likelihood that a firm will become a target in the following year based on a logistic regression model.

We show that the relation between size and expected returns changes from negative to positive upon including the takeover characteristic along with other standard characteristics linked to cross-sectional return patterns.

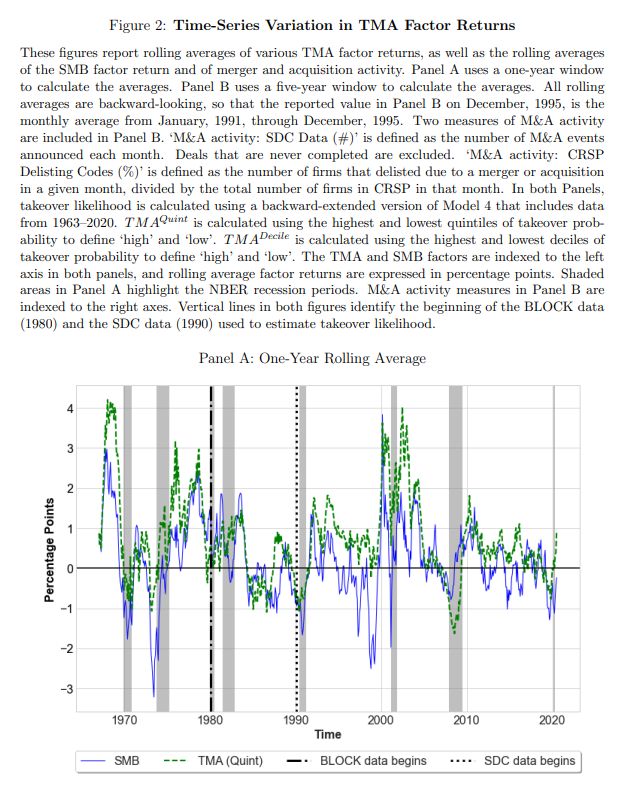

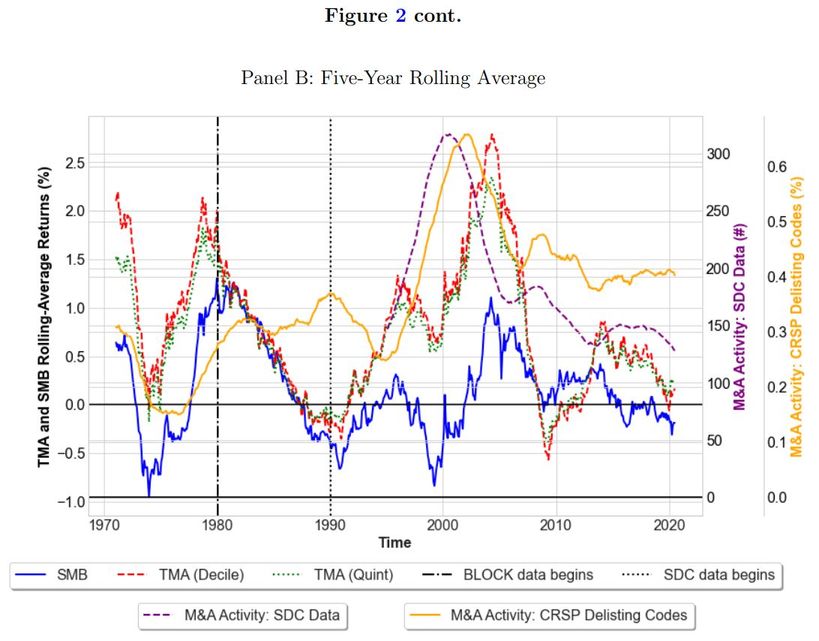

We next consider the asset pricing performance of models that include a “takeover factor” constructed as a hedge portfolio based on the takeover likelihood characteristic, following Cremers et al. (2009). Takeover factor returns correlate positively with SMB returns. Both factors tend to perform relatively well during economic expansions, but poorly just prior to and during economic recessions. However, the premium for the takeover factor is substantially larger than that for the size factor, especially over the most recent three decades.

We measure firm-level daily returns attributable to acquisition announcements using standard event study methods. Aggregate acquisition-related abnormal returns for a particular portfolio are then computed in the same manner as traditional value-weighted (or equal-weighted) portfolio returns, except using the acquisition-related abnormal returns as opposed to total returns.

We focus on deal announcements because these news events are most likely to generate large valuation effects that can be reliably attributed to merger news. The specific announcements included in our analysis consist of SDC-recorded M&A deal announcements during the period 1990–2020. The total number of included events E therefore equals the 46,905 announcement events involving public targets or acquirers following the additional data screens that we apply.

Asset pricing tests indicate that the inclusion of the takeover factor materially improves various benchmark models’ ability to explain return premia. In contrast, the traditional size factor adds little explanatory power to factor models that include the takeover factor.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend