The Fallacy of Concentration Risk

Market concentration has become one of the most discussed structural risks in today’s equity markets. A small group of mega-cap stocks—often the largest five to ten names—now accounts for an unusually large share of major market indices. This has led to widespread concerns that such concentration makes markets more fragile and that elevated index weights at the top may foreshadow weaker future returns. Many investors worry that history is repeating itself and that extreme concentration today implies disappointment tomorrow.

A recent research paper, The Fallacy of Concentration, challenges this popular narrative. While the authors confirm that market concentration is indeed historically high, they find little evidence that concentration itself is a meaningful predictor of future market performance. Using the “effective number of stocks” as a formal concentration metric, the study shows that periods of high concentration have not reliably preceded lower returns, higher volatility, or deeper drawdowns in subsequent periods.

The authors explicitly test whether concentration contains ex-ante predictive information for returns and risk. Across multiple specifications—including panel regressions with time and sector fixed effects—the results are consistent: concentration explains virtually none of the variation in future returns. The incremental explanatory power is economically trivial and statistically insignificant. In other words, knowing that an index is highly concentrated provides little insight into how it will perform next year.

The key takeaway is subtle but important. While market concentration may feel uncomfortable and intuitively risky, it is not, by itself, a reliable signal for timing markets or adjusting equity exposure. Concentration appears to be more a byproduct of successful firms growing larger than a warning sign of imminent underperformance. For investors, this research suggests caution against making allocation decisions based solely on how concentrated the market looks—because concentration alone has historically offered very little guidance about what comes next.

Authors: Mark Kritzman and David Turkington

Title: The Fallacy of Concentration

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5436695

Abstract:

Many investors believe that the U.S. stock market is riskier than it has been historically because a large fraction of its capitalization is concentrated in a few large technology companies. Some investors, therefore, conclude that they should rebalance their portfolios toward safer assets. The authors present clear evidence that the U.S. stock market has indeed become more concentrated. However, they also discuss practical and theoretical arguments and present persuasive empirical evidence that gives pause to the notion that investors should act to offset concentration.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“▪ Conventional wisdom holds that the stock market becomes riskier if a small number of companies grows to become a large fraction of the market’s capitalization.

▪ The U.S. stock market has become increasingly concentrated in a small number of technology companies in recent years as the AI revolution has channeled investment to these companies.

▪ However, both intuition and theory, supported by persuasive empirical evidence, belie the conventional wisdom that concentration begets risk. The U.S. stock market has not become riskier as it has become more concentrated.

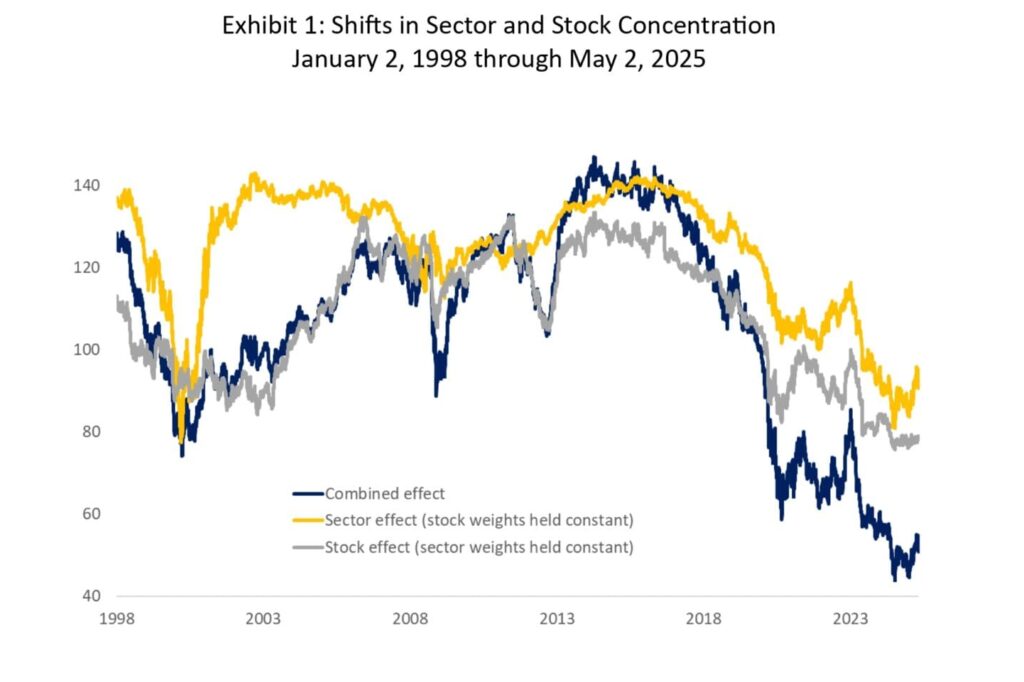

Exhibit 1 clearly shows that the S&P 500 Index recently has become more concentrated than any time since 1998 and that this concentration is due both to sector and stock effects. But Exhibit 1 covers a relatively short period. We therefore obtain monthly market capitalization data for 49 industries from Ken French’s online data website from July 1926 through June 2025.2

Exhibits 4 and 5 show the results of this dynamic trading rule compared to a buy-and-hold strategy with the same ex post average stock exposure of the dynamic trading rule. This rule of investing less in the stock market when it is more concentrated reduces return and increases risk compared to the buy-and-hold strategy that allows concentration to evolve naturally.

Exhibit 6 shows the effective number of stocks for 260 measurements (26 years by 10 sectors). It shows there is a significant amount of variation both cross-sectionally and through time.3

[Authors] provided undeniable evidence that the U.S. stock market is more concentrated currently than it has been for more than a quarter of a century and nearly as concentrated as it has ever been over the past century. And we showed that this increased concentration is due to both stock effects and sector effects.

Finally, [authors] reviewed several theoretical arguments about why investors should not act to offset concentration. We first discussed the power law which shows that concentration is a natural consequence of growth because growth is self-reinforcing. We then discussed the efficient markets hypothesis which holds that information arrives randomly and is immediately captured by prices; hence markets properly value companies. And we discussed the Capital Asset Pricing Model, which holds that in equilibrium investors should hold the market portfolio in combination with a safe asset irrespective of the market portfolio’s size distribution.

[Authors] therefore conclude that, regarding stock market concentration, the best action is no action.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend