Valuing Stocks With Earnings

Today, we will venture a little into the fundamental analysis corner, and we will give you a glimpse of an intriguing paper (Hillenbrand and McCarthy, 2024) that discusses the advantages of using ‘Street’ earnings over traditional GAAP earnings. The paper suggests that ‘Street’ earnings provide better valuation estimates and improved financial analysis. Is this a way how to improve the performance of the struggling equity value factor?

Street earnings contain more information about future fundamentals than GAAP earnings because they exclude transitory items. They also do not suffer from issues with smoothing past earnings and are unaffected by shifts in corporate payout policies. When applying the Campbell-Shiller decomposition to the Street price-earnings ratio, the results align with the excess volatility puzzle (Shiller, 1981): fluctuations in the Street price-earnings ratio are primarily driven by future returns, with little explanation from future earnings growth.

This suggests that stock returns should exhibit predictable return variation, a vital implication of the excess volatility puzzle. Accordingly, they demonstrate that the Street price-earnings ratio can predict stock returns both in-sample and out-of-sample. Their findings indicate that the Street price-earnings ratio is ideal for studying the excess volatility puzzle and return predictability. It may also help investors time their market exposure more effectively.

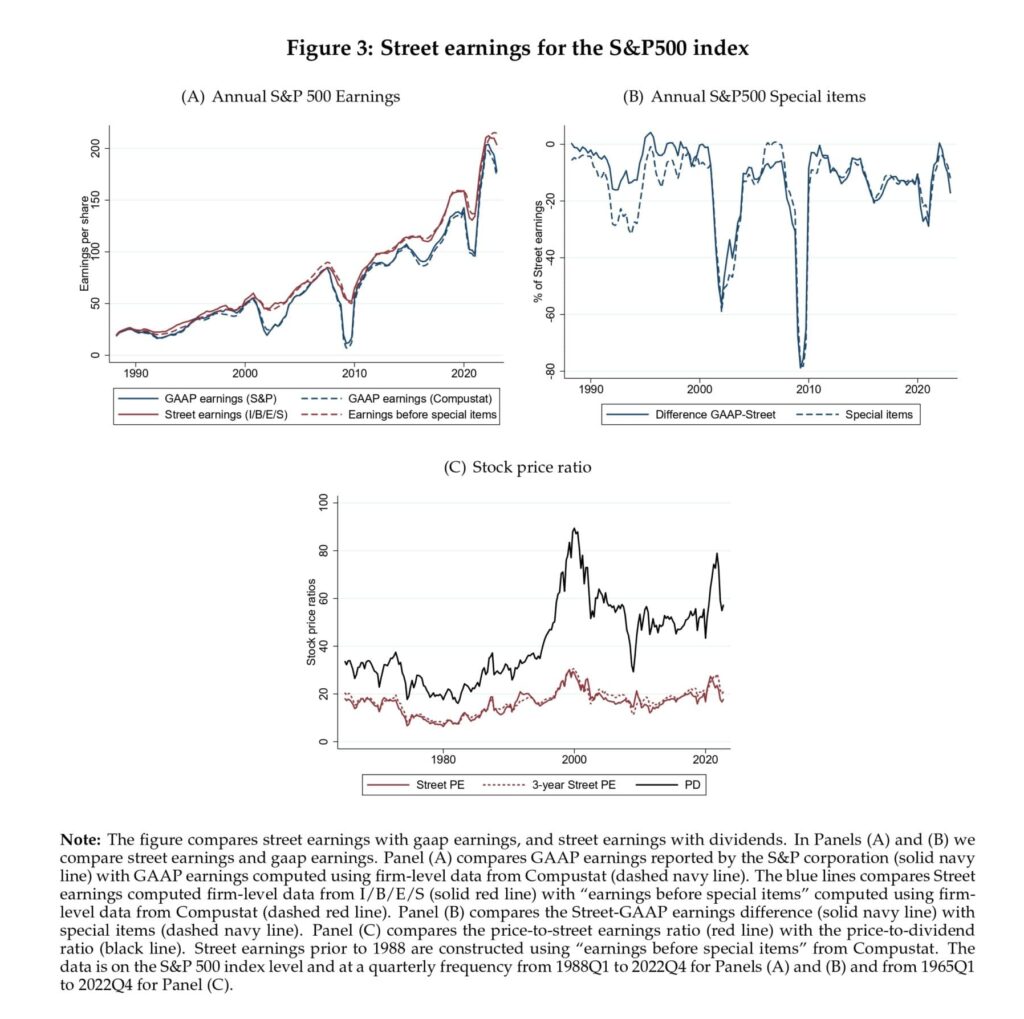

Despite the potential subjectivity, it is shown in Figure 3 that aggregate “earnings can closely replicate aggregate Street earnings reported by I/B/E/S before special items” using Compustat. This implies that subjectivity does not play a significant role since we can replicate the earnings numbers following a fixed set of rules.

An open question remains as to what drives excessive stock price movements. The street price-earnings ratio shows investors’ expectations of returns and earnings can help explain the excess volatility puzzle.

Authors: Sebastian Hillenbrand and Odhrain McCarthy

Title: Valuing Stocks With Earnings

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4892475

Abstract:

To address the excess volatility puzzle – the excessive movements in stock prices – researchers often study movements in valuation ratios. However, we demonstrate that movements in valuation ratios based on fundamental measures with high transitory volatility, such as commonly used earnings measures, are uninformative about movements in stock prices. To overcome this, we propose using an alternative fundamental measure: Street earnings. Street earnings, calculated before various transitory items, do not possess this transitory volatility and provide a more informative measure of future fundamentals. Consequently, movements in the price-to-street earnings (Street PE) ratio reflect movements in stock prices, making it highly informative about the excess volatility puzzle. Accordingly, we show that the Street PE has more in- and out-of-sample explanatory power for predicting returns than other valuation ratios. Additionally, it helps reconcile conflicting views on which subjective expectations drive stock price movements, showing that expectations of short-term earnings growth, long-term earnings growth, and returns can all help explain the excess volatility puzzle.

As always, we present several exciting figures and tables:

Notable quotations from the academic research paper:

“To validate the use of Street earnings, we demonstrate that, at the aggregate level, Street earnings are indeed a more stable and informative measure of earnings than GAAP earnings. First, we show the large difference between aggregate Street and GAAP earnings arises due to income statement items classified as “special items”. Specifically, aggregate (and industry-level) Street earnings (from I/B/E/S) are closely replicated by computing aggregate (and industry-level) earnings before “special items” as reported in Compustat.2 Second, because special items correspond to transitory items (such as one-off impairments, write-downs, etc.), by removing these transitory items, Street earnings are smoother and more persistent than GAAP earnings. Third, because transitory items have little relevance for future earnings, past Street earnings are more informative about future aggregate earnings (both GAAP and Street), consistent with the firm-level evidence documented in Rouen, So, and Wang (2021).

Using the Street PE, we find statistically and economically significant evidence for in-sample return predictability, for both short and long-horizon returns. The bias-adjusted predictive coefficients of −0.68 (p = 0.067), −2.43 (p = 0.021), and −4.95 (p = 0.005) for 1-year, 3-year, and 5-year returns, respectively, indicate significant predictive power. The increasing magnitude of these coefficients over longer horizons not only supports theories of mean reversion in expected returns (Fama and French, 1988; Campbell, 2001), but also provides strong evidence that movements in the Street PE are intimately linked to long-run returns. For example, a one-point increase in the Street PE predicts nearly a 5% decrease in returns over the next five years. Given that Street PE ranges from 7 to 28, this suggests that when stocks are at their cheapest, expected returns over the next five years are approximately 105% higher than when they are at their most expensive. Similar results are observed when using the 3-year Street PE. The Street PE consistently outperforms other valuation ratios – PD, CAPE, and GAAP PE – in predictive power for returns. In fact, none of the traditional measures are significant at the 5% level for the 1-year or 3-year horizon, and only the PD is significant at the 5% level for the 5-year horizon.

We conclude that the variation in future returns induced by excess stock price movements can indeed be predicted using the Street PE. Thus, using the Street PE ratio reconciles return predictability test swith the excess volatility puzzle. Our return predictability evidence is all the more remarkable since it shows robust in- and out-of-sample sample predictive power without relying on “theory-motivated” regression frameworks (e.g., Lewellen, 2004; Cochrane, 2008; Campbell and Thompson, 2008) or complex estimation techniques (e.g., Kelly, Malamud, and Zhou, 2024).3

[Authors] study documents that Street earnings are a good fundamental measure for valuing stocks. We show that the Street price-earnings ratio is superior at predicting aggregate returns (both in- and out-of-sample) as well as cross-sectional returns relative to traditional financial ratios. Thus, it is excellently suited for asset pricing tests aimed at understanding stock price and return variation (and hence, the excess volatility puzzle). We also show that its use can reconcile conflicting views in prior research.

[Authors] also construct a measure of “earnings before special items” at the S&P 500 level using Compustat. Panel (A) of Figure 3 shows that this closely replicates the Street earnings report by I/B/E/S. “Earnings before special items” are helpful for the return prediction exercise since I/B/E/S began reporting realized earnings only in 1983. We, therefore, use the “earnings before special items” in the extended sample starting in 1965 (we use annual Compustat for the period 1965 and quarterly Compustat after 1970). [. . .] Panel (C) of Figure 3 shows a more pronounced increase in the PD ratio compared to the Street PE ratio over the past decades.

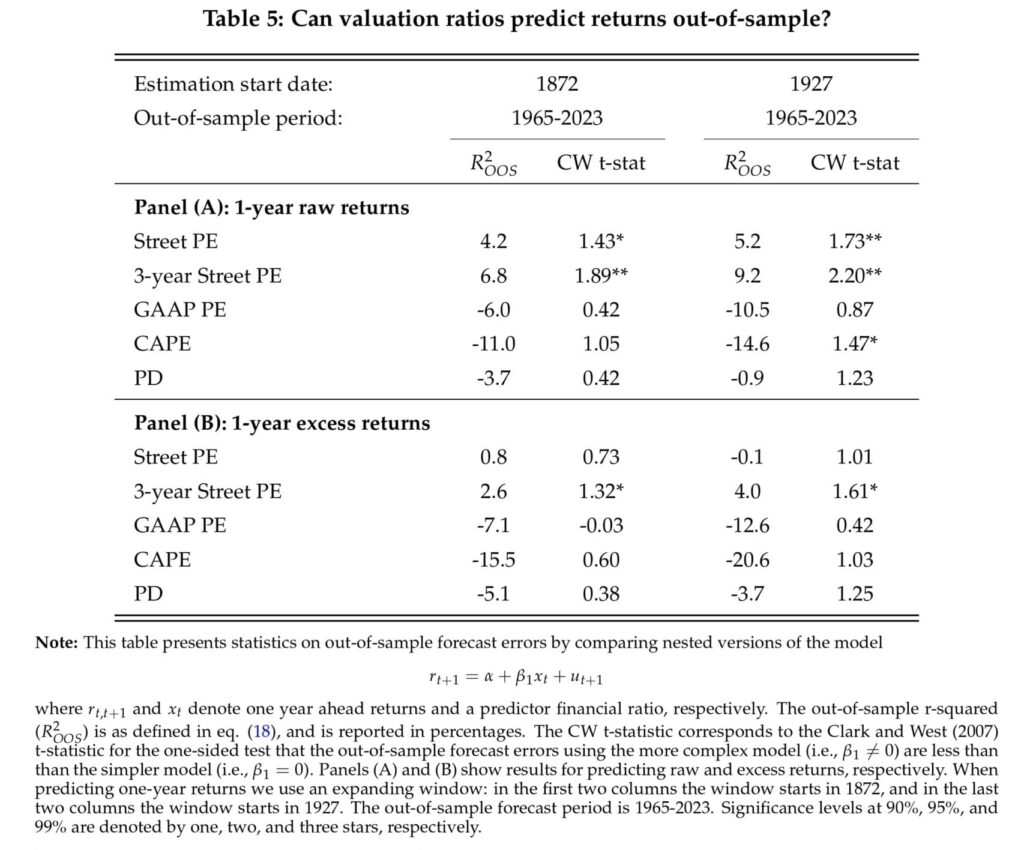

Table 5 reports the results where we report both R2OOS statistic and the CW t-statistic for the null that Clark-West SPE Difference is zero against the alternative that its positive (i.e., the more complex model adjusted for noise performs better). Panel (A) demonstrates that the Street PE and 3-year Street PE ratio have significant predictive power, with R2OOS values of 4.2% and 6.8%, respectively, for the 1872 estimation start date, and 5.2% and 9.2% for the 1927 start date. The corresponding CW t-statistic confirm the significance of these results: all the results are significant at the 5% level with the sole exception of Street PE for the 1872 estimation start, which is still significant at the 10% level. This indicates that these two Street-based valuation ratios are robust predictors of future returns out-of-sample. [. . .] Panel (B) of Table 5 also reports the results for one-year excess returns as in Goyal and Welch (2008). The results are less favorable. However, the Street PE and 3-year Street PE still manage to outperform the other valuation measures.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend