What Can We Extract From the Financial Influencers’ Advice?

Social media are often the main and primary choice of information in almost every area of our lives, and they also influence the financial decisions of retail traders and investors. A lot of people give opinions anywhere on the Internet; some are respected, others are disrespected, some are more well-known, and others obscure. But the power of those people, financial influencers, as a group, is substantial as they create the market sentiment. But what’s the real value of their advice? Can we extract useful information from their opinions?

Swiss Finance Institute Research Paper Series, with the plain name Finfluencers, touches on this topic. The answer to the important question of whether competition among users of social media platforms is such that followers can easily identify skilled and drive out unskilled finfluencers from the market for social information is, unfortunately, no. However, a few interesting tidbits result even in a profitable strategy built upon some findings.

Social media users tend to follow unskilled and antiskilled finfluencers, defined as finfluencers whose tweets generate negative alpha. Antiskilled influencers often achieve the same return and social sentiment momentum, which coincides with the behavioral biases of retail investors who trade on antiskilled finfluencers’ flawed advice. These results are consistent with homophily (“love of sameness,” which is a sociological theory that similar individuals will move toward each other and act in a similar manner), also seen in other social networks and groups, in this case often resulting in the survival of un- and antiskilled finfluencers even though they do not provide valuable investment advice.

One of the profitable applications and proposed strategies is contrarian investing based on going against advice from the tweets by antiskilled influencers, which yields abnormal out-of-sample returns, funnily called by authors “wisdom of the antiskilled crowd.” All in all, these findings shed light on the quality of finfluencers’ unsolicited financial advice and the competition among and economic incentives faced by finfluencers which the SEC has been concerned about.

Authors: Ali Kakhbod, Seyed Mohammad Kazempour, Dmitry Livdan, and Norman Schuerhoff

Title: Finfluencers

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4428232

Abstract:

Tweet-level data from a social media platform reveals low average accuracy and high dispersion in the quality of advice by financial influencers, or “finfluencers”: 28% of finfluencers are skilled, generating 2.6% monthly abnormal returns, 16% are unskilled, and 56% have negative skill (“antiskill”) generating -2.3% monthly abnormal returns. Consistent with homophily shaping finfluencers’ social networks, antiskilled finfluencers have more followers and more influence on retail trading than skilled finfluencers. The advice by antiskilled finfluencers creates overly optimistic beliefs most times and persistent swings in followers’ beliefs. Consequently, finfluencers cause excessive trading and inefficient prices such that a contrarian strategy yields 1.2% monthly out-of-sample performance[.]

And as always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“This paper assesses the quality of investment advice provided by different finfluencers. Using tweet-level data from StockTwits on over 29,000 finfluencers, we classify each finfluencer into three major groups: Skilled, unskilled, and antiskilled, defined as those with negative skill. We find that 28% of finfluencers provide valuable investment advice that leads to monthly abnormal returns of 2.6% on average, while 16% of them are unskilled. The majority of finfluencers, 56%, are antiskilled and following their investment advice yields monthly abnormal returns of -2.3%. Surprisingly, unskilled and antiskilled finfluencers have more followers, more activity, and more influence on retail trading than skilled finfluencers.

[. . .] we investigate the persistence and determinants of users’ skills. To study persistence, we split the sample into two halves and estimate users’ skills separately in each half of the data. We find that while the autocorrelation for the estimated alphas is close to zero and insignificant, all four alternative skill measures exhibit significant persistence. For instance, a one percent increase in the expected true alpha over the first half of the data predicts a 0.09% increase in the expected true alpha over the second half. We then investigate whether users’ tweeting activity determines their skill. We find that skilled finfluencers are less active than unskilled and antiskilled influencers. Users who tweet more frequently are less skilled in that a ten times increase in the total number of tweets posted by a user is associated with a 3.7% decrease in the probability of being skilled and a 0.08% decline in the monthly expected true alpha. Additionally, the tweet composition correlates with the degree of its informativeness as users posting more negative tweets tend to be more skilled. A one percent increase in the share of negative tweets is associated with a 0.01% increase in the expected true alpha and a 0.06% increase in the probability of being skilled.

Following the advice by antiskilled finfluencers creates overly optimistic beliefs most of the time since their tweets tend to be bullish about most stocks, and overly pessimistic beliefs some of the time when their tweets tend to be more pessimistic than the skilled influencers’ tweets. Furthermore, the social media sentiment by antiskilled finfluencers is highly persistent and induces long swings in the magnitude of their followers’ belief bias. More strikingly, one can earn 1.2% monthly out-of-sample buy-and-hold abnormal returns by trading against the antiskilled finfluencers’ advice. When we combine these results with our additional findings that the finfluencers’ skills are persistent but are not sufficient for finfluencers’ survival, we can conclude that on social media platforms “the message is more important than the messenger.” That is as long as there are any antiskilled finfluencers “preaching” their message the investors tend to like their message and are willing to trade on it.

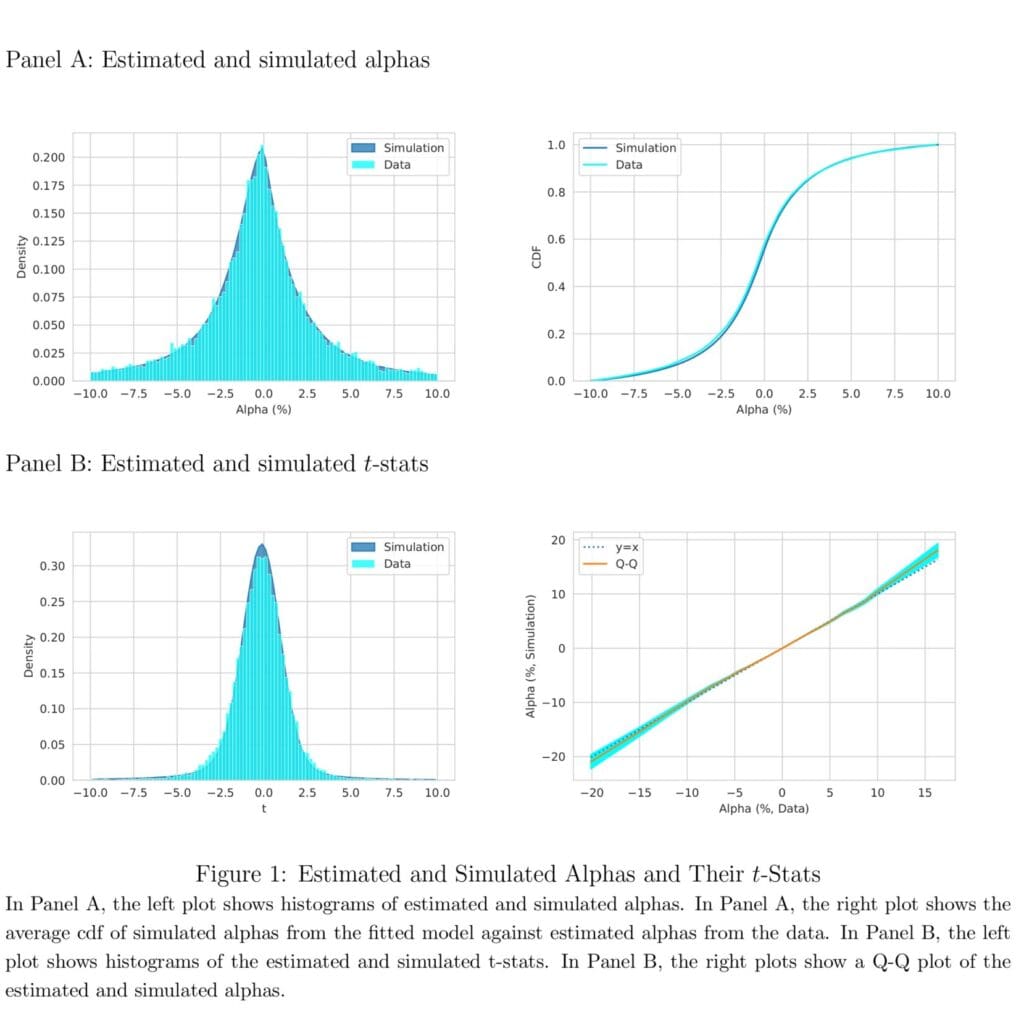

Figure 1 reports the results of several approaches to gauge the goodness of fit. First, we calculate the average pdf and cdf of the simulated samples and plot them against the pdf and cdf of the data. Panel A of Figure 1 shows the results. The distribution of simulated alphas is close to the estimated alphas from the data. To quantify the closeness of the distributions, we run Kolmogorov-Smirnov tests between the estimated alphas from the data and the simulated alphas from each of the simulated samples, using the null hypothesis that the two distributions are equal. The KS test rejects the null at 10%/5%/1% significance levels for 19.20%/7.40%/0.70% of simulations.

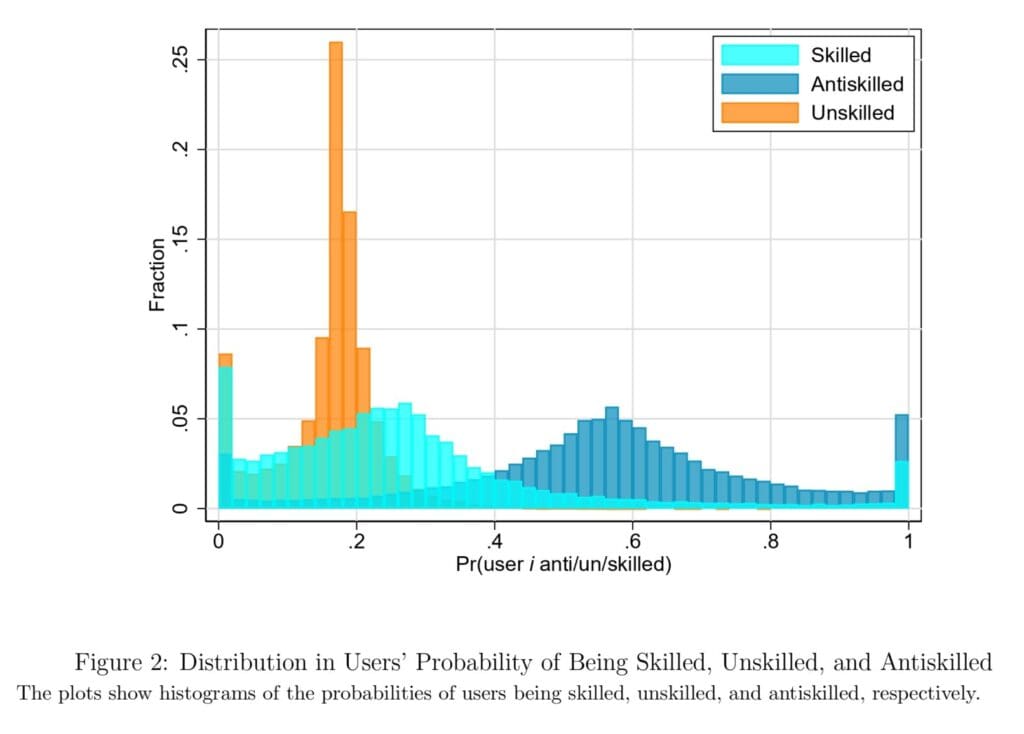

Figure 2 depicts histograms of the probabilities of users being skilled, unskilled, and antiskilled, respectively. The plot shows that there exists a lot of dispersion in the probability of being a skilled or antiskilled StockTwits user. It is evident from the plot that less than 3% of StockTwits users are unambiguously skilled and the first column of Table 3 shows that the majority of StockTwits users have a probability of less than 1/3 of being skilled.

Figure 3 documents the univariate relation between users’ followers and our measures of skill. The three binscatter plots show a strong positive relation between users’ followers, as measured by the log of overall follower count, and the probabilities of being unskilled and antiskilled. The right binscatter plot shows, however, that follower count is negatively related to users’ probability of being skilled.

Table 4 reports the results when we regress the number of followers for each finfluencer on the measures of her skill. The explanatory variables are either the finfluencer’s measured alpha in the data, ˜αi, the expected value of alpha given its measurement in the data, E[αi|˜αi], the probability that a user is skilled, Pr(αi > 0|˜αi), the probability that a user is unskilled, Pr(αi = 0|˜αi), or the probability that a user is antiskilled, Pr(αi < 0|˜αi). The estimates show that neither finfluencers’ measured alpha, ˜αi, nor finfluencers’ expected alpha given its measurement, E[αi|˜αi], has a relation with follower count. Instead, skilled finfluencers have fewer followers than either unskilled or antiskilled finfluencers. Next, we want to understand the economic forces behind the negative relation between the number of followers and skill measures.

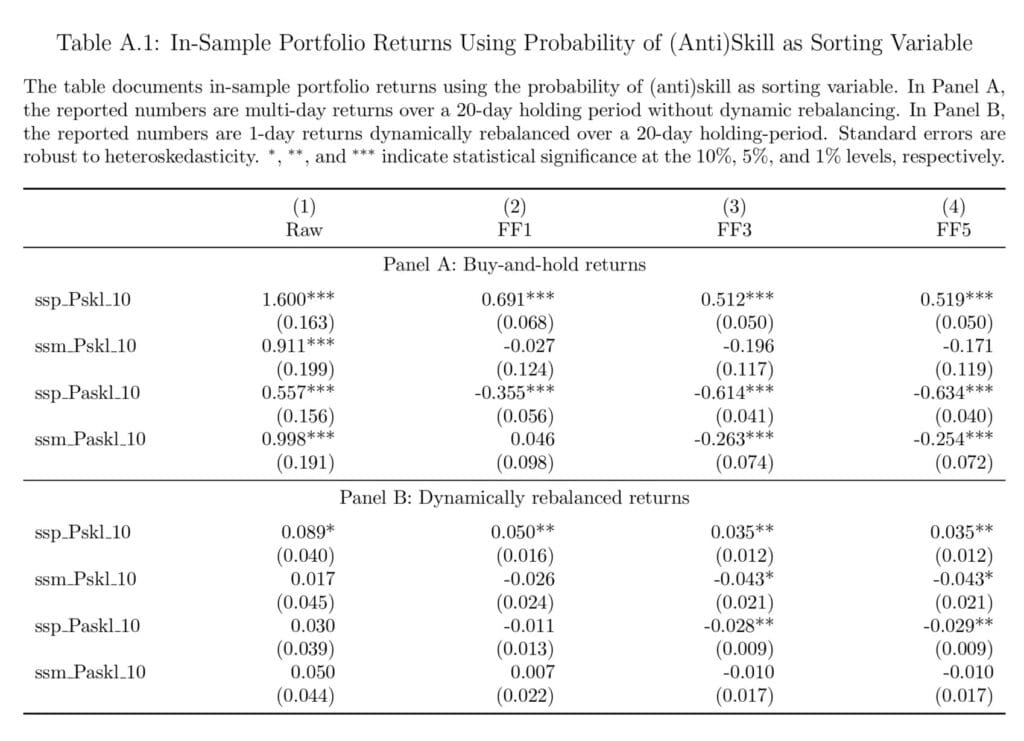

As a robustness check, Table A.1 documents in-sample portfolio returns using the probability of (anti)skill as a sorting variable. In Panel A, the reported numbers are multi-day returns Retbht+1,t+L over a 20-day holding period. In Panel B, the reported numbers are dynamically rebalanced returns Retdyt+1 over a 20-day holding period. The results are broadly in line with Tables 11 and 12.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend