What Drives Crypto Asset Prices?

Cryptocurrencies are no longer just a whim of computer nerds, they are part of the mainstream finance and often accepted part of fixed allocation for an overall diversified portfolio. We will not try to predict, whether they are here to stay in the future or will be subject to failure. This is a topic that has been touched on infinitely. Our interest caught up a purely practical paper by Austin Adams, Markus Ibert, and Gordon Liao, in which the authors apply classic macro-finance principles to identify the impact of monetary policy and risk sentiment in conventional markets on crypto asset prices. So let’s explore their results …

The authors use a structural VAR model identified with sign and magnitude restrictions to investigate the drivers of Bitcoin returns and stablecoin flows. By decomposing price movements into conventional monetary policy shocks, conventional risk premium shocks, crypto adoption shocks, and crypto risk premium shocks, they provide new insights into the factors influencing cryptocurrency markets and their interconnectedness with traditional financial markets.

The findings suggest that crypto-specific factors, namely adoption and risk premium shocks, play a dominant role in explaining the variation in daily Bitcoin returns. While conventional monetary policy and risk premium shocks have some impact on cryptocurrency prices, their influence is more pronounced at lower frequencies. Furthermore, they provide evidence supporting the safe-haven property of stablecoins within the crypto asset space, as stablecoin market capitalization tends to increase during periods of market stress.

The event studies focusing on the COVID-19 market turmoil, the collapse of FTX, and the launch of BlackRock’s spot Bitcoin ETF further validate these findings; case studies highlight the importance of crypto-specific factors in driving cryptocurrency prices and flows during significant market events.

The research, finally, has several intriguing implications for market participants and policymakers:

- Investors should know the distinct factors driving cryptocurrency prices and their potential diversification relative to traditional asset classes.

- Research provides a methodology to understand the direction and magnitude of risk spillovers in new asset classes. The estimates can be used for investor hedging and prudential risk monitoring.

Future research could extend that analysis by incorporating a more comprehensive range of cryptocurrencies and exploring the impact of regulatory changes on cryptocurrency markets. Developing more sophisticated models that capture the time-varying nature of the relationships between cryptocurrencies and traditional asset classes could provide further insights.

Authors: Austin Adams, Markus Ibert, and Gordon Liao

Title: What Drives Crypto Asset Prices?

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4910537

Abstract:

We investigate the factors influencing cryptocurrency returns using a structural vector auto-regressive model. The model uses asset price co-movements to identify the impact of monetary policy and risk sentiment in conventional markets on crypto asset prices, with minimal reverse spillover. Specifically, we decompose daily Bitcoin returns into components reflecting conventional risk premia, monetary policy, and crypto-specific shocks. We further decompose the crypto-specific shocks into changes in crypto risk premia and levels of crypto adoption by exploiting the co-movement of Bitcoin with stablecoin market capitalization. Our analysis shows that crypto asset prices are significantly impacted by conventional risk and monetary policy factors. Notably, contractionary monetary policy accounted for over two-thirds of Bitcoin’s sharp decline in 2022. In contrast, since 2023 the compression of crypto risk premia has been the predominant driver of crypto returns, independent of the buoyant equity market backdrop. Our findings highlight the importance of identifying drivers of crypto returns and understanding crypto’s evolving relationship with traditional financial markets.

As always, we present several exciting figures and tables:

Notable quotations from the academic research paper:

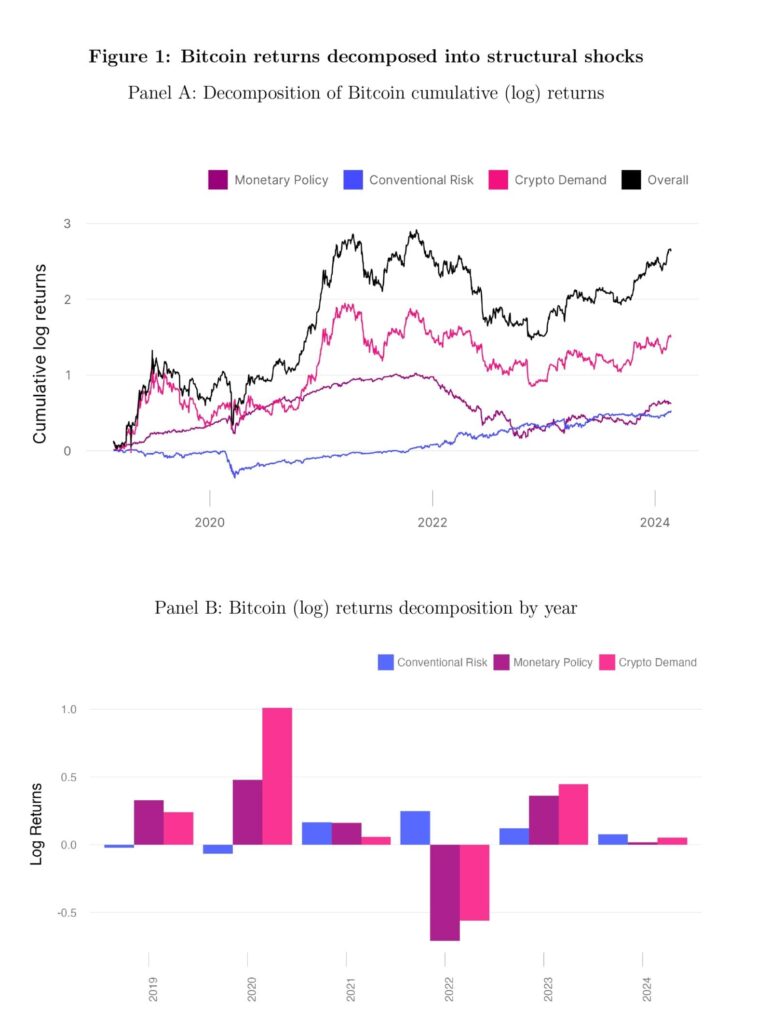

“This paper aims to shed light on the drivers of crypto assets through the lens of a sign-restricted vector auto-regressive (VAR) model. Figure 1 illustrates our approach’s usefulness in decomposing Bitcoin returns into three structural shocks: conventional monetary policy shocks, conventional risk premium shocks, and crypto-specific demand shocks. The figure shows the decomposition both cumulatively from 2019 to 2024 (Panel A) and year-by-year (Panel B).

The figure [1] shows Bitcoin returns decomposed into three structural shocks: monetary policy shocks, conventional risk premium shocks, and crypto demand shocks. The decomposition uses the median-target solution of a structural vector-autoregressive model identified with sign and magnitude restrictions.

Figure 2 plots the paths of cumulative shocks for the model with three structural shocks. The figure shows both the cumulative shocks for the MT solution as well as the median of cumulative shocks across all retained solutions. The median-target solution is generally close to the median of cumulative shocks across all retained solution, suggesting that the optimization in Equation (3) works well. The figure also shows the 95th and the 5th percentiles of the distribution of cumulative shocks. These are generally close to the median-target solution, suggesting that model uncertainty is not a primary concern.

The figure [2] shows cumulative shocks over time. Shocks are a monetary policy shock (positive is contractionary), a conventional risk premium shock (positive is risk-off), and a crypto (Bitcoin) demand shock. The figure shows the median-target solution (in black) of a structural vector-autoregressive model identified with sign and magnitude restrictions, as well as the median across solutions (in purple) and the 5th and 95th percentiles across solutions (in grey).

We illustrate that most of the daily variation in Bitcoin returns is unexplained by conventional risk premium shocks and monetary policy shocks in Figure 4. The figure shows a variance decomposition of daily Bitcoin returns into the three shocks and shows that crypto demand shocks account for more than 80% of the variability in Bitcoin daily returns. This confirms the notion that Bitcoin is a volatile asset whose variability cannot be explained by shocks that drive conventional assets. The low-frequency impact of monetary policy is further highlighted in Table 3 that shows a quarterly-to-daily variance ratio of 1.8 for the monetary policy factor while less than unity for the other two factors. A variance ratio of greater than 1 indicates positive autocorrelation (Lo and MacKinlay, 1988) and possible arbitrage.5

The figure [4] shows the fraction of the daily variance of 2-year Treasury yields (2Y Bonds), S&P 500 returns, and Bitcoin returns explained by monetary policy, conventional risk premium, and crypto (Bitcoin) demand shocks.”

Interest in digital assets continues to rise as more individuals explore simple entry points into cryptocurrency investment. For newcomers, promotional bonuses and referral offers have become an accessible gateway to building a starting balance without financial risk. Many platforms now reward verified users with small token amounts to encourage participation in the crypto market. Accessing free crypto through these signup promotions introduces individuals to trading tools, verification systems, and asset management processes.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend