What Drives Volatility of Bitcoin?

Extremely high Bitcoin returns and drawdowns come hand in hand with significant volatility. As Bitcoin is becoming an unignorable part of finance with substantial institutional participation, it is necessary to understand the key drivers of returns and volatility, which is comparably persistent as in other, more established asset classes. In addition, other cryptocurrencies are extremely correlated with Bitcoin, so understanding of key drivers of Bitcoin volatility might also carry to other cryptos. For example, if you buy xrp, ethereum, litecoin, or other altcoins, then you should understand that its volatility will often be affected by the volatility of Bitcoin. The research of Lyócsa, Molnár, Plíhal and Širaňová (our colleague from Slovak Academy of Sciences) examines several possible drivers of the volatility. The authors study the realized volatility and its jump component and identify whether the volatility is influenced by various factors such as news about the regulation of bitcoin, hacking attacks on bitcoin exchanges, investor sentiment, and various types of macroeconomic news. The study identifies the significant impact of two intuitive factors: news about the regulation or cryptocurrency exchange hacks. Lagged volatility is also an essential factor, as shown by regression analysis. Regarding macroeconomic data, economic fundamentals do not seem to influence the volatility, except for forward-looking indicators (e.g., the consumer confidence index). Lastly, the authors study the investor sentiment extracted from Google searches, but only the positive sentiment has some impact. Overall, the research is a vital addition to the literature that helps us understand Bitcoin’s volatility.

Authors: Štefan Lyócsa, Peter Molnár, Tomáš Plíhal and Mária Širaňová

Title: Impact of macroeconomic news, regulation and hacking exchange markets on the volatility of bitcoin

Link: https://www.sciencedirect.com/science/article/pii/S0165188920301482

Abstract:

We study whether news and sentiment about bitcoin regulation, the hacking of bitcoin exchanges and scheduled macroeconomic news announcements affect the volatility of bitcoin, measured as realized variance and its jump component. Our results show that realized variance and its jump component exhibit similar dynamics and react similarly to various types of news. Volatility of bitcoin reacts most strongly to news on bitcoin regulation, positive investor sentiment regarding bitcoin regulation extracted using Google searches, and most notably, hacking attacks on cryptocurrency exchanges. Quantile regression reveals that hacking attacks have particularly strong impact on the upper conditional distribution of bitcoin volatility. We also find that the volatility of bitcoin is not influenced by most scheduled US macroeconomic news announcements, such as government budget deficits, inflation, or even monetary policy announcements. On the other hand, bitcoin responds with increased volatility to announcements of forward-looking indicators, such as the consumer confidence index.

As always we present interesting tables:

Notable quotations from the academic research paper:

“In this paper, we study the drivers of bitcoin price volatility and its jump component. The role of a broad set of macroeconomic news announcements has not yet been explored in the existing literature. The existing literature has already considered that monetary policy announcements might play an important role in this respect. For example, Corbet et al. (2017) report a statistically significant response in bitcoin volatility, while Vidal-Tomäs and Ibanez (2017) show otherwise. Bouri et al. (2018) identifies significant sources of bitcoin volatility stemming from other financial markets.

We fill the gap in the literature by studying the role of scheduled macroeconomic news announcements in eight eco- nomic categories: consumption, forward-looking indicators, government spending, investments, import-export, monetary policy, prices, and real economic activity. Moreover, we also explore the role of an important class of variables for bitcoin price formation; namely, news related to regulation, sentiment and the hacking of exchange markets. We find that, systematically, the bitcoin-to-US-dollar exchange rate realized volatility responds only to scheduled news announcements related to forward-looking indicators.

Second, news related to potential or implemented regulatory policies increases the observed realized volatility. Specifically, we proxy for the news related to regulation by scanning through articles in the Financial Times newspaper. Next, we find that on the day prior to the publication of news related to the regulation of bitcoin, the volatility of bitcoin increases. Third, we find that bitcoin volatility declines when positive sentiment (derived from Google searches) with regard to bitcoin, cryptocurrencies and regulation increases.

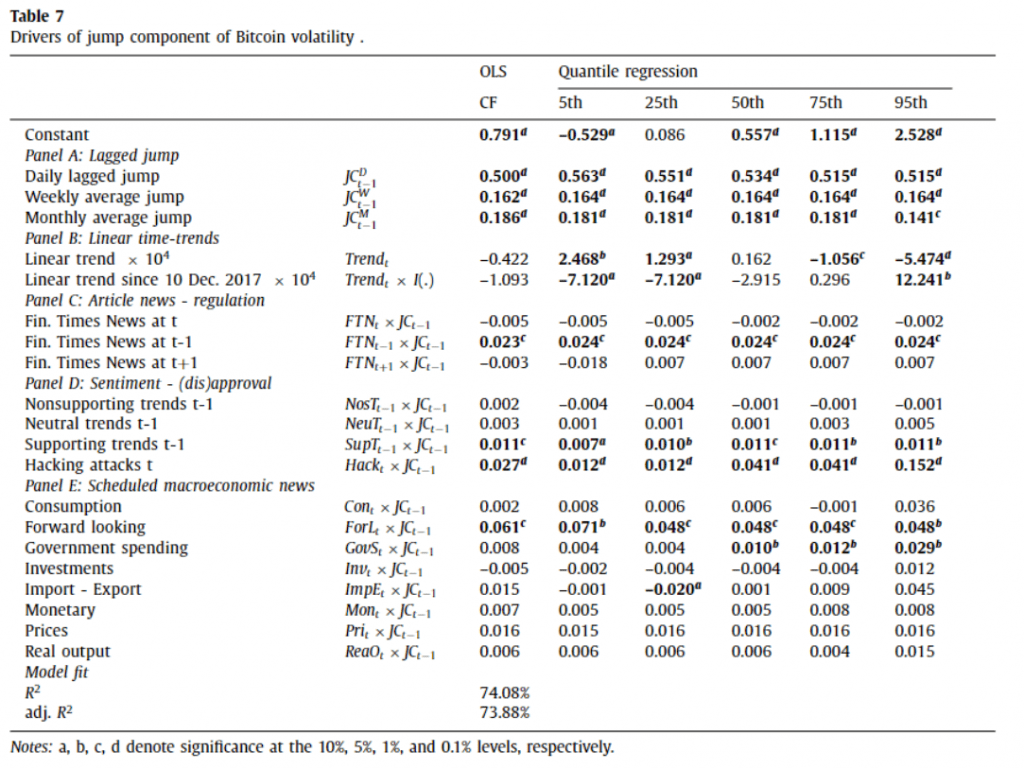

Fourth, hacking services related to cryptocurrencies, such as the hacking of cryptocurrency exchanges, leads to increased volatility. These results suggest that hacking is a unique risk factor when pricing bitcoin investments. A particularly large effect is observed for the right tail of the volatility distribution, i.e., the hacking of cryptocurrency exchanges has the potential to lead to extremely volatile periods. Fifth, the jump component has drivers very similar to those of the realized volatility, while news items related to regulation and, particularly, hacking exchange markets have a potentially massive impact on the price formation of the bitcoin.

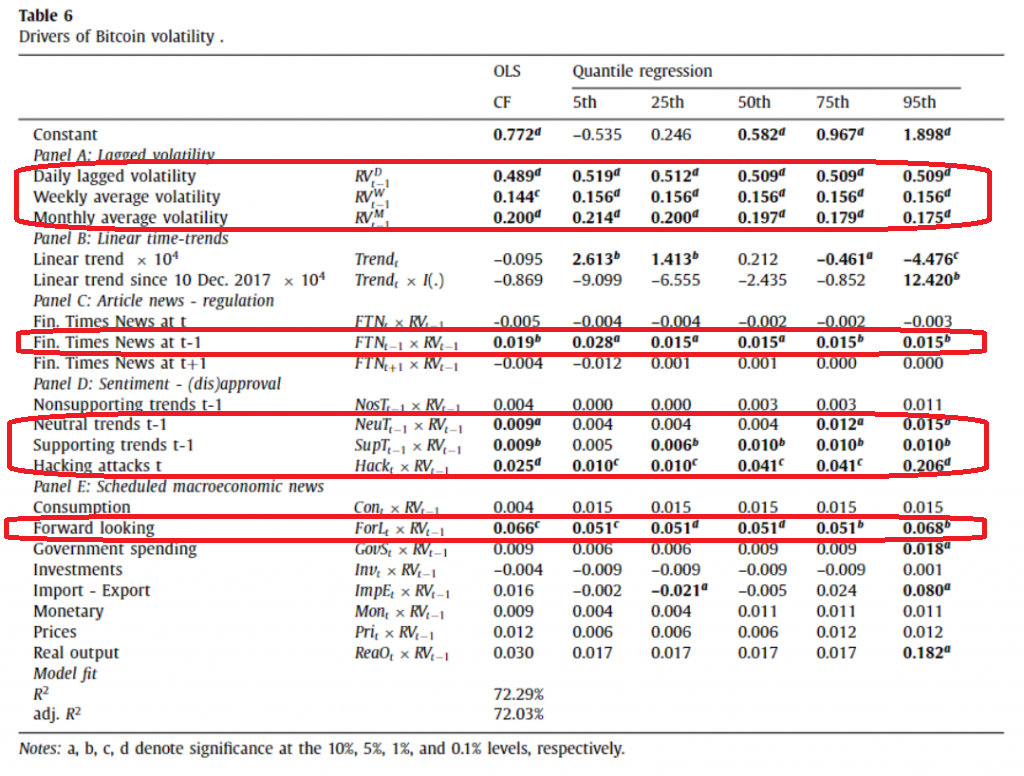

The linear time trend (see Panel B) indicates that, on average, the overall level of volatility has not changed over time. However, the quantile regressions reveal that the lower quantiles of volatility have increased over time (2.613 and 1.413 at the 5 th and 25 th percentiles, respectively), while higher quantiles of volatility distribution have decreased over time ( −0 . 461 and −4 . 476 at the 75 th and 95 th percentiles, respectively). Moreover, according to our model, the introduction of derivatives has only led to an increase in the extreme quantiles of volatility distribution.

Financial Times articles have a systematic effect on the next day’s realized volatility of the bitcoin price series. The estimated coefficient of 0.019 ( F T N t−1 variable) can be interpreted as a 1.9% increase in realized volatility compared to the previous day’s level of volatility. The quantile regression results show that the news articles have almost two times stronger impact on lower quantiles of volatility. Hacks of cryptocurrency exchanges have a potentially explosive effect driving high levels of volatility (Panel D). The es- timated coefficient from the OLS model is 0.025, and that for the conditional 5 th percentile model is 0.01, while it is 0.206 for the 95 th percentile of the realized volatility. The differences in these estimated coefficients suggest that cryptocurrency hacking events have the potential to lead to periods of extremely high volatility, as the corresponding coefficient is more than 20 times larger for the conditional 95 th quantile of volatility than for the 5 th quantile. The coefficient 0.206 corre- sponds to a 2.72% increase in realized volatility when the average value of the Hack t variable is considered and 0.06% when the median value is used.

Controlling for sentiment also appears to have merit (Panel D). Neutral sentiment, which can be interpreted as a general attention, increases the overall level of realized volatility as well as the supporting (positive) sentiment. The results across quantiles show that the effects tend to increase for extreme quantiles. For example, positive sentiment increases the ex- pected right-tail volatilities more than it increase left-tail volatilities. These results show that a positive attention toward cryptocurrencies actually tends to increase the level of volatility.

The role of macroeconomic news announcements is explored in Panel E, where news announcements are interacted with lagged realized volatility. We find that only releases of forward-looking components tend to systematically lead to realized volatility on the market. This finding does not come as a surprise, as most of the empirical studies consistently highlight the rather speculative nature of bitcoin, which is more sensitive to exogenous market disturbances (crashes, regulations) or factors influencing its use as medium of exchange in black market transactions and tax avoidance. The effect seems to be larger for extreme quantiles.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend