Who Profits from Prediction Markets?

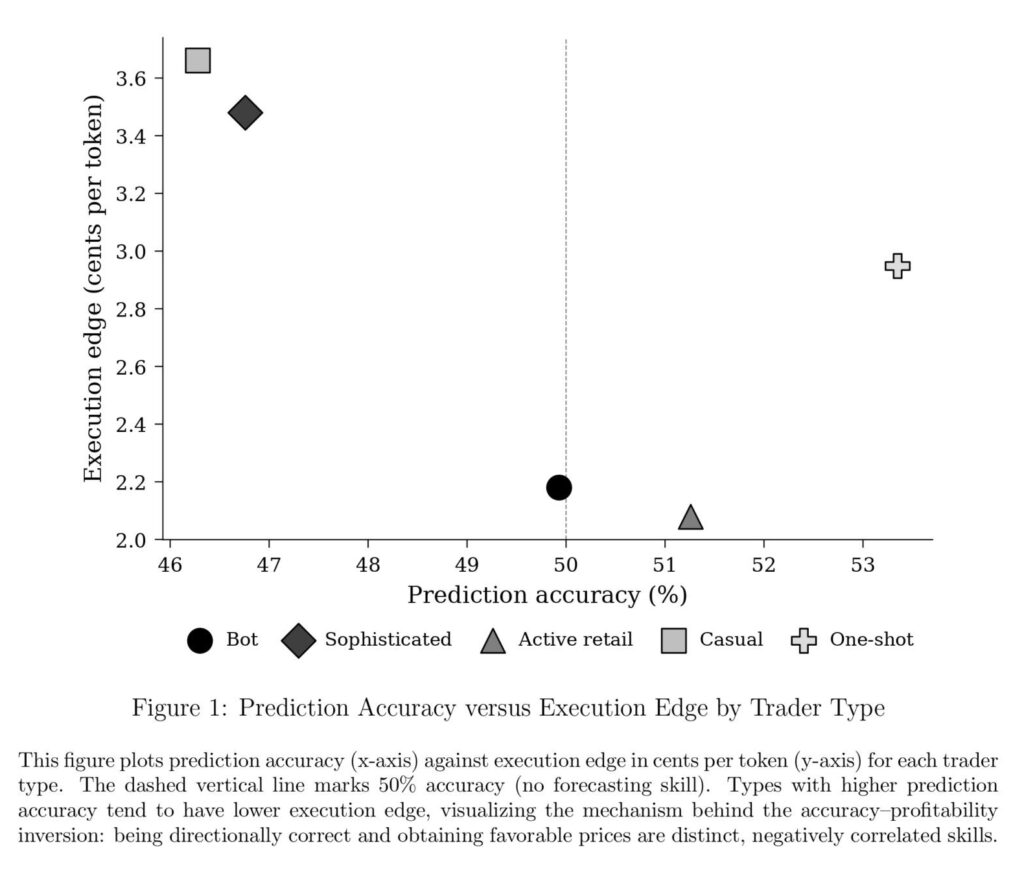

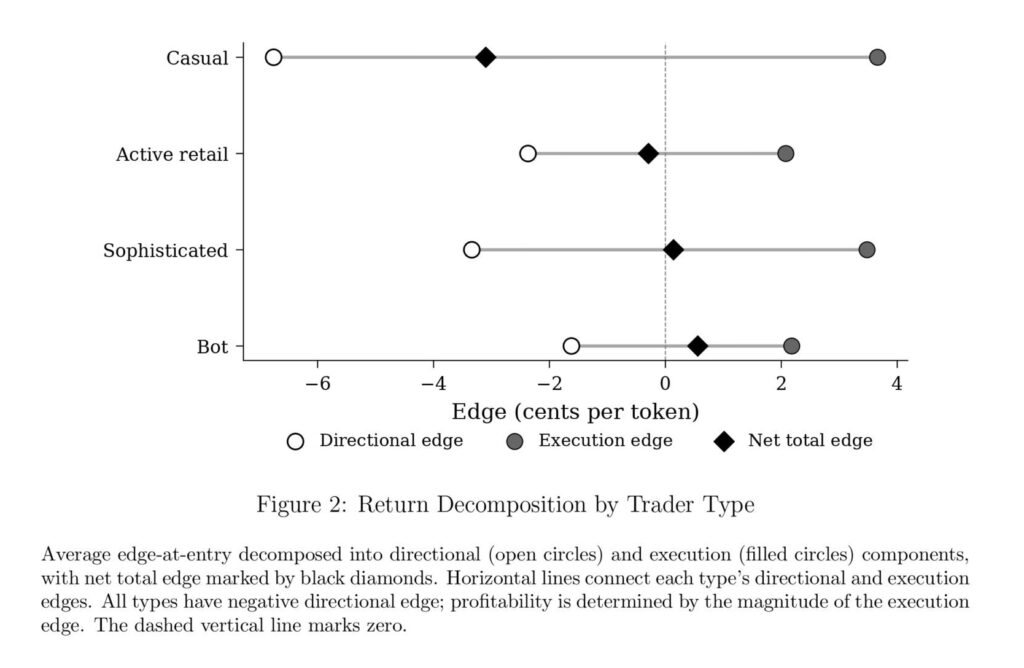

In the high-stakes arena of prediction markets, a counterintuitive pattern emerges: retail traders who correctly pick winners more than half the time still lose money, while automated traders with coin-flip accuracy pocket nine-figure profits. Using 222 million prediction market trades with directly observable terminal payoffs, the paper “Who Profits from Prediction? Execution, Not Information” presents a clean answer to why it is so. The authors decompose trader returns into a directional component and an execution component, revealing that the execution component, not the directional component, determines which trader types earn positive returns.

The intuition behind the results is surprisingly simple. In prediction markets, being “right” is often not enough to make money. What matters is the price at which you enter the trade. Buying a contract at $0.50 and correctly predicting the outcome 55% of the time can be highly profitable. Buying the same contract later at $0.85 requires extraordinary accuracy just to break even, since you are risking $0.85 to make only $0.15. The study shows that many retail traders actually predict outcomes correctly more often than not, but they tend to enter too late — after prices have already adjusted and most of the opportunity has disappeared.

The real edge therefore comes from execution rather than forecasting skill. The most profitable participants are not necessarily the best predictors; they are the traders who consistently avoid paying the spread, provide liquidity through limit orders, and enter markets early before price discovery is complete. Automated traders (bots) excel precisely in these dimensions. On average, bots entered positions more than eight days before contract resolution, while casual retail traders entered only about three days before expiration. Roughly 70% of the bots’ advantage came simply from superior timing during the market lifecycle, while the remaining edge came from spread capture and better order execution. In practice, this means bots were acting more like market makers than directional speculators.

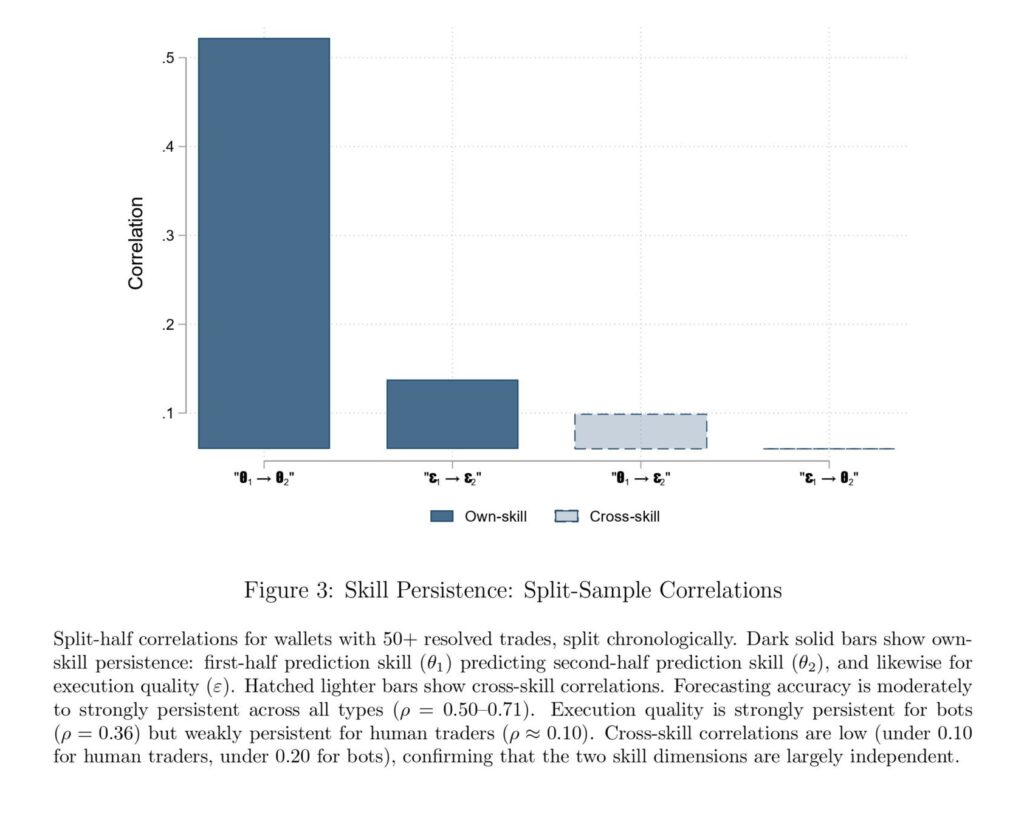

Perhaps the most important takeaway for traders is that forecasting skill and execution skill appear to be almost completely unrelated. Traders who were more accurate were not more profitable, because their higher accuracy usually came from trading after information had already been incorporated into prices. The market had effectively “priced in” their correct prediction before they entered the trade. The paper therefore argues that in highly competitive and fast-moving markets, execution quality — patient order placement, liquidity provision, and early positioning — dominates raw prediction ability as the primary source of trading profits.

Authors: Joshua Della Vedova

Title: Who Profits from Prediction Markets? Execution, not Information

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6191618

Abstract:

Retail prediction market traders pick winners 51.3% of the time yet lose money; automated traders achieve coin-flip accuracy yet earn $133 million. Decomposing 222 million trades with observable terminal payoffs into directional and execution components, we show the two are nearly independent, with shared variance under 1% for human traders. No trader type beats the price-implied accuracy benchmark; execution timing determines profitability. The conventional VWAP benchmark produces a spurious negative correlation and understates execution persistence fivefold. Forecasting execution separability replicates in 14.1 million CBOE equity option contracts; the accuracy-profitability inversion does not, confirming it requires single-margin settings.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“We decompose trading skill into two dimensions, forecasting accuracy (picking the right side) and execution quality (getting a favorable price), and show that these dimensions are nearly independent. Execution, not forecasting, determines which traders profit. Automated traders on the world’s largest prediction market achieve 49.9% directional accuracy, no better than a coin flip, yet they are the only participants who make money, earning $133 million in aggregate profits. The one-dimensional view cannot generate this pattern; the two-dimensional view predicts it.

[E]xample illustrates the paper’s central decomposition. Every trade has a directional component (did the trader pick the right side?) and an execution component (did the trader get a favorable price?). The $0.85 trader wins on direction; the $0.50 trader wins on execution, capturing $0.50 per correct prediction rather than $0.15. Direction determines which side to take; execution determines whether taking it is profitable. A human who reads political polls has no inherent advantage in order placement speed; a bot optimized for spread capture has no inherent advantage in predicting elections.

[Authors] test the framework’s boundary predictions using 14.1 million CBOE equity option contracts classified by exchange-assigned origin code. The two-dimensional framework predicts that θ-ε separability should generalize across market structures, but the accuracy profitability inversion should break down in settings where traders exploit multiple margins of skill. Both patterns appear in the options data: the separability and negative within type correlation replicate despite continuous payoffs and private information, but in options, where traders choose direction, strike, and expiration, accuracy and profitability move together rather than apart.

The mechanism operates through execution timing: accurate forecasters arrive after prices have already moved toward terminal values, paying an execution penalty that more than offsets their directional advantage. The same two-dimensional structure replicates in 14.1 million CBOE equity option contracts through a different channel (adverse selection pricing rather than timing), confirming the theory’s prediction that θ-ε separability generalizes across market structures.

Policies targeting information asymmetry alone, the focus of most market regulation, may miss the execution channel through which retail losses accumulate when price discovery is fast. Best-execution obligations and execution quality reporting address the relevant margin, but as the benchmark sensitivity analysis shows, measuring execution quality requires a decomposition that is itself sensitive to the choice of fair-price benchmark; conventional VWAP-based measures conflate the two dimensions they aim to separate.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend