Full vs. Synthetic Replication and Tracking Errors in ETFs

The growth of passive investing and ETFs is indisputable. Consequently, this boom also affects financial markets (e.g., market elasticity or by creating predictable buys and sells) and assets that ETFs track. Even though all passive ETFs aim to replicate some benchmark index, there are two distinct approaches to doing so. The first approach is directly replicating the benchmark (by buying underlying assets) either by full direct replication or sampling. The second approach consists of synthetic replication using derivatives – most commonly by total return swaps (or futures).

The investor is interested primarily in the tracking error (and perhaps in counterparty risk in synthetic ETFs), which is the leading research topic for the novel paper by Zheng (2021). Since synthetic replication is more spread in Europe, the author examines equity and fixed-income ETFs during 2001-2020 and studies how the replication method affects the tracking error.

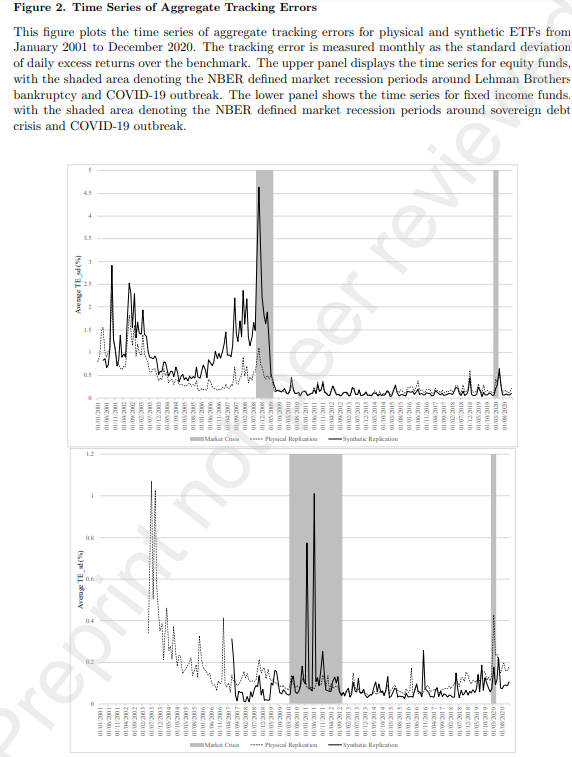

The first finding is that there is no significant difference in the tracking ability across the whole sample period. However, the global financial crisis was a structural break, after which the tracking errors were reduced. The synthetic equity ETFs seem to have a better tracking ability and lower sensitivity to market turbulence after the crisis. Additionally, synthetic ETFs have more substantial tracking errors after a sudden increase in counterparty risk but are less affected by liquidity shocks than physically replicated ones. The author has also identified that there have been crucial improvements in risk management of swap counterparty risk over the past decade.

Overall, the paper offers several insights and an essential comparison of physical and synthetic ETFs. Understanding the synthetic ETFs can be crucial for investors since it is commonly utilized to track less liquid or developed markets and appears to be more tax-efficient.

Author: Xinrui Zheng

Title: Does the Replication Method Affect ETF Tracking Efficiencies?

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3962470

Abstract:

Using 2,290 European equity and fixed income ETFs from 2001 to 2020, this paper studies how replication method affects the tracking efficiencies of ETFs, especially during market crisis. There is no persistent evidence suggesting superior tracking performance of synthetic ETFs relative to physically-replicated ones. I identify 119 indices simultaneously tracked by both physical and synthetic ETFs, and conduct difference-in-difference analysis around Lehman Brothers bankruptcy, sovereign debt crisis, and COVID-19 outbreak. Synthetic ETFs face steeper declines in tracking efficiencies after a sudden increase in counterparty risk, but they are shielded from liquidity shocks. There is a remarkable drop in the sensitivity of tracking performance to market distress measures after the global financial crisis.

As always we present several interesting figures and tables:

Notable quotations from the academic research paper:

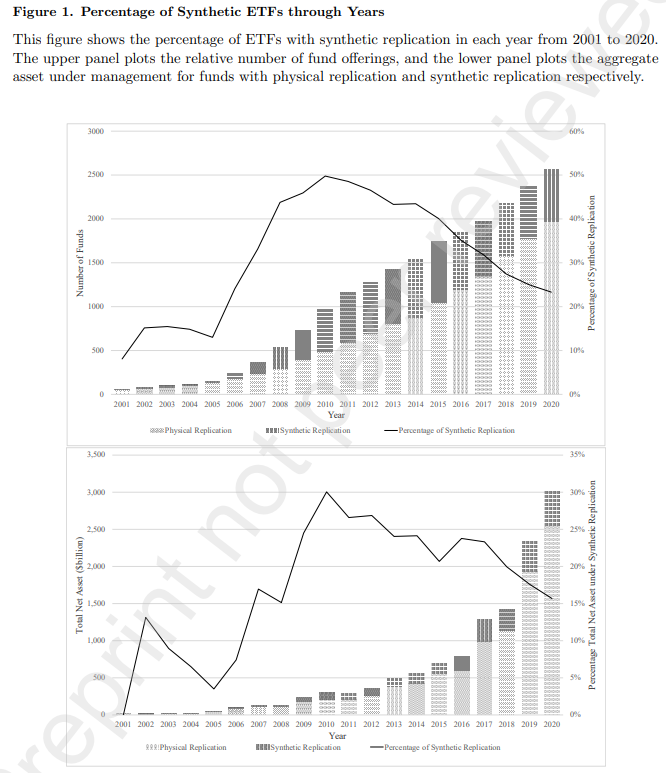

“The market share of synthetic ETFs reaches its peak in 2010, representing 50% of the total number of ETF offerings in Europe and 30% of aggregate assets under management. However, despite the exponential growth in ETF assets, the market share of synthetic ETFs has been shrinking in the past decade. By the end of 2020, synthetic ETFs represent only 23% in number and 17% in total net asset (TNA) of European ETFs. After the global financial crisis, synthetic ETFs has been widely criticized by regulators and financial advisors for their complexity, lack of transparency and counterparty risk. However, there is a resurgence in interest for synthetic ETFs, particularly those providing exposure to the US equity market due to their tax advantage over their physical peers (Zarate et al., 2021).

Do synthetic ETFs posses superior tracking ability compared to physically-replicated ones? Second, which replication method can better withstand market distress? Third, is there any improvement on risk management after the global financial crisis, especially in terms of the swap counterparty risk of synthetic ETFs? In this paper, I find no evidence of persistent superior tracking ability of synthetic ETFs across the sample period, especially after controlling for heterogeneity across the investment objectives. There are significant cross-sectional variations in tracking errors. Furthermore, after the global financial crisis, I observe a large reduction in tracking errors. Synthetic ETFs face steeper declines in tracking efficiencies after a sudden increase in counterparty risk. But during liquidity shocks, their tracking ability is less affected relative to the physical ones. I explain the relative tracking performance between physical and synthetic replication around market crisis by describing the trade-off between counterparty and liquidity risk that dominates the market. Finally, I find that the tracking performance of both physical and synthetic ETFs becomes significantly less sensitive to market distress after the global financial crisis. Specifically, synthetic equity ETFs demonstrate superior tracking ability in terms of both lower tracking errors and lower sensitivity to market turbulence in the post-crisis period.

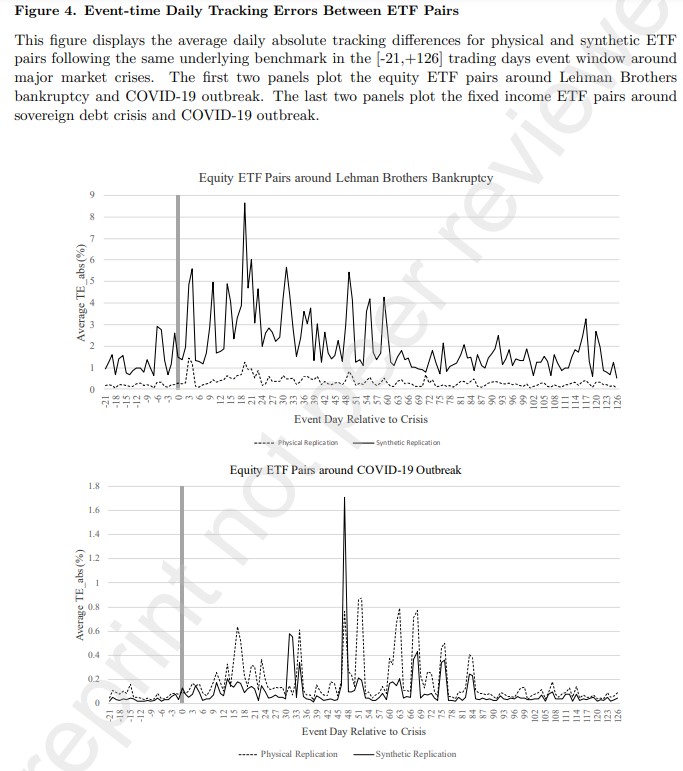

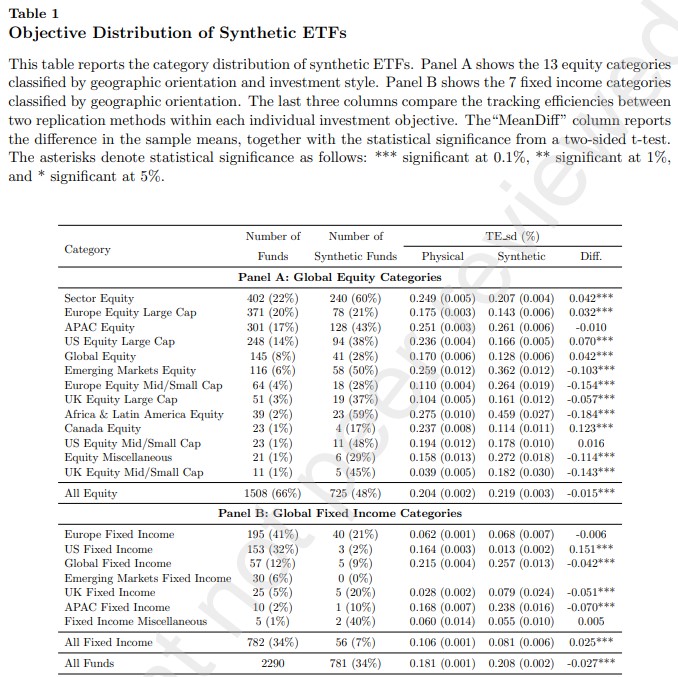

Unlike the previous work, I account for the significant time-series and cross-sectional variations in tracking errors, which largely reconcile the inconsistencies in the literature. There is a structural break in the level of tracking errors after the 2008 global financial crisis, especially among equity ETFs. Cross-sectionally, funds with high return volatility and poor past performance are associated with higher tracking errors. Although a synthetic structure is applied more commonly in less liquid or less developed markets, I find no persistent relation between the liquidity or efficiency of an objective market and the relative tracking efficiencies. To address the second research question, I identify 119 physical and synthetic ETF pairs that have the same underlying benchmark, and conduct a difference-in-difference (DiD) analysis. Previous literature documents higher tracking errors for all ETFs during crisis periods characterized by large bid-ask spreads, small trading volumes, and high volatility of currency

and exchange rates (Buetow and Henderson, 2012; Johnson et al., 2013).

In this paper, I disentangle the impact of extreme market movements on ETFs with different replication methods. Results from the DiD analysis suggest that equity (fixed income) ETFs with synthetic structures experience larger declines in tracking efficiencies around Lehman Brothers’ bankruptcy (sovereign debt crisis). However, synthetic ETFs fared better during the COVID-19 market shock in 2020, compared to their physical equivalents. Therefore, I relate the different tracking ability between physical and synthetic ETF pairs during extreme market turbulence to the trade-off between liquidity risk and counterparty risk.

This paper contributes to the literature from three perspectives. First, this paper disentangles the effect of market distress on ETF tracking efficiencies. Difference in tracking performance deterioration around market crisis between ETFs with physical and synthetic replication is attributed to their different reactions to counterparty risk and liquidity risk. Second, the extensive 20-year sample period allows identification of several physical and synthetic ETF pairs tracking the same underlying benchmarks, and therefore a like-for-like comparison across different types of major market crisis. To my best knowledge, this is the first paper to make a direct comparison of ETFs with different replication methods on the same underlying index. Third, I identify a structural break in both the level and sensitivity of market-wide tracking efficiencies after the global financial crisis, and provide empirical evidence on how market failure evokes tighter risk management.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend