How Retail Loses Money in Option Trading

Over the last few years, we may have noticed a significant growth in retail investing. No surprise, the COVID pandemic outbreak increased the numbers even more, and undoubtedly, options trading is no exception. According to the authors (de Silva, Smith, Co), retail traders seek options expecting spikes in volatility and, for that reason, incline toward firms with more media coverage. Furthermore, their trading increases around the time of firms’ earnings announcements. Thus, the authors examined the connection between retail option demand and expected announcement volatility (EAV). They found that retail traders seem unwilling to close their option positions following high EAV earnings announcements, which increases their losses. However, bidding up option prices is the main reason for retail losses, supported by enormous bid-ask spreads in options ahead of high EAV announcements. On the other hand, market makers make up another active group around earnings announcements, offsetting retail investors’ positions. As a result, market makers benefit from the behavior mentioned above, which causes a large flow of money from retail to market makers.

Authors: Tim de Silva, Kevin Smith and Eric C. So

Title: Losing is Optional: Retail Option Trading and Earnings Announcement Volatility

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4050165

Abstract: We document the growth of retail options trading over time and provide evidence that retail investors are drawn to options by anticipated spikes in volatility. Using data on options trades by clientele groups, we show retail investors concentrate their trading around firms’ earnings announcements and incur large losses from bidding up prices for options of firms whose announcements are expected to trigger greater abnormal volatility. Retail losses from bidding up prices are compounded by enormous bid-ask spreads in options ahead of high expected volatility announcements. Retail investors also appear reluctant to close options after announcements with high expected volatility despite volatility quickly subsiding post-announcements. Jointly, these effects translate to retail losses of 5-to-9% around earnings announcements on average, and 10-to-14% for high expected volatility announcements. Market makers are the primary beneficiaries of these patterns, particularly in recent years coinciding with the COVID pandemic, resulting in large capital flows from retail to market makers.

As always we present several interesting figures:

Notable quotations from the academic research paper:

„To help motivate our focus on retail behavior around earnings announcements, we begin by documenting several empirical regularities present in our sample:

- The extent of retail trading in options has grown substantially over time, increasing more than ten-fold over the past decade in terms of dollar volume traded.

- For all clientele groups, option trading activity concentrates around firms’ quarterly earnings announcements relative to non-announcement periods.

- Retail investors and market makers are the most active clientele groups around earnings announcements, with market makers largely offsetting positions by retail investors.

These patterns indicate that retail trade is likely an increasingly important determinant of both retail traders’ wealth and option prices around earnings announcements.

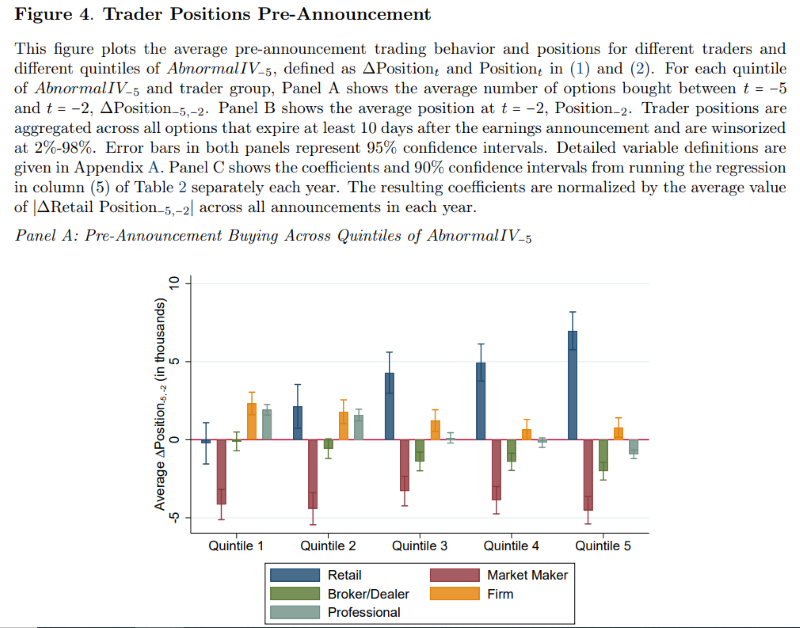

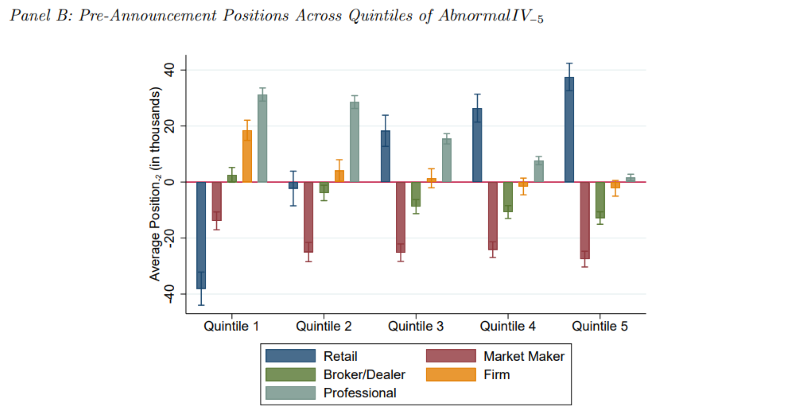

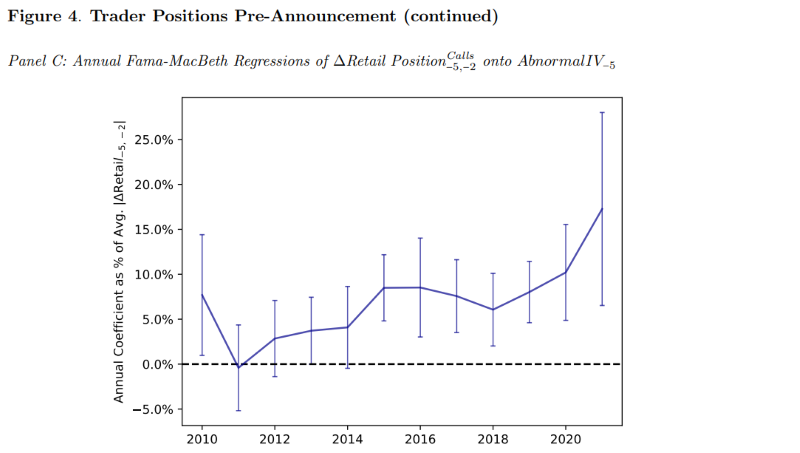

Our first set of tests explore the link between retail option demand and the extent of expected abnormal announcement volatility (EAV). These tests are motivated by prior evidence that retail tends to gravitate towards firms with more media coverage (e.g., Barber and Odean 2008) and that the media is more likely to cover earnings announcements with larger anticipated spikes in volatility (e.g., Noh, So, and Verdi 2021). Combined with theories and evidence of investors’ preference for volatile assets (e.g., Baker, Bradley, and Wurgler 2011; Barberis and Xiong 2012), we predict retail investor option demand increases with the amount of volatility expected at the announcement.

A second key finding to explain the dynamics of option prices is that retail traders appear reluctant to close their option positions following high EAV earnings announcements. This reluctance increases in the extent of losses borne by retail investors, suggesting that behavioral preferences (i.e., a disposition effect) contribute to this pattern. Notably, retail investors hold open these option positions despite post-announcement volatility being statistically indistinguishable between high and low EAV announcements. Thus, the delay in retail closing their positions does not seem to be driven by rational post-announcement hedging motives in which high EAV announcements are followed by persistent elevated volatility.

Using both of these approaches, we show that in the days leading up to high EAV announcements, retail investors take large net long positions. This ramp up of retail demand is concentrated in firms with pre-announcement media coverage, suggesting attention effects strongly contribute to pre-announcement retail option demand. A potential alternative explanation for our findings is that retail investors are attracted to high EAV announcements because of a preference for positively-skewed, i.e., lottery-like payoffs.

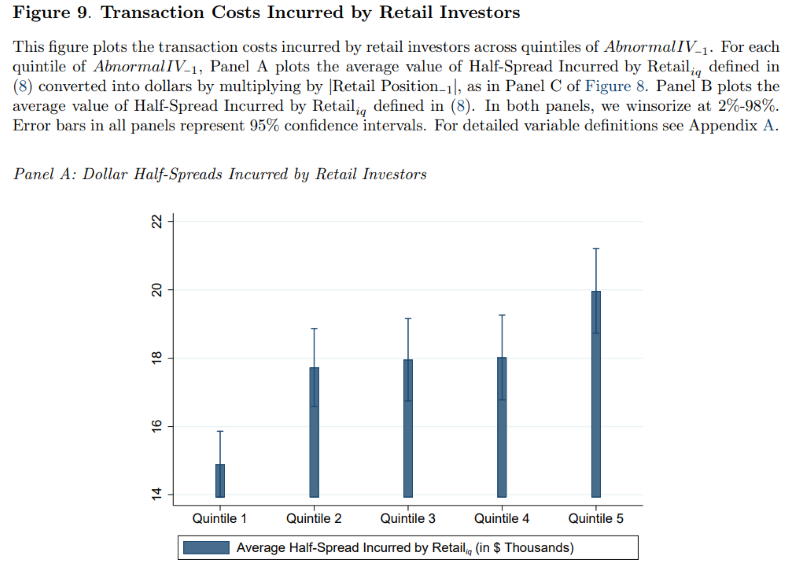

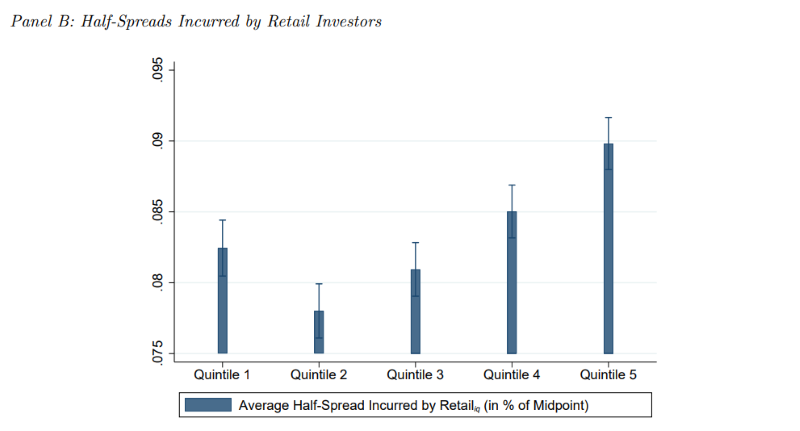

Retail losses predictability concentrate in the subsample of high EAV announcements. Before accounting for transaction costs, retail investors collectively lose roughly $60,000, or 10% of their investment, during the 10 days following the average high EAV announcement. This amounts to $1.5 billion flow of capital away from retail investors during our sample window, and the gains primarily accrue to market makers. Retail losses from bidding up option prices are compounded by enormous bid-ask spreads in options ahead of high EAV announcements. Average bid-ask spreads in our sample amount to a whopping ∼ 20% of the option price and increase further ahead of the high EAV announcements where retail investors concentrate their trades. This increase in spreads is intuitive and consistent with increased information asymmetry leading up to these high-uncertainty events.“

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend