How Wise is the Crowd in Prediction Markets

Authors: Deleep, Avaneesh and Lee, John and Bai, Jenny and Suresh, Dhruv and Dhawan, Harsh

Title: How Wise is the Crowd? Bias and Edge in Prediction Markets

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6322678

Abstract:

Prediction markets are increasingly relied upon as real-time probability oracles, yet their predictive signals remain polluted by structural inefficiencies. While prior literature documents anomalies like the favorite-longshot bias at an aggregate level, the microstructural origins of these distortions—specifically, who generates and exploits them—remain unstudied in modern ecosystems. To investigate this, we engineer a scalable, multi-threaded data architecture capable of synchronously ingesting and persisting tick-level order flow, decentralized wallet histories, and user commentary across Polymarket and Kalshi.

As ever, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“Prediction markets are increasingly relied upon as real-time probability oracles, yet their predictive signals remain polluted by structural inefficiencies. While prior literature documents anomalies like the favorite-longshot bias at an aggregate level, the microstructural origins of these distortions—specifically, who generates and exploits them—remain unstudied in modern ecosystems.

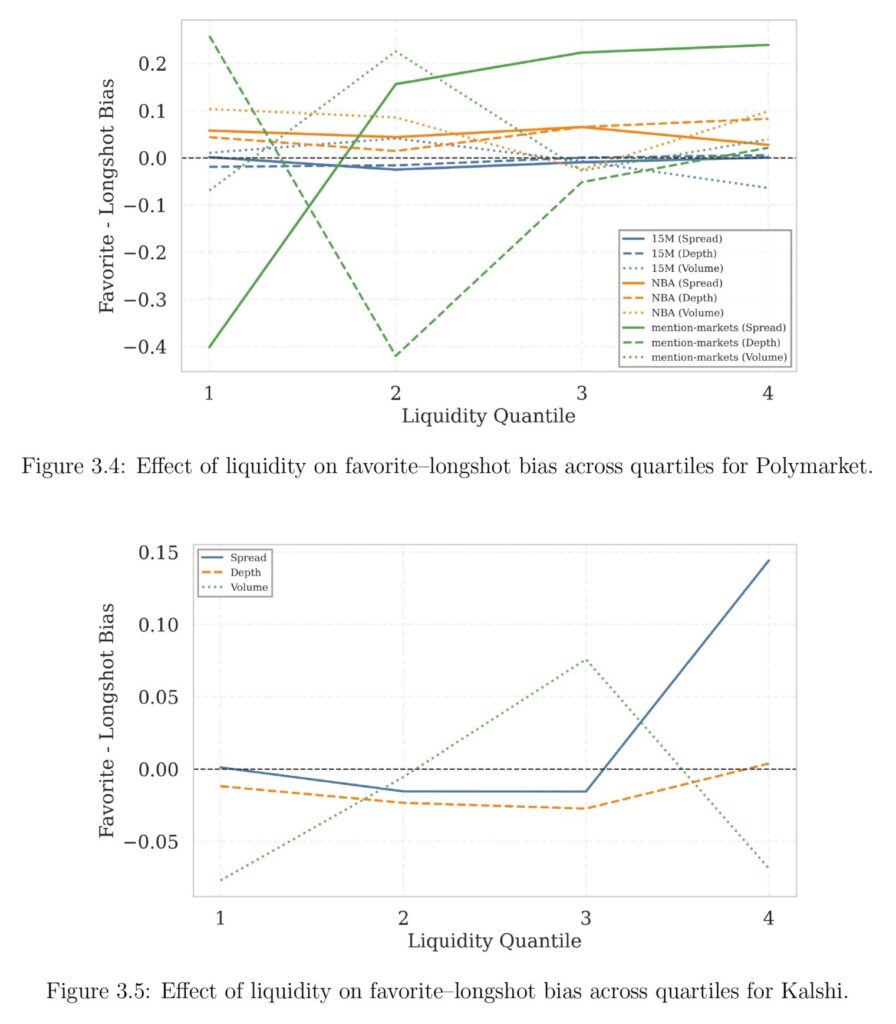

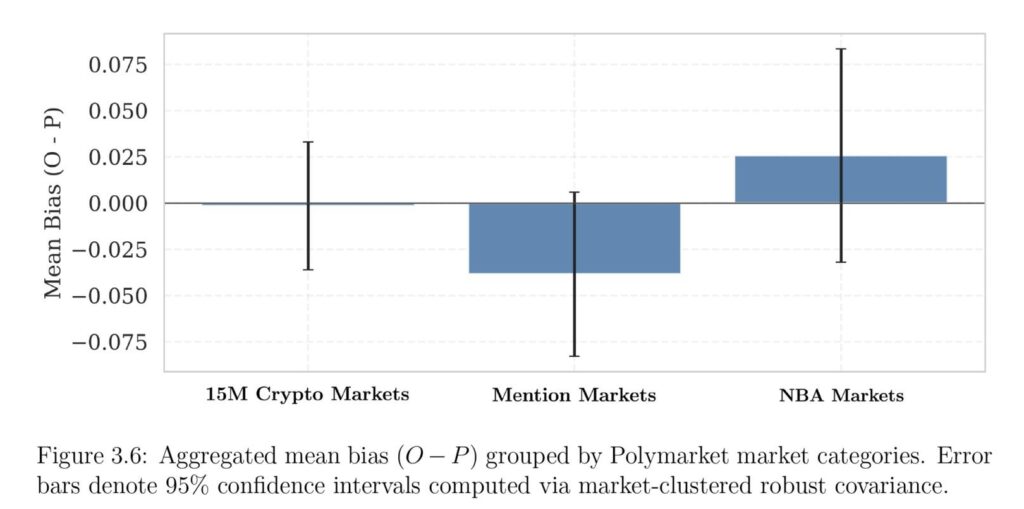

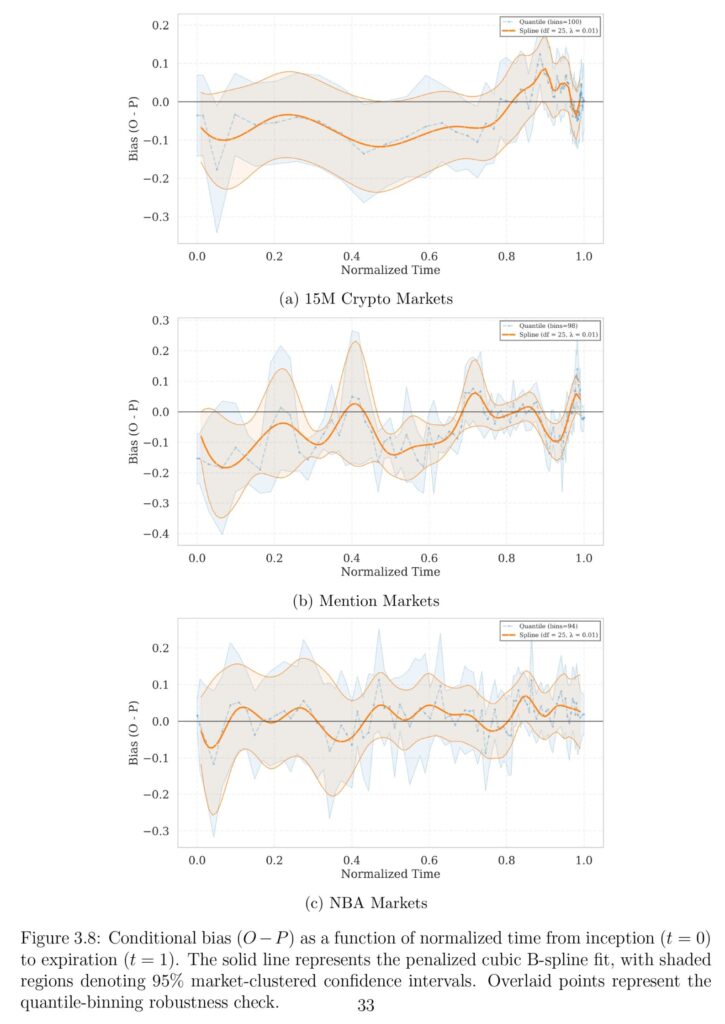

The Apparent Illusion of the Favorite-Longshot Bias: Our preliminary univariate analysis suggested the presence of a classic favorite-longshot bias in Mention Markets. However, by deploying multivariate penalized splines to control for the confounding effects of contract lifecycle timing, we reveal this to be a statistical artifact. Instead, these markets exhibit a pervasive “Yes Bias,” whereby participants consistently overpay for the “Yes” outcome — that is, the contract that pays off if the reference event occurs — relative to the corresponding “No” outcome.

Furthermore, we find that “Whales”, or the most capitalized players, are not the most sophisticated. By dynamically reconstructing participant positions, we demonstrate that Whales, on average, systematically bleed expected value to small-order traders. Rather than acting as sharp informed players, these large actors likely trade on ideological conviction, structurally overpaying for specific narratives and suffering from adverse selection against smaller participants.

We find no statistically significant correlation between sentiment intensity and informational edge, indicating that the most prominent voices in these ecosystems function primarily as sources of communicative noise.

Ultimately, this research provides a reproducible methodology for actively denoising prediction market probabilities by adjusting for temporal lifecycles, liquidity environments, and the ideological biases held by heavily capitalized, unsophisticated traders.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend