Quantpedia in April 2024

Hello all,

Welcome again to Quantpedia’s monthly recapitulation.

Firstly, a few words about the Quantpedia Awards 2024 competition. Our submission process for the best quant/algo trading research paper of the year 2024 ended on the 30th of April. Quantpedia’s team has processed papers, and the final ten have been sent to our committee for the next stage – ranking. We will list the whole top 10 and who will get a share of the $15.000 prize pool in the second half of May. Stay tuned, and we will announce more soon …

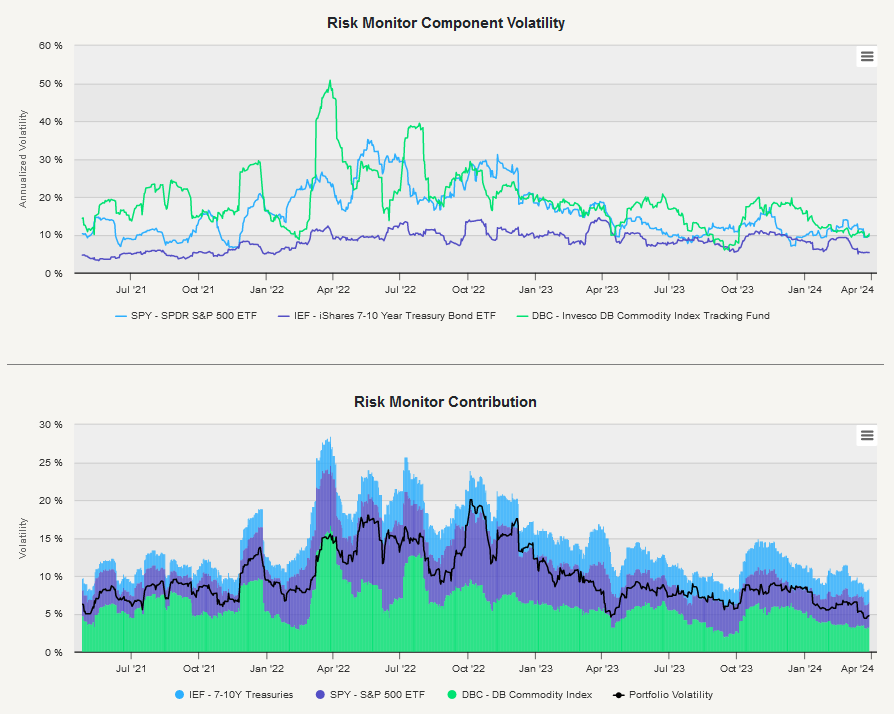

Secondly – a new Quantpedia Pro development – the Risk Monitor Report allows our users to supervise risk in the individual components of the Model Portfolio. In the first part, the report displays the rolling 20-day volatility of individual portfolio components and their contribution to the total portfolio risk.

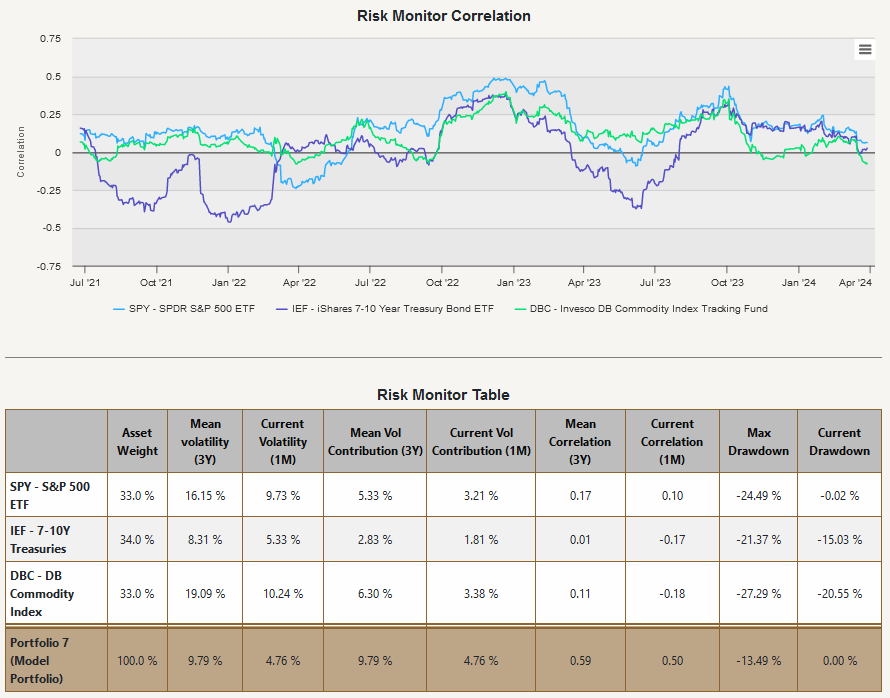

The volatility is not the only variable that contributes to the risk; therefore, afterward, the next chart shows the development of the rolling 3-month correlation of the individual components over time. At the end of the report, the summary table presents important metrics for individual components and for the portfolio as a whole – mean and current volatilities, contributions, mean and current correlations, and current + maximal drawdowns..

Thirdly, we would like to spread the word about the interesting product from our partner vBase, that have built a lightweight solution for making financial signal data, backtests, strategies, etc., more trustworthy and thus more valuable by making them auditory point-in-time and transparently tracking relevant metadata. We are actively researching the integration of their time-stamping into the backtested strategies.

And as usual, let’s also quickly recapitulate Quantpedia Premium development:

- 11 new Quantpedia Premium strategies have been added to our database

- 11 new related research papers have been included in existing Premium strategies during the last month

- 8 new backtests were written in QuantConnect code. Our database currently now contains nearly 770 strategies with out-of-sample backtests/codes.

Additionally, 5 new research articles were published on the Quantpedia blog in the previous month:

Private vs. Public Investment Strategies

Author: Xiang Xu

Title: Private vs. Public Investment Strategies: Reported and Real-World Performance

ESG Investing during Calm and Crisis Periods

Authors: Henk Berkman and Mihir Tirodkar

Title: ESG Investing During Calm and Crisis: Implied Expected Returns

Can Google Trends Sentiment Be Useful as a Predictor for Cryptocurrency Returns?

Authors: Lukas Zelieska and Cyril Dujava

Title: Can Google Trends Sentiment Be Useful as a Predictor for Cryptocurrency Returns?

Impact of Business Cycles on Machine Learning Predictions

Authors: Li Rong Wang, Hsuan Fu, and Xiuyi Fan

Title: Stock Price Predictability and the Business Cycle Via Machine Learning

FX Carry + Value + Momentum Strategies over Their 200+ Year History

Authors: Joseph Chen

Title: Currency Investing Throughout Recent Centuries

Yours …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend