Quantpedia Introduces 3rd Party Factors

Every year, Quantpedia’s team investigates thousands of academic research papers to bring you the most promising ideas from the academic world. We read papers, identify ideas and backtest them to build our unique database. As a result, we have already identified hundreds of factors and built tools to help you orient better in the broad universe of trading strategies and systematic investment factors.

And now, we are opening the possibility to all external researchers, quants, and portfolio managers to contribute to Quantpedia.

So, do you have your own factor, trading strategy, or investment model? Is it backed by solid whitepaper/article? Would you like to show your expertise, increase your visibility and present your work to Quantpedia’s professional readers?

Then help us find you and let us know because we are looking exactly for you!

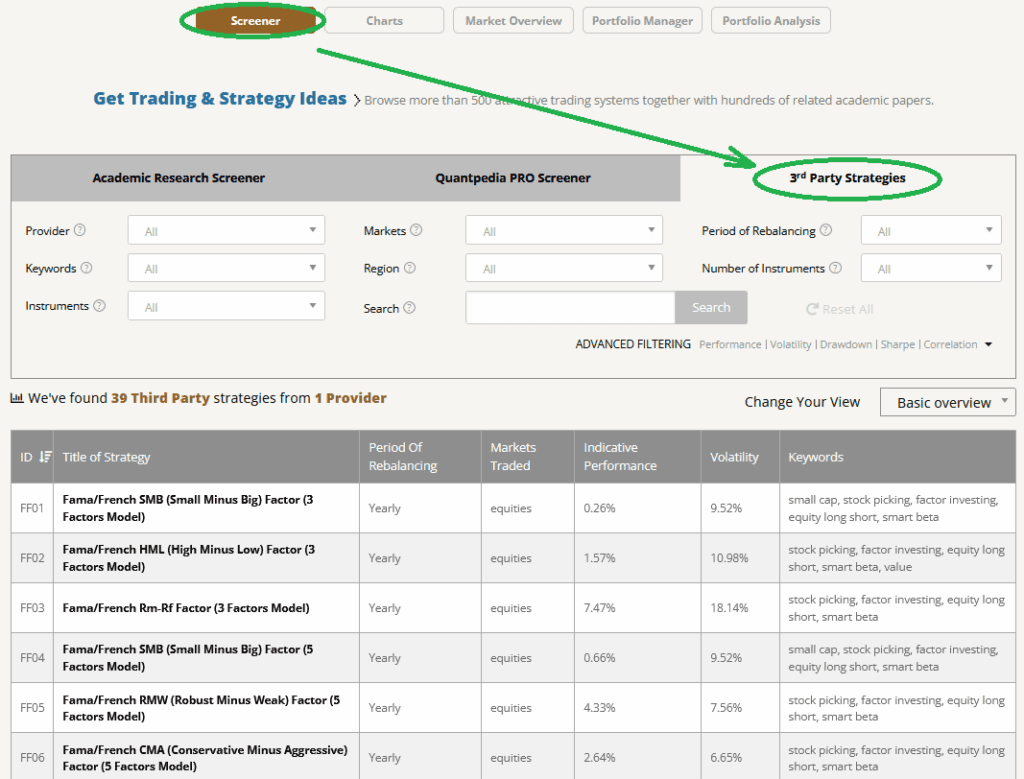

We will place your factor/strategy as a custom 3rd party strategy into Quantpedia Pro. All Quantpedia Pro users will be able to screen for your factor/strategy and test it in their model portfolios.

There are just two hard rules that must be met if any 3rd party researcher/quant would like to show their factor/strategy to Quantpedia Pro’s audience:

1. Your factor must be completely transparent. It means that your factor must be explained in an academic paper (or article), and trading rules must be stated in plain language. Article/paper should be available and accessible on the internet. Do you want an example? See Meb Faber’s papers on SSRN or see Quantpedia’s blogs in which we describe trading models (for example, 1, 2, or 3).

2. Your factor/strategy must have a daily data granularity. It doesn’t mean that you must update your data/factor every day (you can do it weekly/monthly/quarterly, or even yearly). But your factor/strategy must have daily performance data points. We do not need your actual trading code or know your trades. We just need you to make for us accessible your factors/strategy equity curve in the form of daily performance bars. This public information is interesting to all your potential clients/readers and is also interesting for us.

And that’s all.

It will cost you nothing to list your work as 3rd party strategy/factor in Quantpedia Pro. We will link your work and website. We will do our work and integrate your strategy’s/factor’s equity curve into Quantpedia Pro. And we will increase the visibility of your work.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend