Reconstructing a Century of U.S. Corporate Bonds

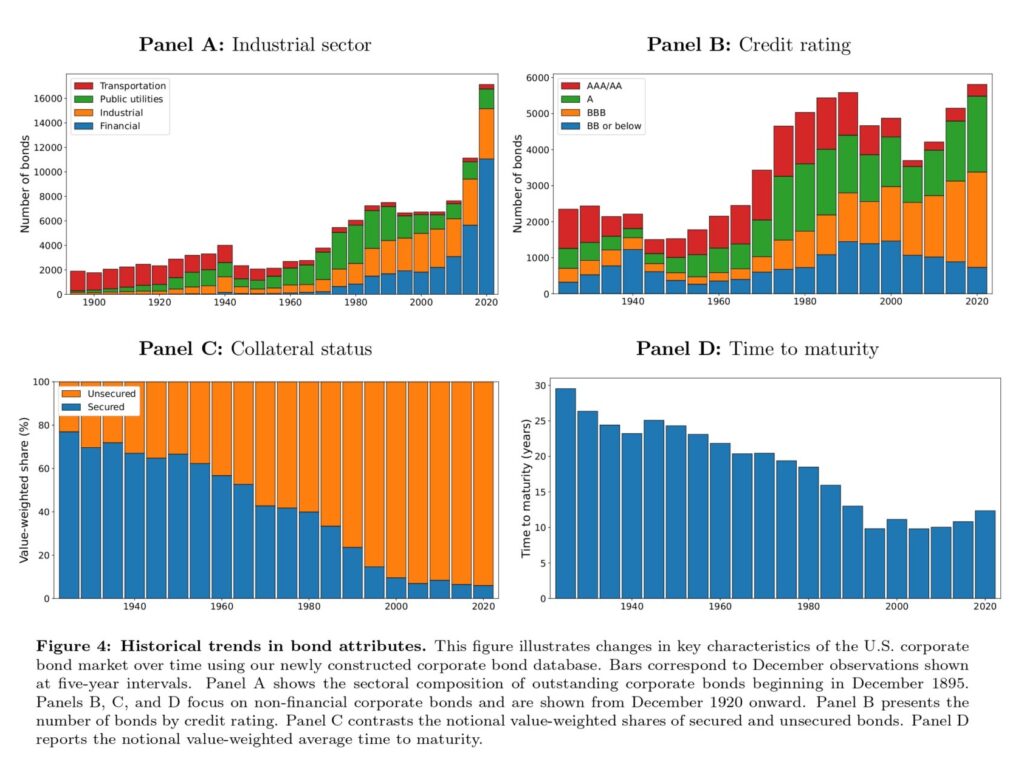

How much do we really know about corporate bond returns before the modern data era? Until recently, the answer was: not enough. Most empirical work in corporate bond pricing has relied on relatively short samples, especially the post-2002 TRACE period, leaving open the question of whether observed risk premia are robust over longer horizons. Ghaderi, Plante, Roussanov, and Seo (2026) Ghaderi, Plante, Roussanov, and Seo (2026) address this limitation by constructing a historical database of U.S. corporate bond returns from 1895 to 2022. Using hand-collected monthly bond quotes from sources such as the Commercial and Financial Chronicle, Standard & Poor’s Bond Guide, and Mergent/Moody’s Bond Record, they assemble a large panel of corporate bonds that allows for a much longer view of credit risk, return predictability, and factor pricing in fixed income.

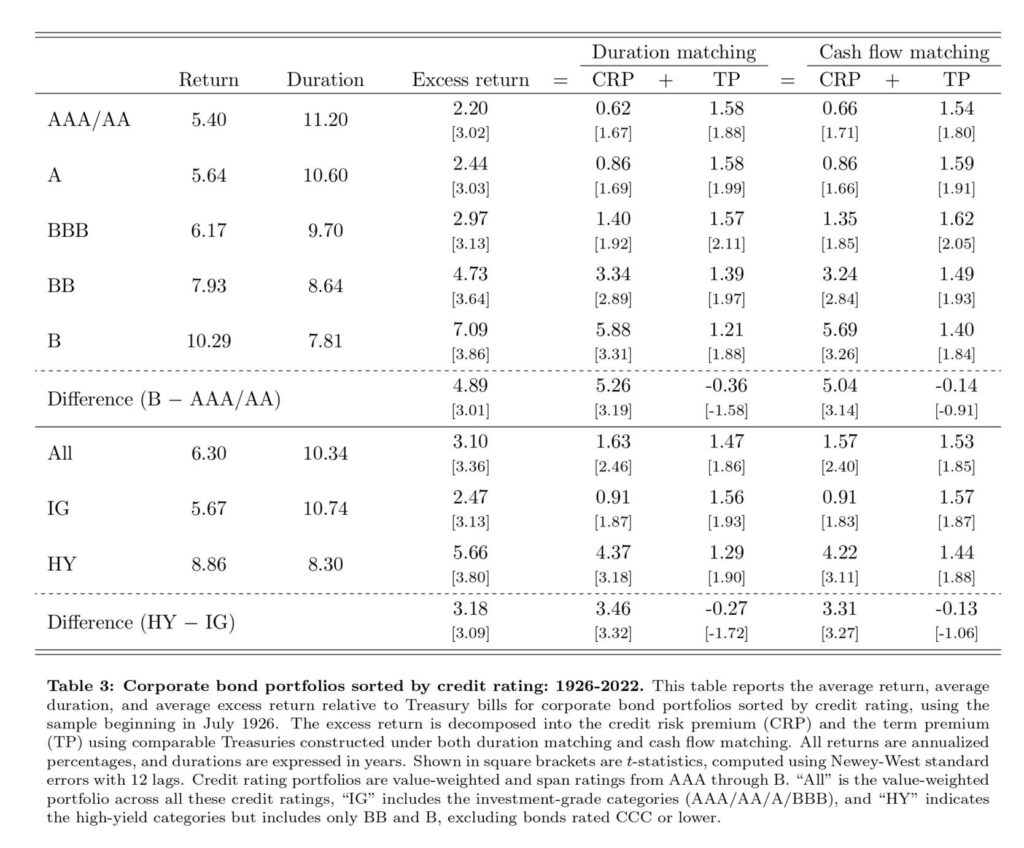

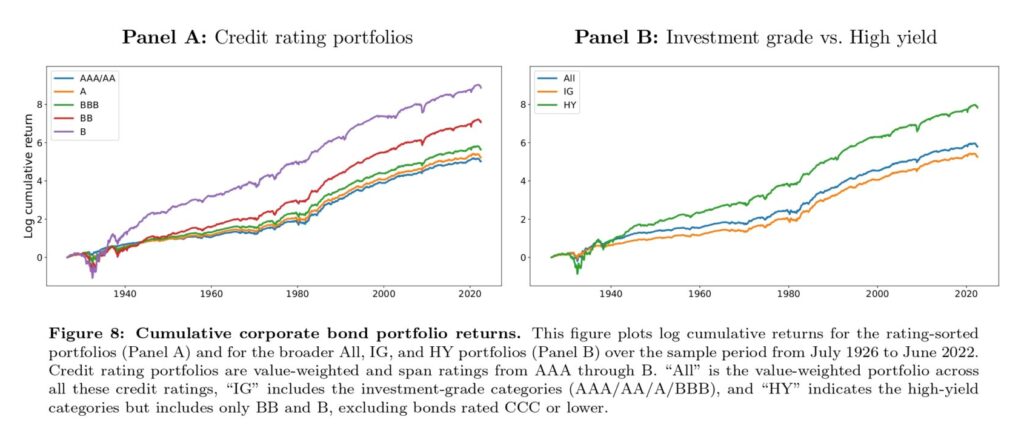

The paper’s central empirical contribution challenges recent literature suggesting that corporate bond excess returns are driven primarily by the term premium, similar to U.S. Treasuries. When the authors extend their analysis to the full 1895–2022 sample, they document a sizable and statistically significant credit risk premium that persists after controlling for duration and interest rate risk. Using Fama-MacBeth regressions, they show that the bond market factor (MKTB) is robustly priced in the cross-section of corporate bond returns, with additional explanatory power from bond-specific factors such as the downside risk factor (DRF) and credit risk factor (CRF) proposed by Bai, Bali, and Wen (2019). Critically, these results emerge only with the enhanced statistical power afforded by the century-long dataset; short-sample analyses fail to detect these effects, underscoring the perils of extrapolating from limited historical windows.

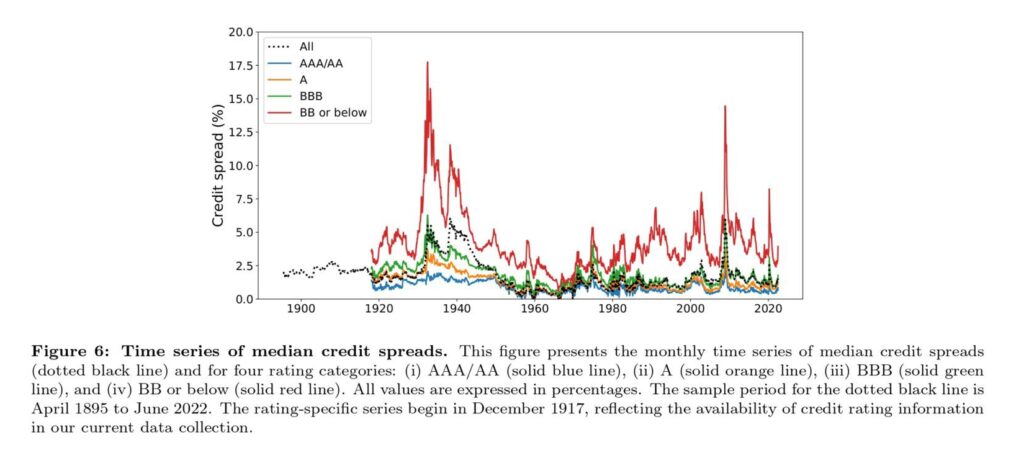

A second key finding concerns the predictive content of credit spreads. The authors confirm that aggregate credit spreads forecast future corporate bond returns and key macroeconomic aggregates, consistent with theories linking credit conditions to business cycle dynamics. However, they also document that the predictive power of spreads for real activity weakens when prewar data—including the extreme volatility of the Great Depression—are incorporated. This nuance suggests that while credit spreads remain valuable indicators of financial stress, their relationship with macroeconomic outcomes is time-varying and sensitive to structural breaks in the economy. The extended time series of the Gilchrist-Zakrajšek (GZ) spread, reconstructed back to 1926, further validates its role as a forward-looking measure of recession risk, albeit with varying efficacy across historical regimes.

Finally, the study bridges the equity and fixed-income literatures by demonstrating that prominent stock factors—including the Fama-French market, size (SMB), and value (HML) factors—are significantly priced in the cross-section of corporate bond returns when evaluated over the long sample. This finding supports the hypothesis of a common factor structure across asset classes and challenges narratives of market segmentation. Nontraded macro factors, such as intermediary capital shocks, macroeconomic uncertainty, and stock variance, also exhibit theoretically consistent risk premia, reinforcing the view that corporate bonds price economy-wide risks beyond idiosyncratic credit events.

Key takeaways for practitioners: First, the existence of a persistent credit risk premium supports strategic allocations to investment-grade and high-yield corporate bonds within diversified portfolios, particularly for long-horizon investors seeking return enhancement. Second, the time-varying predictive power of credit spreads implies that macro-aware tactical adjustments may improve timing decisions. Third, integrating this historical database with CRSP equity data opens new avenues for joint analysis of capital structure decisions and security returns. For researchers, this work establishes a new benchmark for empirical asset pricing in fixed income and cautions against overreliance on short-sample inferences. As the authors note, their database is designed to be a public resource—potentially catalyzing a new generation of studies on corporate bond pricing, credit cycles, and multi-asset risk management.

Authors: Mohammad Ghaderi, Sebastien Plante, Nikolai L. Roussanov, Sang Byung Seo

Title: Reconstructing a Century of U.S. Corporate Bonds: Credit Risk in Historical Perspective

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6444420

Abstract:

Do corporate bond investors earn compensation for bearing credit risk? We construct a new historical corporate bond database spanning 128 years, from 1895 to 2022, which allows us to estimate a corporate bond counterpart to the equity risk premium. Combining hand-collected monthly corporate bond quotes from three archival print sources with modern datasets, we assemble a panel comprising over 100,000 unique bonds and more than 7 million observations. While evidence from recent samples suggests that corporate bond excess returns are driven largely by the term premium similar to that earned by U.S. Treasuries, our longer historical sample reveals a sizable and statistically significant credit risk premium. Aggregate credit spreads predict future corporate bond returns and macroeconomic aggregates, although their predictive power for business cycle fluctuations weakens when prewar data, including the Great Depression, are added.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“Passive investing approaches have grown in popularity in recent decades relative to active investing. As the argument goes, it is difficult, if not impossible, to outperform the market, consistent with a large body of research that finds that the average mutual fund’s returns are equal to or lower than market returns (e.g., Fama and French, 2010). In addition, as its name suggests, passive investing is relatively easy and transparent, resulting in lower costs for a variety of reasons, including less trading and limited agency concerns. Thus, passive investors seek to match the market while minimizing costs. These investors often gravitate towards index funds, which exemplify passive investing by offering ownership in a large subset of the market with supposedly limited rebalancing and stock selection. As a result, index returns are usually close to the market return, and their fees are typically quite low, especially relative to other, more active mutual funds.

In summary, sampling has the potential to affect fund costs and returns through at least two channels. First, because the approach entails holding fewer positions, transaction costs could be lower, resulting in higher returns. Second, because the approach is based on factors other than index inclusion and size, it might entail more trading and effort that could either enhance or detract from cost and return performance. Ultimately, the relative strength of these two channels is an empirical question that we seek to answer in this study.

Several additional analyses support and extend our main results. First, our results hold in subsamples of S&P 500 indexers and other market-cap-based indexers, which helps rule out concerns that our findings are driven by one or a few peculiar indices, by “style” or “sector” funds, or by unobservable cross-index differences. Second, we find that our results are strongest among funds following indices with fewer constituent stocks, and that they entirely disappear for samplers following indices with 1,000 or more stocks. This suggests that sampling may not be detrimental to returns when it can drastically reduce the number of stocks held in the portfolio. Third, we find that investors’ funds increasingly flow to samplers relative to replicators over our sample period, which is puzzling given our cost and return results. While this might be explained by the formidable search frictions facing investors (Hortacsu and Syverson, 2004; Choi, Laibson, and Madrian, 2010), we leave it for future research to more fully resolve this puzzle.

Our study is among the first to compare the investment outcomes of replication vs. sampling index funds, which many still consider to be the closest thing to a purely passive investment. For example, Cheng, Massa, and Zhang (2019) document how conflicts of interest between sampling funds and their affiliated banks lead to deviations from the benchmark and higher returns; however, they do not compare the overall performance of replicators and samplers. We do, and the resulting findings are especially relevant to the vast literature examining the many types and aspects of active investing. These studies usually exclude index funds based on the assumption that they are passive (e.g., Pastor, Stambaugh, and Taylor, 2020); our evidence suggests this may not be an appropriate design choice in many cases.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend