Stock Price Overreaction to ESG Controversies

Nobody can doubt that in the recent period, ESG investing has significantly grown and is a staple part of the financial markets. The academic literature has also grown with the popularity of ESG investing. The negative, mixed and positive results for ESG scores in portfolios have evolved, and generally, there is a consent that ESG scoring can be a vital part of the portfolio management process. It can be observed that in the past, the ESG scores were not priced in the equity market and still, the ESG is not priced in the corporate bond market (apart from Europe). Nowadays, the investors react to the ESG scores, but the research paper of Cui and Docherty (2020) has novel insights that investors may react too much to the ESG. Their research shows that investors overreact to the negative ESG events and stocks connected with negative ESG events sharply fall, but the prices have mean-reverting properties. As a result, there is a reversal after bad ESG events. Stocks firstly sharply fall, but then their prices are reverted to the previous values. Therefore, this paper is interesting from the market pricing or efficiency point, but it also can be utilized by a reversal investor.

Authors: Bei Cui and Paul Docherty

Title: Stock Price Overreaction to ESG Controversies

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3559915

Abstract:

There has been substantial growth in the incorporation of environmental, social and governance (ESG) issues into investment decisions, and this trend has been motivated by the societal benefits that are achieved when socially responsible firms have access to cheaper capital. While the benefits with ESG investing are apparent, we investigate the possible downside of the trend towards ESG by examining how this approach to investing might affect market efficiency. ESG is now a highly salient aspect of an investor’s information set and, given cognitive limitations, investors might devote substantial resources to examining ESG characteristics to the detriment of other firm fundamentals. Consistent with salience theory, we report that this over-emphasis on ESG results in the market overreacting to news about ESG controversies. This over-reaction is more pronounced within smaller firms and stocks that were held by more transient investors before the announcement. Contrarian investors are likely able to profit from the unpopular strategy of buying stocks after bad ESG news is released.

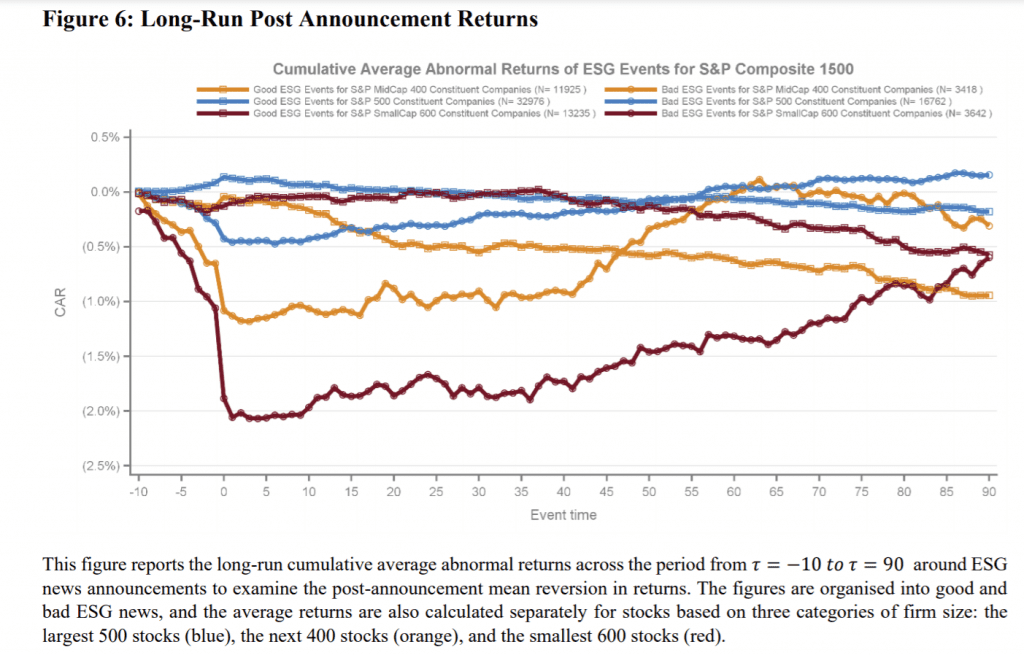

As always, the results can be presented through interesting chart:

Notable quotations from the academic research paper:

“While significant attention has been paid to the positive externalities created by the growth in ESG investing, a possible adverse outcome from this growth is that it may decrease market efficiency. ESG investors are argued to overweight information related to social performance relative to a firm’s financial fundamentals.

Our examination of the long-run announcements after ESG news announcements is motivated by recent literature that explores how institutional investors’ preferences for ESG may affect market efficiency. Hartzmark and Sussman (2019) report evidence of inflows (outflows) to funds that have good (poor) fund-level social responsibility ratings. This relationship is likely to encourage institutional investors to focus on the ESG characteristics of stocks and pay less attention to fundamentals (Cao et al., 2019). Furthermore, Starks, Venkat, and Zhu (2017) report that socially responsible funds are less inclined to sell stocks with high ESG ratings, even after negative news or fundamentals are reported. Consistent with the argument that preferences for ESG may affect market efficiency, Cao et al. (2019) report that stocks with higher ESG scores also tend to rank more highly on the Stambaugh, Yu, and Yuan (2015) mispricing measure and that the mispricing of socially responsible stocks is more prominent among stocks with higher ownership by ESG funds. This result is consistent with evidence that shows institutional investment constraints can affect stock prices (Cao, Han, and Wang, 2017).

Consistent with investors overreacting to ESG information, we report that negative ESG news releases are associated with a negative announcement return and a subsequent mean reversion. This overreaction is more pronounced across stocks with a high transient institutional investor ownership and high limits to arbitrage.

We argue that investors’ preferences for ESG should manifest in investors overreacting to news announcements relating to ESG. Our argument is grounded in salience theory. Taylor and Thompson (1982) define salience as “the phenomenon that when one’s attention is differentially directed to one

portion on the environment rather than to others, the information contained in that portion will receive disproportionate weighing in subsequent judgments.” The substantial increase in assets managed in a

socially responsible manner indicates that ESG issues are a salient aspect of the information set of a firm.

When news about an ESG controversy is released, investors overweight the probability that this event will be repeated in the future and therefore overreact to the news. Consistent with this overreaction, we report that there is a negative announcement effect when news about ESG controversies is released, but these returns mean-revert over the subsequent 90 days. The impact of both announcement returns and subsequent reversals are stronger for smaller capitalisation stocks and those stocks held by more transient investors before the news release.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend