Quantpedia in September 2024

Hello and welcome to our September recap!

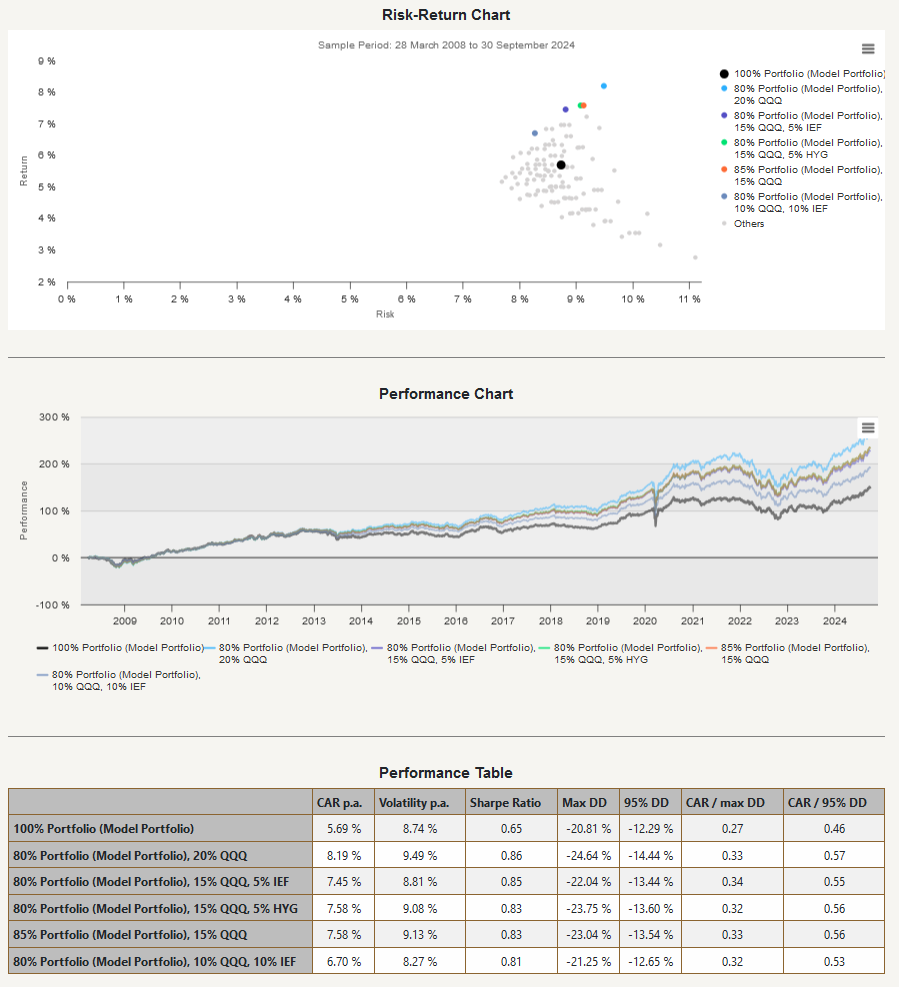

Let’s start with the recent Quantpedia Prime, Premium and Pro development – our new Optimization Report. As portfolio managers, we constantly seek ways to enhance the performance of our Model Portfolios, and we need a quick, efficient method to evaluate which assets from a Benchmark could improve the risk/return characteristics the most. That’s exactly why we built this tool. The new report allows users to simulate different portfolio adjustment scenarios by reducing the weight of the Model Portfolio and adding different combinations of assets from the Benchmark. This process generates multiple optimized portfolios, which are then visualized and ranked based on their return-to-risk ratio. The goal of this tool is to simplify portfolio management by helping users find the most effective asset allocations to maximize returns while minimizing risk.

Risk-Return Chart highlights the Model portfolio and the five portfolios with the best return/risk ratio. Afterward, the performance table includes standard metrics like return, volatility, max drawdown, Sharpe ratio, and car/max DD, listing the Model portfolio and the top five optimized portfolios along with their asset compositions and weights.

- 11 new Quantpedia Premium strategies have been added to our database

- 12 new related research papers have been included in existing Premium strategies during the last month

- 7 new backtests were written in QuantConnect code. Our database currently now contains over 800 strategies with out-of-sample backtests/codes.

Additionally, 5 new research articles were published on the Quantpedia blog in the previous month:

Valuing Stocks With Earnings

Authors: Sebastian Hillenbrand and Odhrain McCarthy

Title: Valuing Stocks With Earnings

ETF Re-balancing and Hedge Fund Front-Running Trades

Authors: Wang, George Jiaguo and Yao, Yaqiong and Yelekenova, Adina

Title: ETF Rebalancing, Hedge Fund Trades, and Capital Market

What Drives Crypto Asset Prices?

Authors: Austin Adams, Markus Ibert, and Gordon Liao

Title: What Drives Crypto Asset Prices?

How to Improve Commodity Momentum Using Intra-Market Correlation

Authors: Margareta Pauchlyova

Title: How to Improve Commodity Momentum Using Intra-Market Correlation

Revisiting Trend-following and Mean-reversion Strategies in Bitcoin

Authors: Sona Beluska

Title: Revisiting Trend-following and Mean-reversion Strategies in Bitcoin

Yours …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend