Quantpedia in February 2026

Hello all,

Welcome again to Quantpedia’s monthly recapitulation.

Firstly, let’s go through the Quantpedia Pro update.

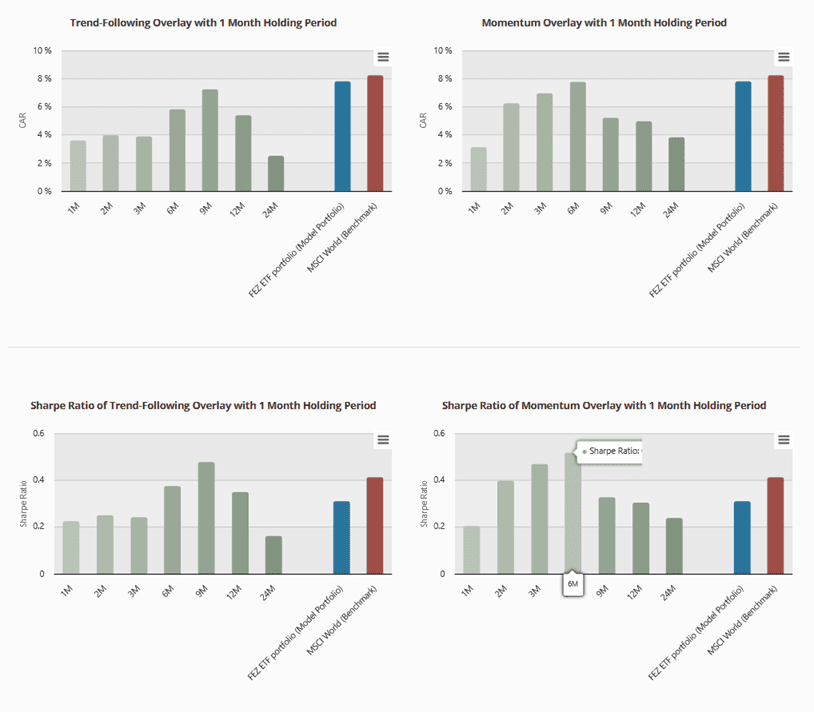

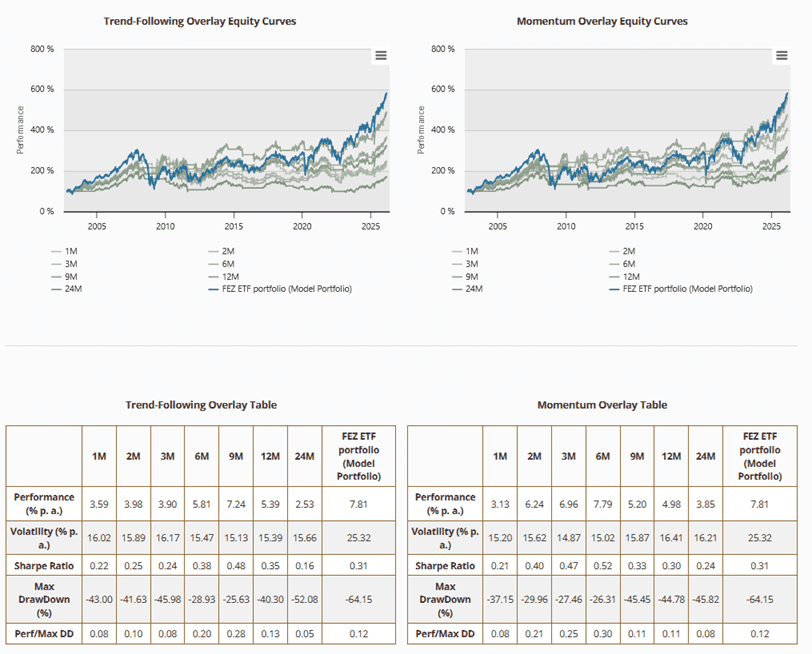

Over the past month, we revisited and significantly expanded the Trend/Reversal Analysis Report within Quantpedia’s portfolio analytics tools. The report is designed to help users evaluate how their custom model portfolio behaves under different momentum and trend-based overlays. In the first section, the tool applies positive trend and momentum overlays, where the portfolio is held long only during periods following positive trend or momentum signals. The results are directly compared with the original portfolio, allowing users to evaluate whether adding a trend-following filter improves risk-adjusted performance.

The report then expands the analysis across several additional scenarios. Users can test reversal rules, where the portfolio is short when the trend indicator signals a positive trend, as well as negative trend overlays, where the portfolio is held long only after negative momentum periods. Finally, the opposite overlay examines the case where the portfolio is short during negative trend regimes. With a broader set of rules and a significantly expanded set of charts, the redesigned report provides a more complete view of how a strategy performs across different trend and reversal environments, helping users assess whether such overlays can enhance the return-to-risk characteristics of their portfolios.

Secondly, we would like to invite you to watch the 8th episode of our YouTube video series QuantBeats. Crypto markets never sleep, but your trading system can do the work for you. Jiři Mrkva from Link.investments breaks down how he builds systematic crypto strategies, why automation beats emotional decision-making, and how robust quant systems can run in the background so investors spend less time watching charts and more time living their lives.

Listen to this newest Quantbeats episode, and we also sincerely invite you all to follow us on our YouTube, Linkedin, FB, Twitter, and/or Bluesky links.

Thirdly, we would like to invite you to the Future Alpha conference, which brings together a global community of quants, portfolio managers, risk leaders, and trading technologists focused on cross-asset investing. The event is designed around three dedicated tracks covering the full alpha lifecycle: AlphaX (alpha strategies, alternative data, and signal intelligence), RiskX (market risk, factor models, and portfolio construction), and TechX (infrastructure, execution systems, and trading architecture). The conference provides a platform for practitioners from leading funds, asset managers, and investment banks to share ideas, explore new signals, and discuss innovations shaping the future of quantitative investing.

If you are interested in attending, Quantpedia readers can use the code “Quantpedia20” during registration to receive a 20% discount on the conference pass.

Fourthly, we would like to remind all of you of our Quantpedia Awards 2026 competition. Time is ticking away, and the end of April is here very soon. Do not forget to join our race for a $25.000 prize pool, and if you can’t (or do not want to join), then please, share the message around you.

And finally, let’s also quickly recapitulate Quantpedia Premium development:

- 11 new Quantpedia Premium strategies have been added to our database.

- 5 new related research papers have been included in existing Premium strategies during the last month

- 7 new backtests were written in QuantConnect code. Our database currently contains, in total, over 930 strategies with out-of-sample backtests/codes.

Additionally, 5 new research articles were published on the Quantpedia blog in the previous month:

Combining Calendar Strategies into the Trading Portfolio

Author: David Mesicek

Title: Combining Calendar Strategies into the Trading Portfolio

Evaluating Reversal Potential in Niche Alternative ETFs

Author: David Belobrad

Title: Evaluating Reversal Potential in Niche Alternative ETFs

Systematic Allocation in International Equity Regimes

Author: Cyril Dujava

Title: Systematic Allocation in International Equity Regimes

2-Year Notes Momentum: Extracting Term Structure Anomalies from FOMC Cycles

Author: Cyril Dujava

Title: 2-Year Notes Momentum: Extracting Term Structure Anomalies from FOMC Cycles

Finding and Integrating Crisis Hedge Strategies: Improving Equity Portfolio Resilience

Author: David Mesicek

Title: Finding and Integrating Crisis Hedge Strategies: Improving Equity Portfolio Resilience

Yours …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend