Evaluating Reversal Potential in Niche Alternative ETFs

Alternative ETFs sit at an unusual intersection of public-market accessibility and hedge-fund-style investment techniques. They package managed futures, merger arbitrage, and option-based income strategies into exchange-traded products, yet they remain thinly traded and relatively niche compared to mainstream equity or bond ETFs. This combination makes them intriguing: they offer exposure to alternative risk premia, and their limited liquidity raises possibilities to build short-term reversal strategies.

When an ETF is liquid but its underlying assets are difficult to price in real time, temporary dislocations between market price and intrinsic value can arise, particularly during periods of elevated volatility. Sharp market sell-offs or rapid rallies may push the ETF price away from a reasonable estimate of its net asset value, not because fundamentals have changed, but because liquidity demand, hedging pressure, or order-flow imbalances dominate short-term pricing. These deviations create tactical opportunities for arbitrage-minded traders, who can buy temporarily oversold ETFs or short those that become overextended, expecting mean reversion once pricing efficiency is restored.

In the past, we analyzed the Overnight Reversal Effects in the High-Yield Market on the HYG ETF, which represents high-yield bonds of more heavily indebted firms. We examined their seasonal behavior throughout the week, while the fundamental value of the underlying assets remained largely unchanged. Not surprisingly, some anomalies appeared. Similarly, in the current context, the fundamental value of the assets remains more or less stable, and our focus is on observing and exploiting short-term reversal signals.

Data and assets

The landscape of alternative ETFs includes a range of niche strategies, each with its own approach and history. DBMF (iMGP DBi Managed Futures Strategy ETF), launched on May 8, 2019, seeks to replicate the performance of leading CTA hedge funds by trading diversified liquid futures across equities, fixed income, currencies, and commodities, aiming for returns with low correlation to traditional markets. Similarly, WTMF (WisdomTree Managed Futures Strategy Fund) employs a rules-based managed futures strategy that systematically trades futures on commodities, currencies, and interest rates to deliver returns independent of broad equity or bond movements; it was first listed on January 5, 2011. MNA (NYLI Merger Arbitrage ETF), launched on November 17, 2009, implements a merger arbitrage strategy by holding long positions in announced takeover targets, capturing the spread between current trading prices and expected deal prices. Finally, PBP (Invesco S&P 500 BuyWrite ETF), which began trading on December 20, 2007, follows a covered-call approach by holding the S&P 500 and writing call options on the index to generate premium income and reduce downside volatility.

Since our analysis will also include short positions, we are adding BIL (State Street SPDR Bloomberg 1-3 Month T-Bill ETF) to account for shorting costs. BIL tracks very short-term U.S. Treasury bills, providing a low-risk proxy for the financing cost of borrowing assets when implementing short strategies. Including it allows a more accurate evaluation of net returns in a trend-following or rotational framework.

Future analyses using DBMF show somewhat weaker results. However, due to our commitment to avoiding selection bias, we have decided to present all findings rather than selectively excluding outcomes that underperform. This approach ensures transparency and provides a complete picture of the strategy’s behavior across all alternative ETFs initialy selected.

Data were pulled from EODHD.com – the sponsor of our blog. EODHD offers seamless access to +30 years of historical prices and fundamental data for stocks, ETFs, forex, and cryptocurrencies across 60+ exchanges, available via API or no-code add-ons for Excel and Google Sheets. As a special offer, our blog readers can enjoy an exclusive 30% discount on premium EODHD plans.

Basic strategies

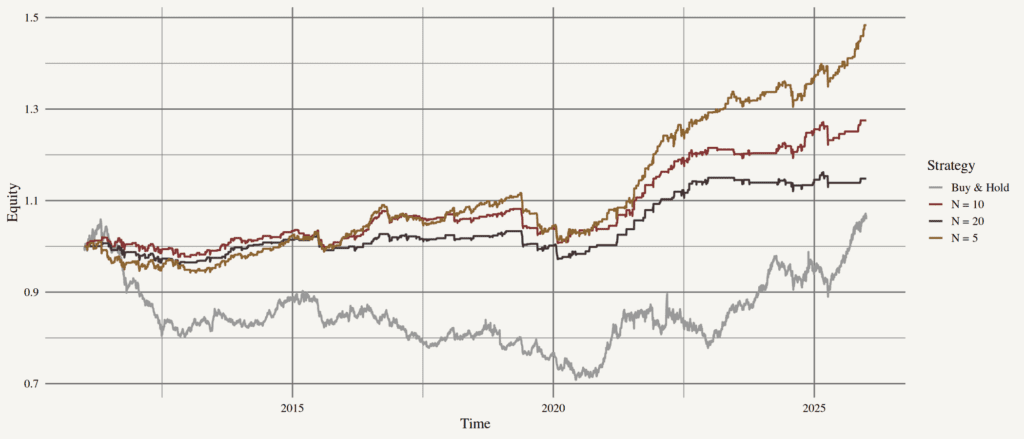

To begin, we examine a set of simple baseline strategies from which our later analysis will build. For each asset, we track its price development and open a short position (for one trading day, at market close) whenever it reaches an N-day high. As a reference strategy, we consider a simple buy-and-hold approach in which the asset is purchased at the start of the period and held throughout the entire period.

We observe that for relatively short-term values of N, the strategy behaves consistently and improves all performance metrics for every asset except DBMF. The resulting equity curves also appear noticeably smoother, which contributes to a higher Sharpe ratio.

This approach can also be applied on the long side, where we buy the asset (for one trading day, at market close) whenever it reaches its N-day low.

Once again, we observe a similarly positive effect of the strategy. This naturally raises the question of how to proceed, as trading only a single asset with limited liquidity is unlikely to be an ideal long-term solution.

Combining assets

A natural next step is to combine all assets into a single strategy. A straightforward approach would be to allocate a proportional share of the portfolio to each asset available at a given time (essentially constructing a naive portfolio) and then allocate that share to the asset whenever the maximum or minimum condition is met. However, this method often results in capital remaining unallocated because, on many days, just a few of the assets meet the required signal. For this reason, we instead adopt an alternative rule: the allocation remains equal across assets, but it is invested only in those that satisfy the corresponding condition on that particular day.

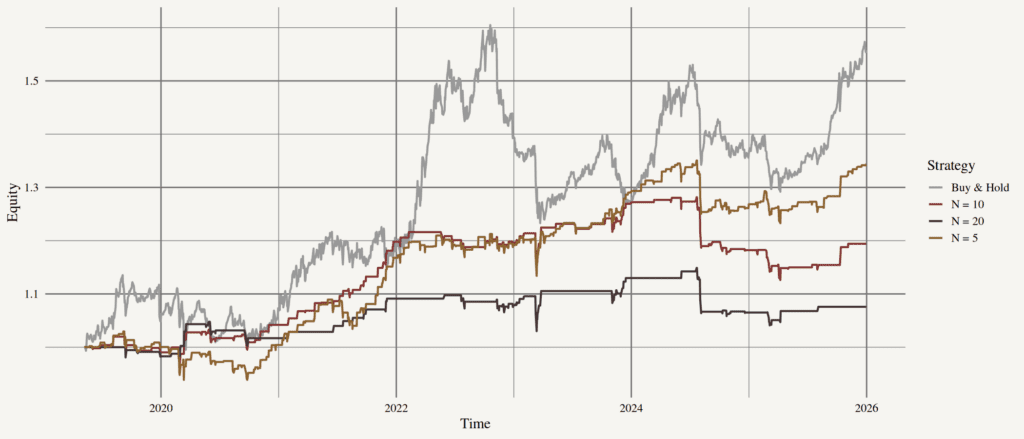

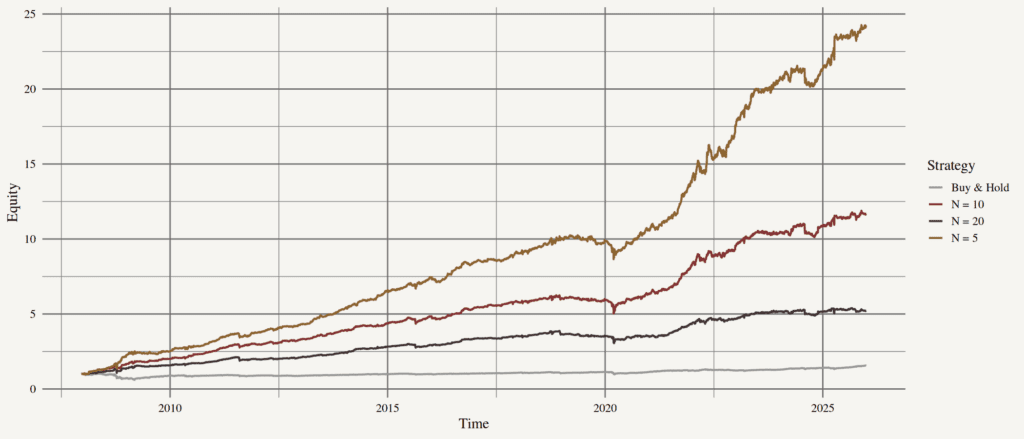

As a first step, we implement a strategy where we open short positions uniformly across all assets that meet the condition of being at their N-day maximum. The cost of holding short positions is covered by allocating to BIL, ensuring that the strategy accounts for the financing impact. For each day, we check which assets satisfy the short condition and allocate equal weights among them. If no assets meet the criterion, no capital is deployed.

Table 1: Performance metrics of short on high strategies for mix of assets.

| PORTFOLIO | CAR p.a. | VOL p.a. | MAX DD | SHARPE | CALMAR |

|---|---|---|---|---|---|

| N = 5 days short on high portfolio | 8.94% | 6.89% | -12.65% | 1.28 | 0.71 |

| N = 10 days short on high portfolio | 7.96% | 5.65% | -7.92% | 1.38 | 1.01 |

| N = 20 days short on high portfolio | 6.15% | 4.94% | -7.37% | 1.23 | 0.84 |

| Benchmark | 2.48% | 11.11% | -43.32% | 0.28 | 0.06 |

We observe that this choice significantly improves the portfolio’s performance. Selecting a smaller number of days for the extrema tends to enhance returns, as the strategy reacts faster to short-term peaks. However, when examining risk-adjusted metrics, it becomes evident that the higher returns come at the cost of increased risk exposure, implying a risk premium is being taken on.

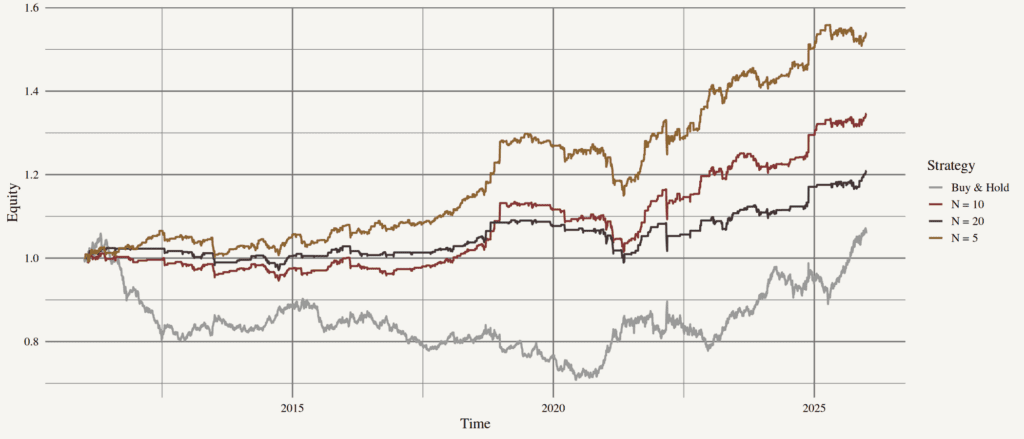

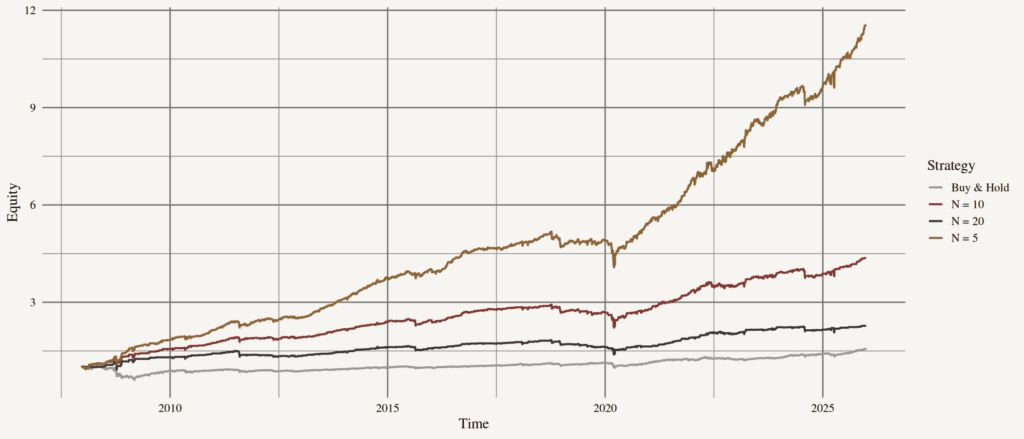

Similarly to previous cases, we can implement a long version of this strategy. In this variant, we open long positions in assets that are at their N-day minimum, allocating capital equally among all qualifying assets. This approach allows us to capture short-term upward reversals while maintaining the same framework for position sizing and risk management.

The cost of holding these positions is naturally lower, as long exposures do not incur financing costs, making the long strategy a complementary counterpart to the short-on-high implementation.

Table 2: Performance metrics of long on low strategies for mix of assets.

| PORTFOLIO | CAR p.a. | VOL p.a. | MAX DD | SHARPE | CALMAR |

|---|---|---|---|---|---|

| N = 5 days long on low portfolio | 14.55% | 9.22% | -21.31% | 1.52 | 0.68 |

| N = 10 days long on low portfolio | 8.53% | 8.85% | -24.21% | 0.97 | 0.35 |

| N = 20 days long on low portfolio | 4.67% | 8.32% | -24.15% | 0.59 | 0.19 |

| Benchmark | 2.48% | 11.11% | -43.32% | 0.28 | 0.06 |

In this case, choosing a shorter lookback window not only improves absolute returns but also enhances risk-adjusted metrics, such as Sharpe and Calmar ratios. This indicates that the strategy captures short-term upward reversals more efficiently, generating higher performance without proportionally increasing risk.

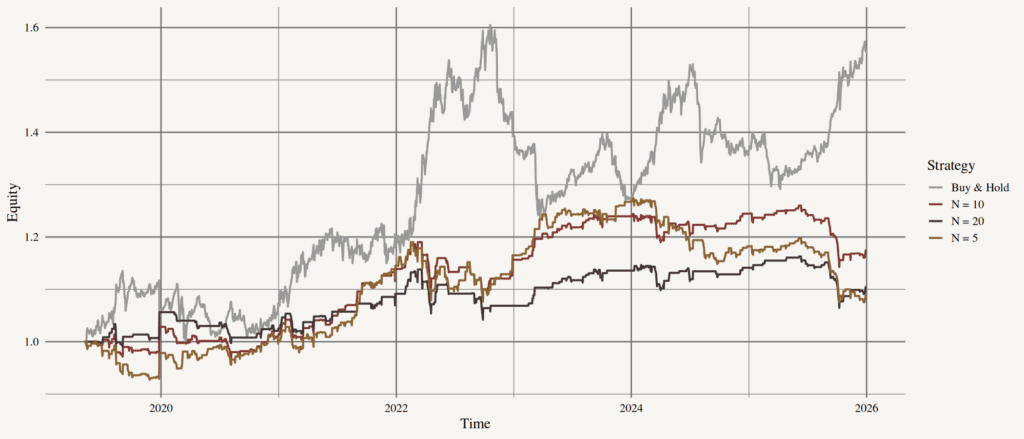

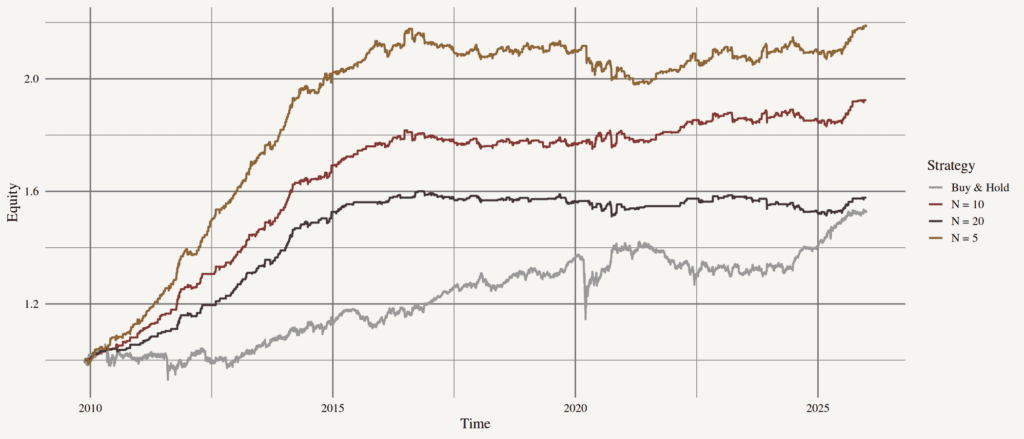

Mix of short & long

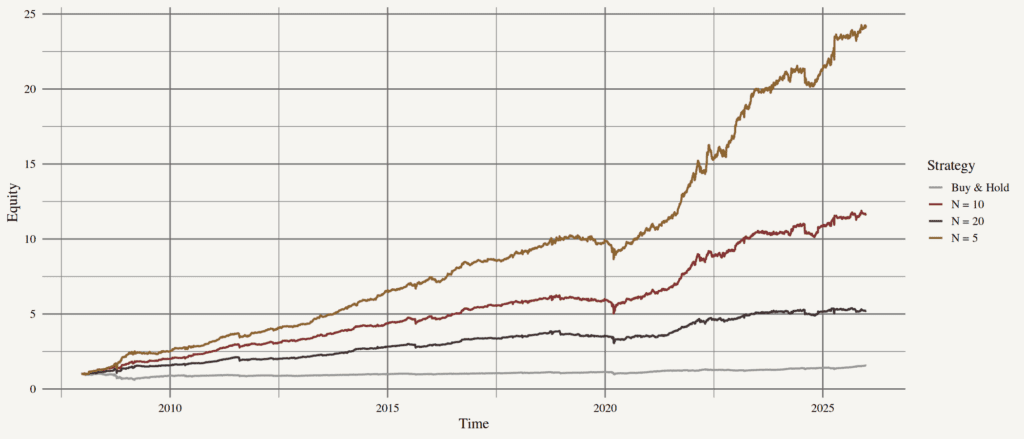

We now have two sets of relatively successful strategies. A natural next step is to implement them simultaneously. In this combined approach, we track which assets meet the N-day maximum (short) and N-day minimum (long) conditions at the same time. Capital is then allocated evenly among all active positions, ensuring that both long and short opportunities contribute proportionally to the portfolio. The short cost continues to be covered by BIL, maintaining realistic financing assumptions. This combined strategy allows us to capture short-term reversals in both directions while keeping risk balanced across all active positions.

Table 3: Performance metrics of combining long on low & short on high strategies.

| PORTFOLIO | CAR p.a. | VOL p.a. | MAX DD | SHARPE | CALMAR |

|---|---|---|---|---|---|

| N = 5 portfolio | 19.37% | 10.04% | -19.91% | 1.81 | 0.97 |

| N = 10 portfolio | 14.63% | 9.58% | -19.91% | 1.47 | 0.73 |

| N = 20 portfolio | 9.62% | 9.08% | -21.20% | 1.06 | 0.45 |

| Benchmark | 2.48% | 11.11% | -43.32% | 0.28 | 0.06 |

Again, we observe that combining the strategies benefits both absolute returns and risk-adjusted metrics. Since capital on the long side is not invested all the time, it can typically be deployed in the short side, allowing the portfolio to remain fully invested when opportunities arise and further enhancing overall efficiency.

Conclusion

In this article, we explored the possibility of trading actively managed small ETFs. We were able to identify several robust strategies that deliver double-digit annual returns while maintaining attractive risk-adjusted performance, demonstrating that even niche, low-liquidity assets can offer exploitable short-term reversal signals.

These strategies, however, come with a set of limitations. Our analyses were conducted using end-of-day data, which may significantly bias the results due to intraday volatility potentially triggering trading rules and creating noise. Another concern is the low liquidity of these assets. Regularly trading larger amounts could likely erode the very patterns we were able to observe, and both long and short sides of the trades could face execution challenges, whether in timing or pricing. Finally, since the strategy involves a high number of trades, a substantial portion of potential profits would likely be consumed by transaction costs, further reducing net performance.

Overall, we are dealing with assets that, while delivering respectable returns, come with limitations that must be acknowledged for the strategies we explored to work in backtests. These constraints, ranging from low liquidity and to intraday volatility and transaction costs, highlight that caution is required when attempting to implement these strategies in practice, despite their promising historical performance.

Author:

David Belobrad, Junior Quant Analyst, Quantpedia

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend