Quantpedia in April 2026

Hello and welcome to April’s recapitulation …

Firstly, let’s go through the Quantpedia Pro update.

In response to continued client interest, we have further expanded the capabilities of the Quantpedia API offering available to Quantpedia Pro subscribers. In addition to programmatic access to our database of systematic trading strategies, in/out-of-sample performance statistics, and source academic research papers, the API now also provides access to full historical equity curves for all backtested strategies together with the associated code snippets used in our research process. The addition of equity curve data significantly broadens the API’s applicability, enabling clients to utilize Quantpedia strategies not only as standalone research ideas but also as alternative datasets and investment factors for portfolio construction, machine learning applications, and AI model training workflows. Access to the API is granted individually to approved Quantpedia Pro subscribers upon request via our contact form.

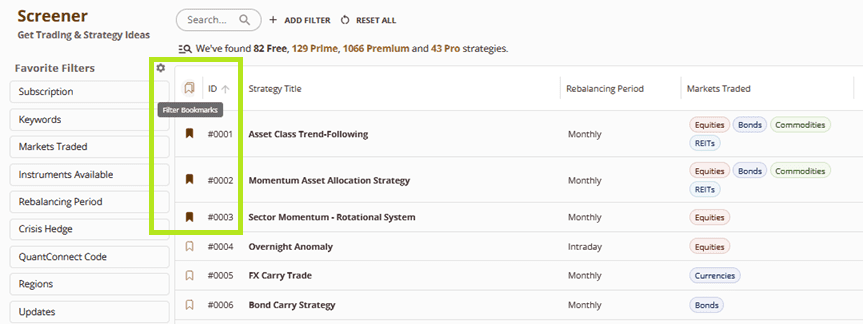

Additionally, we have expanded the functionality of the Quantpedia Screener with the introduction of Bookmarks, allowing users to easily mark and organize strategies they consider particularly interesting or relevant for further research. Bookmarked strategies can now also be incorporated directly into the Screener’s filtering framework, enabling users to create more efficient research workflows, quickly revisit selected ideas, and build customized subsets of strategies for portfolio construction, comparison, or ongoing monitoring.

Secondly, some of you, our readers, are probably interested in knowing the progress of the Quantpedia Awards 2026 competition. The deadline for paper submission is behind us, and Quantpedia’s team has processed papers. The final 10 have been sent to our committee for the next stage, ranking. Do you have any strong favourites? Who do you think will get a share of the $25.000 prize pool? Stay tuned, and we will announce results in the second half of May...

A/ Beckmeyer, Heiner and Berg, Florian and Wiedemann, Timo and Wortmann, Jonas: Reviving Anomalies

https://ssrn.com/abstract=6468806

B/ Colacito, Riccardo and Ding, Hui and Jiang, Fuwei and Qian, Yan: The POP Premium: Populism and the Cross-Section of Stock Returns

https://ssrn.com/abstract=5763042

C/ Gao, Cheng and Yuan, Peixuan: The Unpriced Risk in Momentum Strategies

https://ssrn.com/abstract=6112846

D/ Chen, Zefeng and Pu, Darcy: Autonomous Market Intelligence: Agentic AI Nowcasting Predicts Stock Returns

https://ssrn.com/abstract=6134446

E/ Liu, Huan and Liu, Miao and Liu, Zhizhe and Mei, Danqing: Can AI Do Financial Research? LLM-Guided Hypothesis Discovery in Asset Pricing

https://ssrn.com/abstract=6569258

F/ Nathan, Daniel and Suominen, Matti and Tasa, Joni: The Intramonth Momentum Cycle

https://ssrn.com/abstract=6426026

G/ Nguyen, T., Bui, D., Loi, N., Trinh, T., & Nguyen, N.: AQAA: An Always-On Autonomous Quant AI Agent for Continuous Alpha Discovery, Self-Optimization, and Live Trading

https://zenodo.org/records/19425661

H/ Suvak, Colin and Masturzo, Jim: A Tail of Five Skews

https://ssrn.com/abstract=5554621

I/ Wiedemann, Timo and Beckmeyer, Heiner: All Days Are Not Created Equal: Understanding Momentum by Learning to Weight Past Returns

https://ssrn.com/abstract=5702162

J/ Zarattini, Carlo and Aziz, Andrew and Mele, Antonio: The Volatility Edge, A Dual Approach For VIX ETNs Trading

https://ssrn.com/abstract=5316487

And finally, let’s also quickly recapitulate Quantpedia Premium development:

- 12 new Quantpedia Premium strategies have been added to our database.

- 7 new related research papers have been included in existing Premium strategies during the last month

- 8 new backtests were written in QuantConnect code. Our database currently contains, in total, over 940 strategies with out-of-sample backtests/codes.

Additionally, 8 new research reviews were published on the Quantpedia blog in the previous month:

Dual Momentum Allocation Between Physical Gold and Bitcoin (Digital Gold)

Author: Cyril Dujava

Title: Dual Momentum Allocation Between Physical Gold and Bitcoin (Digital Gold)

The Attention Factor: The Link That Connects Crypto and Public Equity Markets

Author: Harin de Silva

Title: The Attention Factor: The Speculative Risk You May Already Own

When Big Gets Small: Trading the Lower Tier of Large Caps and Upper Mid Caps

Author: David Belobrad

Title: When Big Gets Small: Trading the Lower Tier of Large Caps and Upper Mid Caps

The Tranching Dilemma

Authors: Carlo Zarattini and Alberto Pagani

Title: The Tranching Dilemma. A Cost-Aware Approach to Mitigate Rebalance Timing Luck in Factor Portfolios

Exploiting Mean-Reversion in Decentralized Prediction Markets: Evidence from Polymarket Binary Contracts

Author: Cyril Dujava

Title: Exploiting Mean-Reversion in Decentralized Prediction Markets: Evidence from Polymarket Binary Contracts

Trading as a Small Business: What Beginner Investors and Traders Usually Learn Too Late

Author: David Mesicek

Title: Trading as a Small Business: What Beginner Investors and Traders Usually Learn Too Late

How to Analyze Individual Equity Curves

Authors: David Mesicek

Title: How to Analyze Individual Equity Curves

Commodity Portfolio Strategy for a Potential 2026 Inflationary and Supply Shock Regime

Author: David Mesicek

Title: Commodity Portfolio Strategy for a Potential 2026 Inflationary and Supply Shock Regime

Yours …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend