Analysis of Systematic Crypto Trading Strategies in 2021

We started to systematically search for systematic cryptocurrency trading strategies in academic research approximately two years ago. They currently form around 3% of our database of algorithmic and quantitative trading strategies. They are not so populous as other hot topics like “machine learning” (5% of our database) or “alternative data” (13%), but their ranks are definitely growing. Of course, the highest number of strategies are still related to main asset classes like equities, bonds, commodities or currencies, as strategies related to “smart beta” or “factor investing” keywords constitute over 50% of our database.

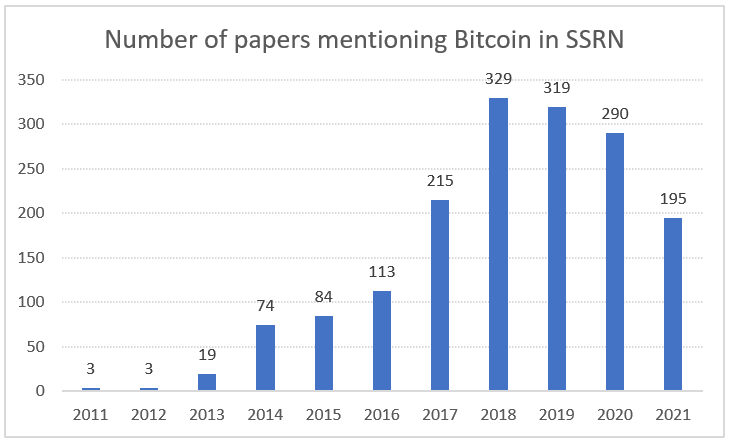

Older academic research related to cryptocurrencies (around the years 2011-2016) investigated mainly macro-economic and monetary attributes of this new phenomenon. Researchers tried to find answers to whether cryptocurrencies are a new asset class or can be part of the existing structure of the financial system, how they differ from other asset classes and if they contribute to money laundering. We can analyze the popularity of cryptocurrencies by looking at the number of research papers related to the word “Bitcoin” in the SSRN database. There exist only three papers from the year 2011 and three from the year 2012. The academic community’s interest started to grow in 2013 (with 19 papers) and 2014 (74 papers), peaked during 2018 and is currently around 300 papers a year. The year 2021 is unfinished; based on the current trend, there will probably be over 300 papers published in 2021. Other keywords (for example, “cryptocurrency”) show a similar pattern.

The debate about whether cryptocurrencies are an individual asset class has been largely closed (we can consider cryptocurrencies to be a distinct asset class with hybrid features of small-cap stocks, commodities and currencies). We have also written a few articles related to Bitcoin behaviour (Bitcoin in a Time of Financial Crisis or our crypto market phases case study). The debate about the role of cryptocurrencies in our society is still ongoing, and it will probably not end soon. But that’s not our interest at the moment.

Academic research started to be focused more on cryptocurrency trading strategies during Bitcoin (and other cryptos) price surge in 2017. Since then, research papers related to crypto trading have started to pop up, but they are still not a majority of published papers. It seems that researchers are still focused more on economic theory than trading practice. But we are thankful for those researchers who have an interest also in systematic trading.

Research papers related to systematic cryptocurrency trading strategies can be divided into 2 parts – price-based strategies, which are often momentum-based or trend-following strategies, very well-known from the other asset classes. The second group of strategies uses non-price signals like cryptocurrency network characteristics (number of active addresses, hash-rate, etc.) or interest rates. As the recent Bloomberg article mentioned, very often, trading strategies that are well-known in other asset classes (stocks) and are no longer so profitable can be rejuvenated as crypto strategies. We are also big fans of using strategies discovered in one asset class in another setting.

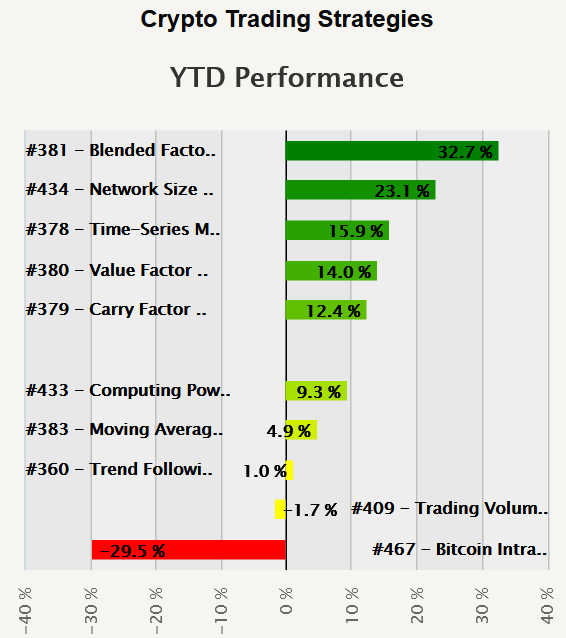

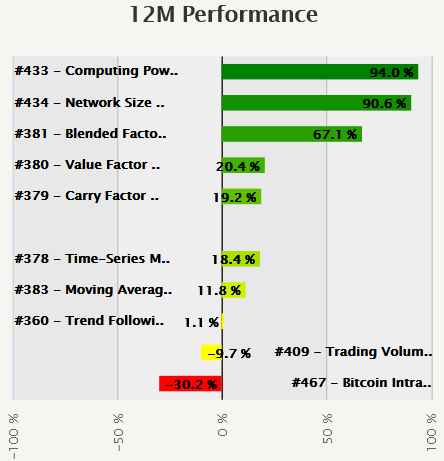

And how does a performance of crypto trading strategies look like? We can use the “Strategy Segment” report from Quantpedia Pro service, which shows the best 5 (and worst 5) strategies over the 1M, 12M and year-to-date periods. We would like to mention that all crypto strategies in the Quantpedia database are scaled to 1/10 of the total portfolio value. We need to do that step to ensure that the volatility of cryptocurrency trading strategies approximately matches the volatility of trading strategies used in other assets (equities, commodities, etc.).

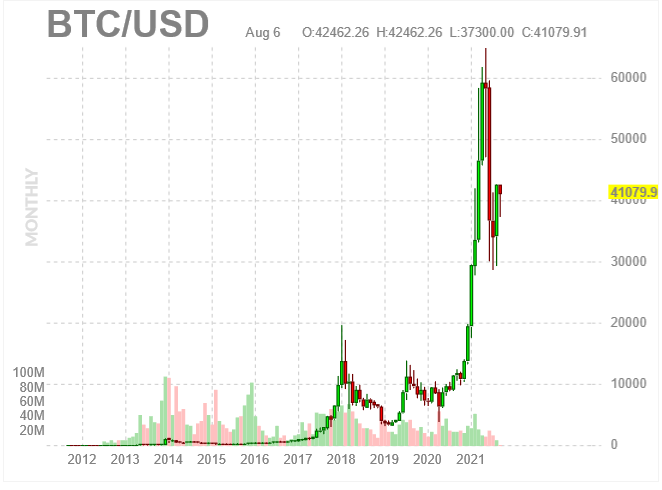

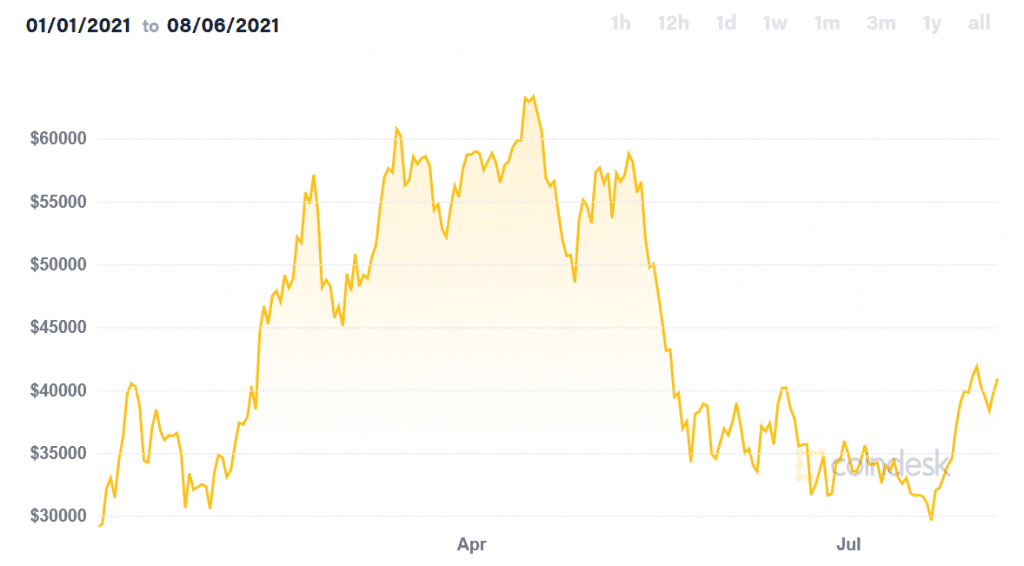

The best performing strategy is a blend of multiple individual factor strategies, and non-price strategies occupy the front 3 out of 5 best YTD strategies. It looks that price action in the cryptocurrency market in 2021 was not suitable for trending strategies (fast surges in price and similarly fast declines; see, for example, BTC price action in the next picture), and non-price signals had higher predictivity.

Interestingly, the 1-year performance of systematic cryptocurrency trading strategies also shows the dominance of non-price signals. Thus, it seems that cryptocurrencies are not so different from other assets. It also pays off to utilize information hidden in blockchains, interest rates, the trading volume of crypto-exchanges, and other predictors to build a more robust multi-factor portfolio of strategies.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend