How to Use ETF Flows to Predict Subsequent Daily ETF Performance

Exchange-traded funds (ETFs) are incredibly versatile investment vehicles. They have become more popular in recent years as investors have grown more comfortable with passive investing strategies. But ETFs can be very useful also in active trading strategies, as they can be used to gain exposure to specific markets, sectors, or themes.

ETFs trade on stock exchanges like regular stocks, which means they can be bought and sold throughout the trading day at market prices. This makes them easy to buy and sell for investors and allows them to be used in a variety of different investment strategies. Another reason for their popularity is their low cost. ETFs typically have lower expense ratios than actively managed mutual funds, which means they can be a more cost-effective option for investors. Last but not least, ETFs offer a high degree of diversification.

Overall, the combination of accessibility, low cost, diversification, and the ability to target specific areas of the market has made ETFs an attractive option for investors and traders. But when you invest in ETFs or trade them regularly; it’s really good to look under the hood and learn some tricks where to obtain a new source of alpha. And one such possible source or information advantage may be the possibility of analyzing the ETF flows data …

Where can we find inspiration? Let’s again turn our eyes to academic research…

Liao Xu, Xiangkang Yin and Jing Zhao (2018, revised 2021) identify an interesting speculating strategy that is likely to be adopted by APs (Authorized Participants) and their clients – acquire or retire ETF shares in the primary markets using unexpected ETF flows. The investment period starts in January 2012 and ends in December 2016. Authors decompose an ETF’s daily flow by regressing it against the market demand for the ETF on that day and the anticipated arbitrage opportunities on the next day. This decomposition process estimates a flow component due to demand in the secondary market of the ETF and another corresponding to arbitraging across the ETF and the basket of the ETF’s underlying securities. The residuals of this regression are unexpected ETF flows.

And here comes the strategy – the unexpected ETF flow is significantly and positively related to the ETF return on the following day. We can construct a value-weighted portfolio with simple rules: At the open of day t, we categorize all ETFs in our sample into two groups based on the Flow variable from day t-1, and then go long ETFs with positive Flow, and short ones with negative. The whole procedure is to be found in section 2.2 ETF Flow Decomposition. The weight of the single individual ETF in question is the ratio of ETF size to the total size of all ETFs in the sample on day t-1, where the size of an ETF is proxied by the value of assets under its management.

Authors state that return predictability by unexpected ETF flows is conditional, depending on the spread between the ETF’s price and its Net Asset Value (NAV). On days when an ETF is traded at a premium (discount), ETF share creation (redemption) can powerfully predict the next day’s positive (negative) returns. However, the creation (redemption) does not credibly predict returns on days when the ETF is traded at a discount (premium).

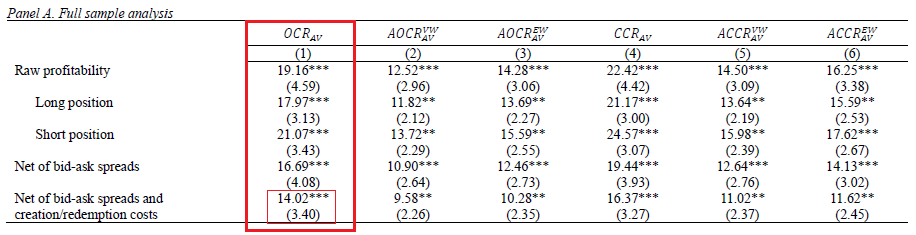

And what’s the performance? Let’s take a look on table 7:

An excerpt from Table 7. Profitability of investment portfolios based on unexpected ETF creation and redemption: Value weighting

The resultant strategy has a yearly performance of 14.02% (net of bid/ask spread and creation/redemption costs) with a t-statistic of 3.40, which we can translate into approximate 16% yearly volatility, which gives us a Sharpe ratio of 0.88.

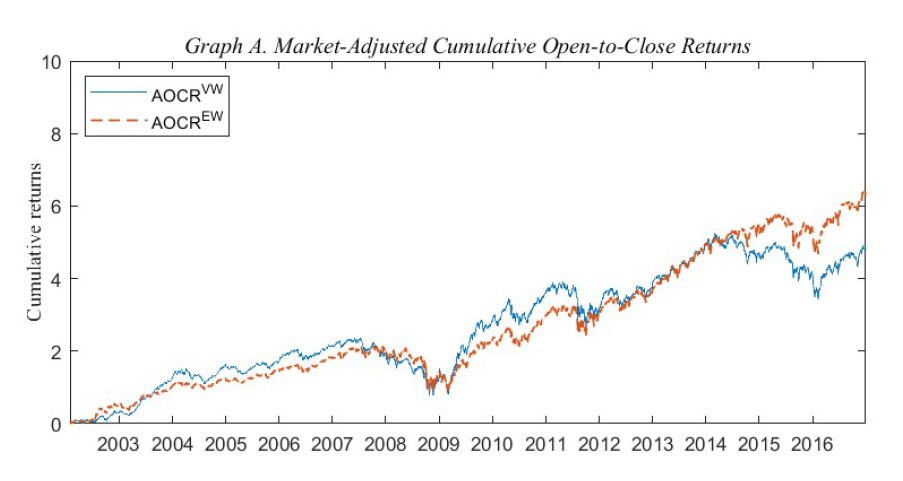

Following Figure 1 from the paper depicts the market-adjusted cumulative profitability of investment portfolios based on unexpected ETF creation and redemption:

The paper studies how Authorized Participants may execute this strategy, and they may have the advantage of using the creation and redemption of ETFs to decrease their trading costs. Most of the market participants do not regularly access ETF primary market, but the strategy can be executed also on the regular exchange, and the paper’s main added value is the idea of using the information about the ETF flows to reap substantial abnormal profits.

Evidently, having the information advantage about ETF creations and redemptions is profitable. But we can refrain from directly copying the proposed very active strategy, and still realize some of the benefits. Sometimes, it’s even enough to incorporate the information about the ETF flows into the portfolio’s rebalancing process and selectively consider postponing or accelerating the sale or accumulation of particular ETFs with algo trading to make a lesser impact on the market.

|

Interested? |

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend