Quantpedia in February 2024

Hello all,

In the domain of portfolio management, the annuity simulation is an indispensable instrument within the investor’s and trader’s toolkit. All of us will sooner or later retire (some already retired), and it is very valuable to have a model that helps to gauge how long will a stash of money endure if it’s invested in a diversified portfolio of ETFs, funds or trading strategies. And that’s what we have prepared for our Quantpedia Pro clients as our next report.

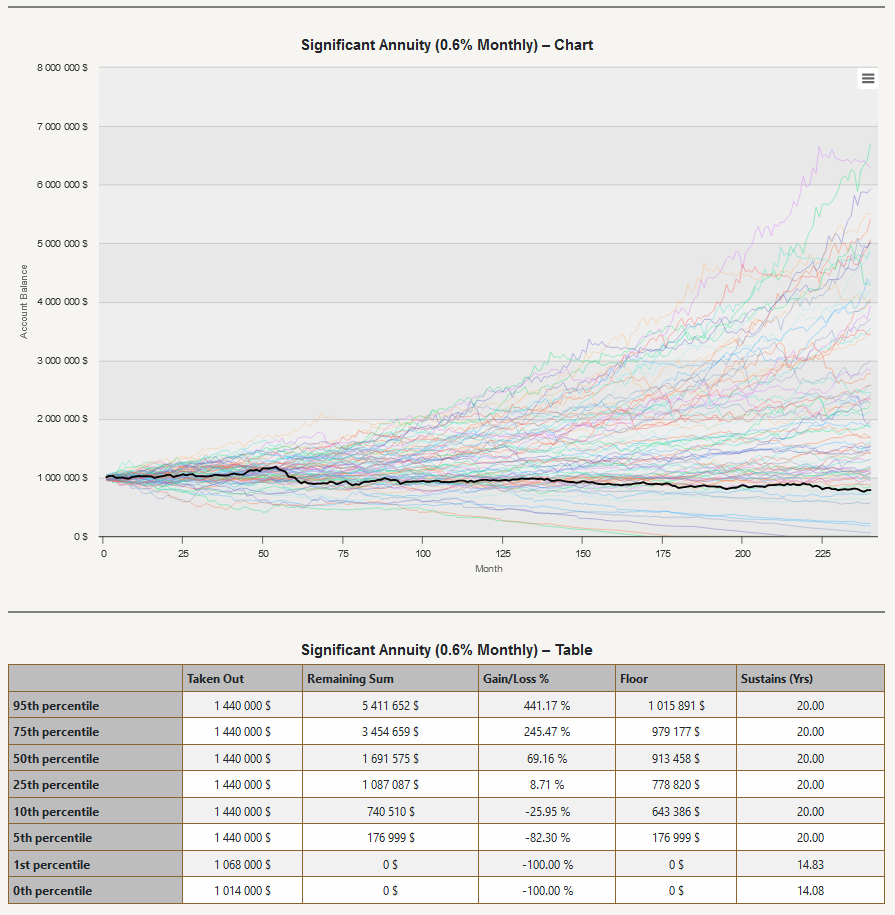

The Annuity Simulation Report investigates spending patterns for your Model Portfolio (built from any combination of our strategies, ETFs, or your uploaded equity curves) over the period of 20 years, with 5 different levels of outlays:

– from the most conservative (0.2% of the model portfolio is withdrawn on a monthly basis, 2.4% on a yearly basis)

– through the balanced annuity (0.4% monthly withdrawal rate, 4.8% on a yearly basis)

– the significant annuity (0.6% monthly withdrawal rate, 7.2% on a yearly basis)

– the aggressive annuity (0.8% monthly withdrawal rate, 9.6% on a yearly basis)

– and the very aggressive annuity (1.0% monthly withdrawal rate, 12.0% on a yearly basis)

As usual, at the beginning of the analysis, we use our state-of-the-art multifactor model to create a 100-year history of synthetic portfolio based on your Model Portfolio to extend the limited historical time window that’s usually available for most of the ETFs and trading strategies. Afterward, we sample the synthetic equity curve and create approximately one hundred 20-year (240-month) historical time periods that are firstly used to study how the one-time investment of $1.000.000 into the underlying model portfolio at the beginning of each period in combination with the monthly annuity would evolve over time. The results can be reviewed in the table and visualized form at the top of the report, whereby the most recent 20-year time period is highlighted.

Users can study the whole distribution of the results, be it the total sum that can be taken out as annuity, final portfolio value at the end of the 20-year period, total % gain, floor (the minimal sum that was in a portfolio over the 20-year period), and how long the portfolio would sustain selected withdrawal rate.

Secondly, we would like to remind all of you of our Quantpedia Awards 2024 competition. Time is ticking away, and the end of April is here very soon. Do not forget to join our race for a $15.000 prize pool 🙂

And as usual, let’s also quickly recapitulate Quantpedia Premium development:

- 10 new Quantpedia Premium strategies have been added to our database

- 11 new related research papers have been included in existing Premium strategies during the last month

- 8 new backtests were written in QuantConnect code. Our database currently now contains nearly 750 strategies with out-of-sample backtests/codes.

Additionally, 6 new research articles were published on the Quantpedia blog in the previous month:

How to Better Estimate Long-Term Expected Returns

Authors: Rui Ma, Ben R. Marshall, Nhut H. Nguyen, Nuttawat Visaltanachoti

Title: Estimating Long-Term Expected Returns

How Much Bitcoin Should We Allocate To the Portfolio?

Authors: Juliana Javorska, Radovan Vojtko

Title: How Much Bitcoin Should We Allocate To the Portfolio?

Robustness Testing of Country and Asset ETF Momentum Strategies

Author: Jiang Du

Title: Robustness Testing of Country and Asset ETF Momentum Strategies

Gauging Existing Technical Fundamental Features through Mutual Information

Authors: Gabriel Kingsley-Nyinah, Sergei Egorov

Title: Gauging Existing Technical Fundamental Features through Mutual Information

The Distribution of Stock Market Concentration in the U.S. Over the History

Authors: Logan P. Emery and Joren Koëter

Title: The Size Premium in a Granular Economy

Yours …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend