Hello all,

January was a really productive month for us. A lot of things clicked as they should, and we have a lot of announcements for you – starting with a new Quantpedia Pro report, continuing with the possibility of gaining an exclusive 10% discount on our services, an invitation to a webinar, a reminder of our Quantpedia Awards 2024 competition, and finally, a usual bunch of new articles and backtests.

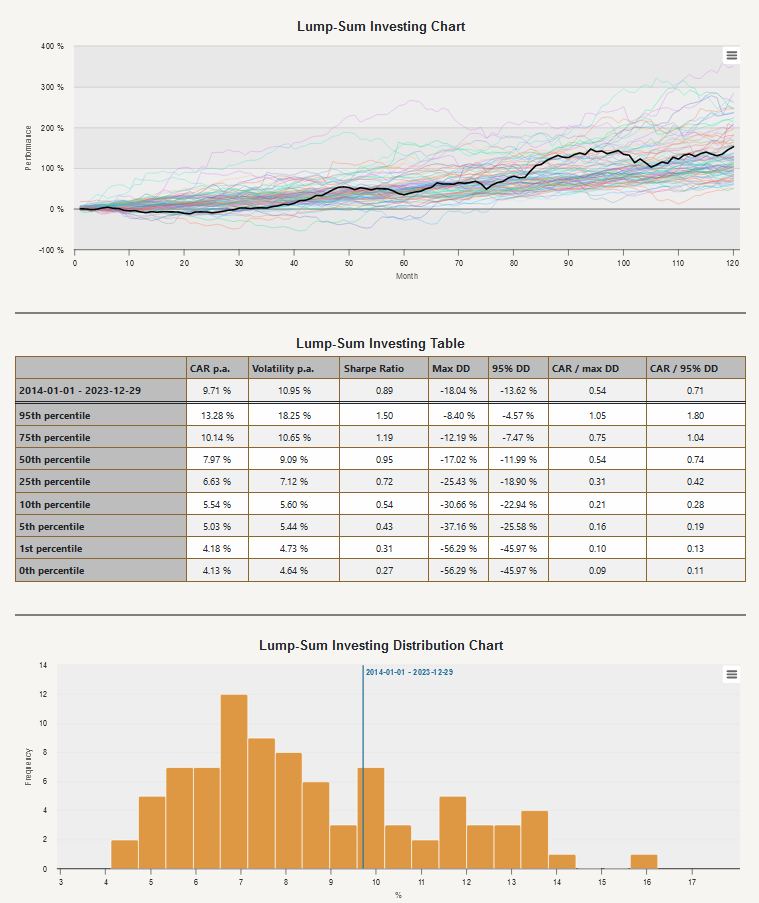

So, firstly, let’s start with a new Savings Plan Analysis report. The main goal of this report is to help all users assess how the Model Portfolio (selected in the Portfolio Manager) would work as an underlying for periodic savings. As usual, at the beginning of the analysis, we use our multifactor model to create a 100-year history of synthetic portfolio based on your Model Portfolio to extend the limited historical time window that’s usually available for most of the ETFs and trading strategies. Afterward, we sample the synthetic equity curve and create approximately one hundred 10-year (120-months) historical time periods that are firstly used to study how the one-time investment into the underlying model portfolio would evolve over time. The results can be reviewed in the table and visualized form at the top of the report, whereby the most recent 10-year time period is highlighted.

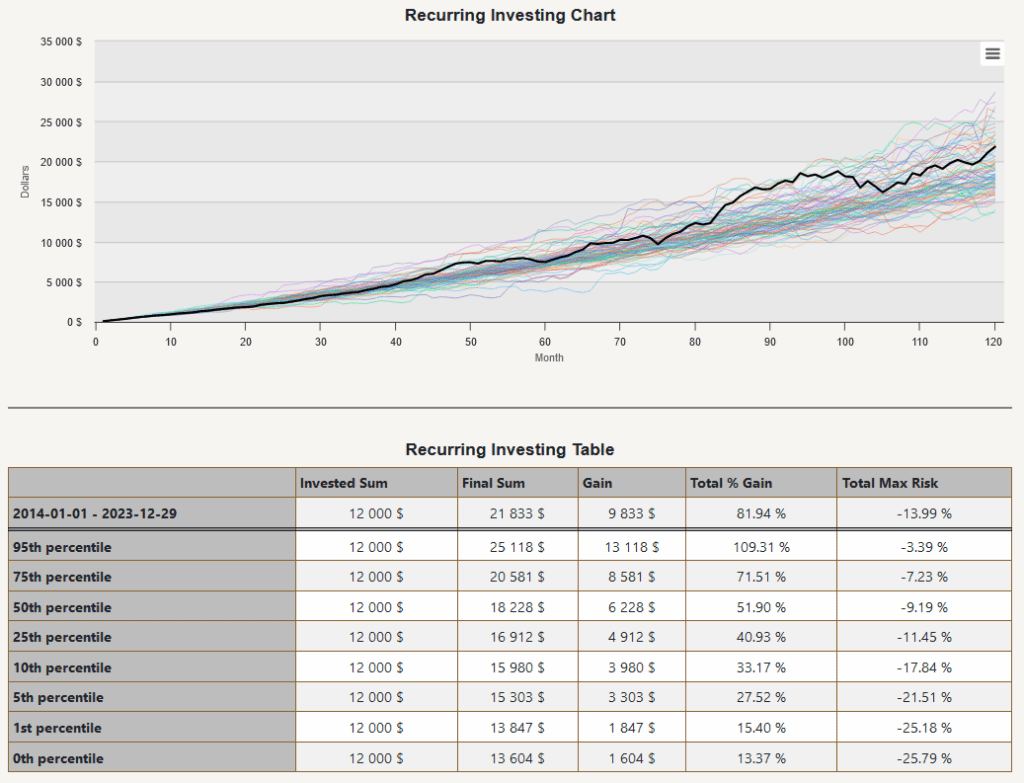

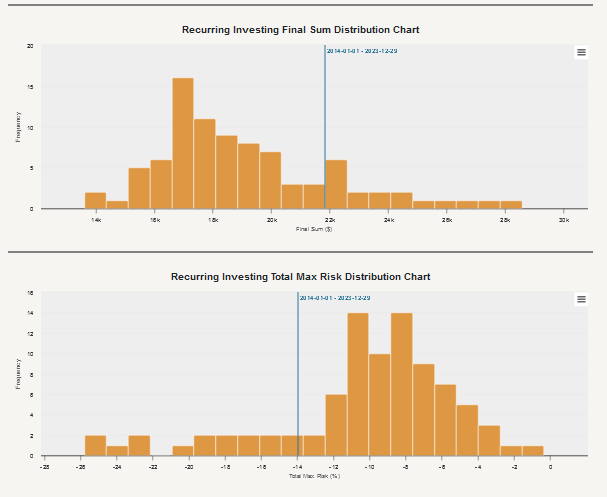

In the next part of the report, we proceed to simulate how the recurring investment of $100 a month (total invested sum of $12.000) would fare over all of the 10-year time periods. Users can study the whole distribution of the results, be it the final portfolio value, total $ gain, total % gain, or maximal risk over the 10-year periods.

This new tool offers you a unique and invaluable perspective on your investment choices. It empowers you to make informed decisions about your savings strategy, ensuring you can confidently choose the most suitable portfolio for your financial goals and maximize your long-term returns.

Secondly, we would like to ask you for assistance 🙂 We work very hard to improve our services, and every month, we bring you new insights from the field of algo/quant research. We want to become even better, and for that, we would like to ask you to help us and fill out the short Quantpedia’s survey that contains questions that will help us to better plan our work for a longer period of time on a strategic level. Of course, we also value your time, so we would like to offer you a 10% discount coupon that will get every one of you who will fill out the survey. This coupon code is valid for the next 12 days (until the 21st of February) and applies to all Quantpedia Prime/Premium/Pro subscriptions.

Thirdly, we would like to sincerely invite you to the upcomming online webinar/webinar where the Quantpedia will be one of the speakers. The title of the webinar would be the ETFs Uncovered: Strategies, Data, and Innovations and you can gain insights into the world of Exchange-Traded Funds (ETFs). Webinar’s panel guests (Wes Gray from Alpha Architect, Jack Kimmel from the ETF Global, Dan Hubscher from Changing Market Strategies, and me – Radovan Vojtko, Quantpedia) will discuss the integral role of ETFs in modern portfolios, covering the strategic and tactical applications, differentiation strategies for new ETF products, and the intriguing topic of Crypto ETFs. Don’t miss this opportunity and join us on Wednesday Feb 28, 2024, 10am ET (New York) Time.

Fourthly, we would like to remind all of you of our Quantpedia Awards 2024 competition. There is still a lot of time until the end of the submission deadline, but time flies very fast, and the end of April is here very soon. So do not forget to join our race for a $15.000 prize pool 🙂

At last, let’s also quickly recapitulate Quantpedia Premium development:

- 11 new Quantpedia Premium strategies have been added to our database

- 12 new related research papers have been included in existing Premium strategies during the last month

- 8 new backtests were written in QuantConnect code. Our database currently now contains nearly 740 strategies with out-of-sample backtests/codes.

Additionally, 6 new research articles were published on the Quantpedia blog in the previous month:

How to Build a Systematic Innovation Factor in Stocks

Authors: Margareta Pauchlyova, Radovan Vojtko

Title: How to Build a Systematic Innovation Factor in Stocks

Improving FX Carry Strategy with Exotic Currencies and the Frontier Markets

Author: Ákos Török

Title: Exotic Currencies and the Frontier Premium in Foreign Exchange Markets

Are Cryptocurrencies Exposed to Traditional Factor Risks?

Authors: Guilda Akbari, Adelphe Ekponon, and Zihan Guo

Title: Are Cryptocurrencies Exposed to Factor Risk?

Exploration of CTA Momentum Strategies Using ETFs

Authors: Margareta Pauchlyova, Radovan Vojtko

Title: Exploration of CTA Momentum Strategies Using ETFs

Machine Learning Execution Time in Asset Pricing

Authors: Umit Demirbaga and Yue Xu

Title: Machine Learning Execution Time in Asset Pricing

Pragmatic Asset Allocation Model for Semi-Active Investors

Authors: Radovan Vojtko, Juliana Javorska

Title: Pragmatic Asset Allocation Model for Semi-Active Investors

Yours …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Visit our Blog or Screener.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want to know more about us? Check how Quantpedia works and our mission.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Do you have an idea for systematic/quantitative trading or investment strategy? Then join Quantpedia Awards 2024!

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend