YTD Performance of Equity Factors – Update After Two Months

Nearly two months ago, in a time of the highest turmoil during the current pandemic crisis, we performed a quick assessment of the status of performance of equity factor strategies. The world has still not been able to ward-off health-care crisis completely, but a lot of countries have made significant progress (on the other hand, there are still a lot of countries in a worse state than a few months ago). Equity indexes have rebounded from the March lows and have removed some of the losses. Therefore, we have received multiple inquiries about the current situation of equity factor strategies.

The economic situation in most countries looks bad with rising unemployment and stopped public life.

However, central banks and governments reacted fast, and it seems, that stocks were able to throw away worries about the economy and are floating on an enormous pillow of underlying fiscal and monetary stimulus. So it may be a good time to revisit once again how factor strategies perform.

Analysis setup

We want to make this comparison the most accurate. Therefore, the We want to make this comparison the most accurate. Therefore, the selected sample again consists of 7 well-known equity factor strategies – size, value, momentum, quality, investment, short-term reversal and low volatility factors. All strategies are again backtested in QuantConnect framework, and investment universe in all 7 cases consists of 1000 US stocks with the highest liquidity (defined as stocks with the highest average monthly dollar turnover). We will not publish trading rules for all strategies again; readers can revisit our previous article if they are interested.

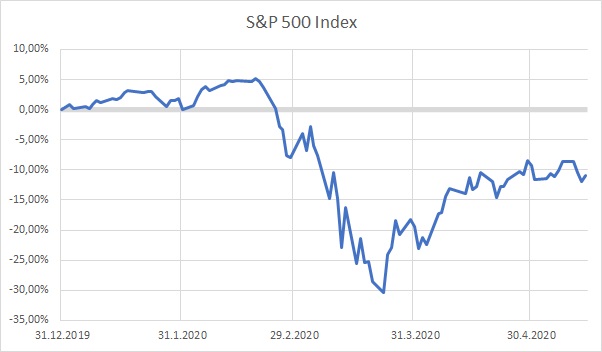

First, let’s look at the performance of the S&P 500 Index to see where we are at the current moment, and then we will move to equity factor strategies.

Updated performance of factor strategies

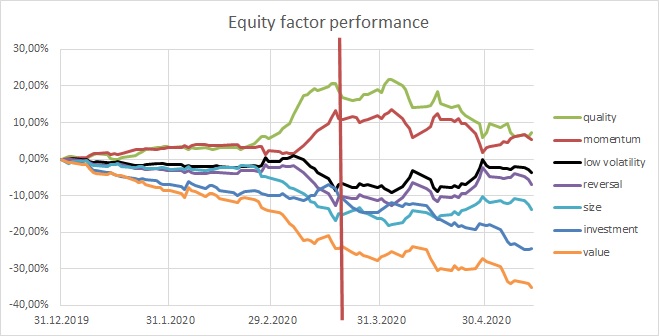

In our last analysis, we had shown two groups of factors: strong winners (quality and momentum) and a lot of bad losers (the rest of the factors). What’s the current status? Pretty grim.

Let’s see once again factor performance in one chart, and then we can look at each factor separately (the red vertical line is showing the day of our last article):

Among the winners still are:

Quality Factor – the quality factor lost almost all of its outperformance from the first quarter of 2020. It seems that lower-quality stocks outperformed during the current rebound. It’s probably not so surprising, as it usually happens during the very strong turnaround.

Momentum Factor – the momentum factor lost some of its profits, but can still be counted among winners. The underperformance of momentum factor during last two months can’t be called a crash, but it’s not surprising. We will here just repeat what we wrote in our previous article – most of the academic research papers related to equity momentum trading strategy show that this factor performs well at the beginning of crises. But momentum usually doesn’t perform well right as the market rebounds following previous large declines. Therefore, use some more sophisticated version of this strategy (see Three Methods to Fix Momentum Crashes).

And what are the losers?

Size Factor – tried to recover some lost ground, but was not very successful.

Low volatility – is still among the losers, but it recovered some of the loses.

Short-Term Reversal Factor – same story as the low volatility factor – recovered some ground but it’s still not enough to be the winner.

Investment Factor – continues to underperform, last two months were not kind to this factor.

Value Factor – poor value factor. The year 2020 will be among the years that will not be forgotten among value investors. We will not go into detail about what has happened to the value factor. There are more authors with higher expertise then we are. But we will just recommend you to read these perfect articles from Cliff Asness (Is Systematic Value Investing Dead), Wes Gray (Absolute Value Versus Relative Value) or Mikhail Samonov (Value Crashes: Deep History).

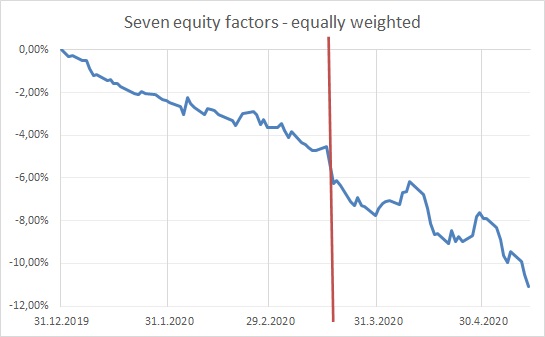

And what about the diversification among all seven factors?

OK, that’s not a pretty picture. It seems that traditional equity long-short factor strategies don’t have a good year. Maybe it’s a time for some non-traditional systematic factor strategies?

Are you looking for strategies applicable in bear markets? Check Quantpedia’s Bear Market Strategies

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend