Quantpedia in September 2025

Hello all,

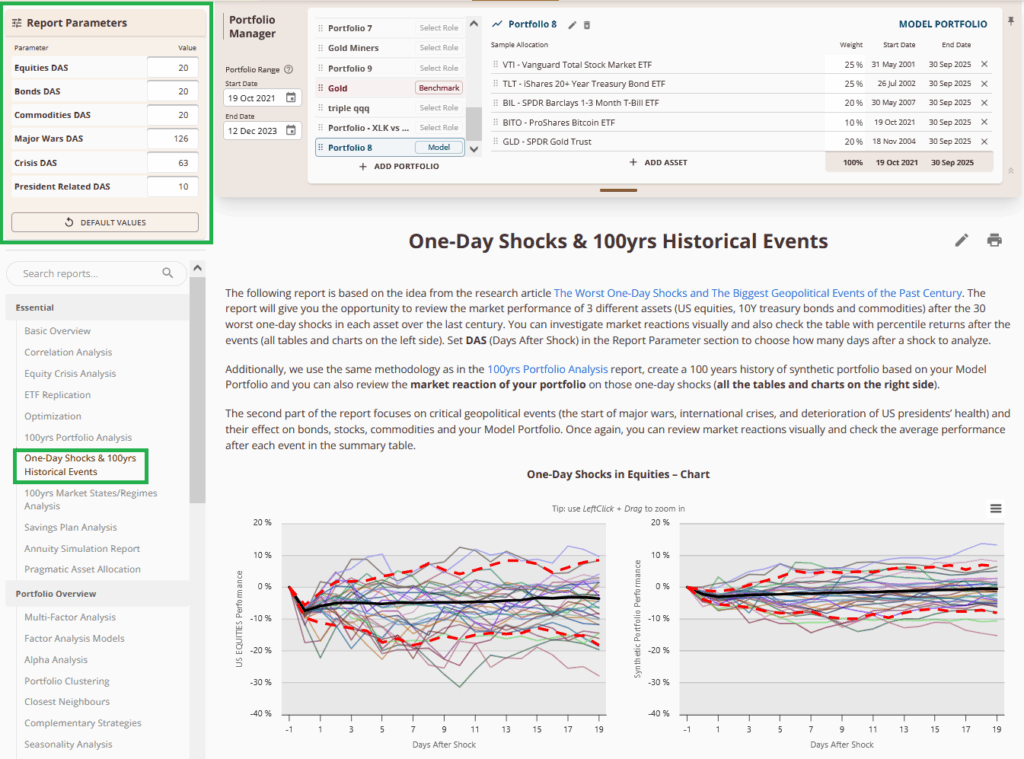

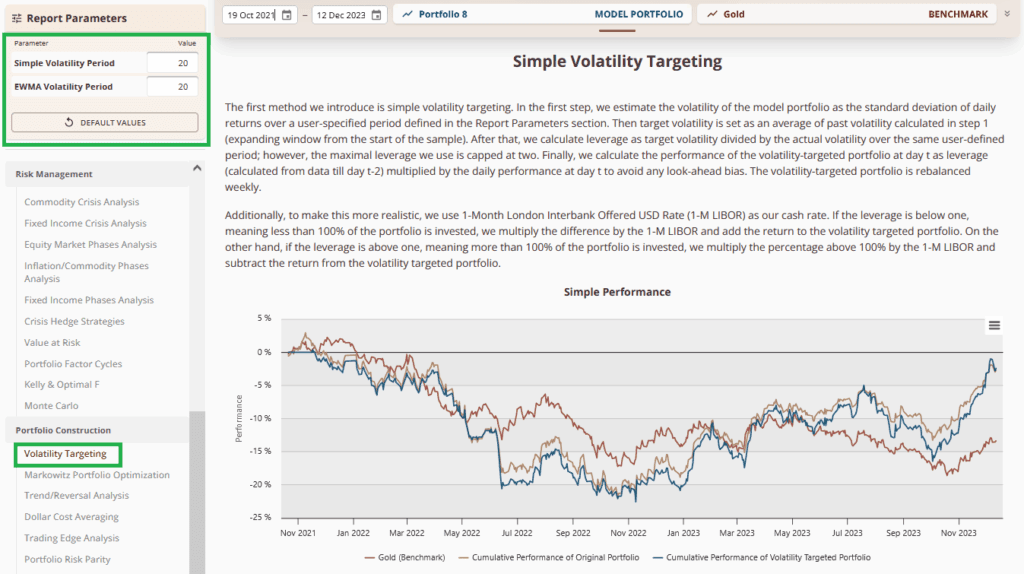

Firstly, as it is customary in this place, a new update to the Quantpedia Pro service. In September, we worked on two improvements in parallel. One of the priorities was to parametrize an additional four of our reports – One Day Shocks & 100yrs Historical Events, Volatility Targeting, Correlation Analysis, and Portfolio Rebalancing. In all reports, the goal was, as usual, to increase the flexibility and ease of use.

Our next priority was to upgrade the AI layer of the Screener (our chatbot/assistant). Over the last few months, we dug deeper into the new designs of AI assistants. We are finalizing the rework of the current version and are on track to get it live at the beginning of November. We are really looking forward to this improvement and the new capabilities it will offer…

Secondly, we would like to invite you to the webinar Unlocking the Power of Calendar and Seasonal Strategies, jointly organized by Quantpedia and Lightspeed Financial Services Group. We plan to discuss how the seasonal and calendar time-based return patterns work, their advantages and risks, methods for identifying and testing them, and how to combine seasonal strategies across asset classes for a diversified portfolio.

By the way, you can still open an account with at least $10,000 in equity using promo code QUANT25 and you will be entitled to the exclusive 12 FREE MONTHS of Quantpedia Premium subscription service (which normally costs $599).

And thirdly, let’s also quickly recapitulate Quantpedia Premium development:

- We had a bigger backlog of academic papers (a lot of them AI/ML related), which we have finally chewed through. Out of that, 20 new Quantpedia Premium strategies have been added to our database.

- 5 new related research papers have been included in existing Premium strategies during the last month

- 7 new backtests were written in QuantConnect code. Our database currently now contains over 850 strategies with out-of-sample backtests/codes.

Additionally, 5 new research articles were published on the Quantpedia blog in the previous month:

Gold’s Rally and the Gold Mining Stocks Trap

Authors: Dirk G. Baur, Lichoo Tay, and Allan Trench

Title: Gold Shares Underperform Gold Bullion

Hedging Tail Risk with Robust VIXY Models

Author: David Belobrad

Title: Hedging Tail Risk with Robust VIXY Models

Cross-Sectional and Dollar Components of Currency Risk Premia

Author: Vahid Rostamkhani

Title: Currency Risk Premia and (Many) Fundamentals Connected in the Long-run

Leveraged ETFs in Low-Volatility Environments

Author: Sona Beluska

Title: Leveraged ETFs in Low-Volatility Environments

What Drives the Excess Bond Premium?

Authors: Kevin Benson, et al.

Title: Understanding the Excess Bond Premium

Yours …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend