Currency Hedging with Currency Risk Factors

A new research paper related to multiple currency risk factors:

#5 – FX Carry Trade

#129 – Dollar Carry Trade

Authors: Opie, Riddiough

Title: Global Currency Hedging with Common Risk Factors

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3264531

Abstract:

We propose a novel method for dynamically hedging foreign exchange exposure in international equity and bond portfolios. The method exploits time-series predictability in currency returns that we find emerges from a forecastable component in currency factor returns. The hedging strategy outperforms leading alternative approaches out-of-sample across a large set of performance metrics. Moreover, we find that exploiting the predictability of currency returns via an independent currency portfolio delivers a high risk-adjusted return and provides superior diversification gains to global equity and bond investors relative to currency carry, value, and momentum investment strategies.

Notable quotations from the academic research paper:

"How should global investors manage their foreign exchange (FX) exposure? The classical approach to currency hedging via mean-variance optimization is theoretically appealing and encompasses both risk management and speculative hedging demands. However, this approach, when applied out of sample, suff ers from acute estimation error in currency return forecasts, which leads to poor hedging performance.

In this paper we devise a novel method for dynamically hedging FX exposure using mean-variance optimization, in which we predict currency returns using common currency risk factors.

Recent breakthroughs in international macro- nance have documented that the cross-section of currency returns can be explained as compensation for risk, in a linear two-factor model that includes dollar and carry currency factors. The dollar factor corresponds to the average return of a portfolio of currencies against the U.S. dollar, while the carry factor corresponds to the returns on the currency carry trade.

We take the perspective of a mean-variance U.S. investor who can invest in a portfolio of `G10' developed economies. We adopt the standard assumption that the investor has a predetermined long position in either foreign equities or bonds and desires to optimally manage the FX exposure using forward contracts. We form estimates of currency returns using a conditional version of the two-factor model where both factor returns and factor betas are time-varying.

A related literature provides strong empirical evidence, with underpinning theoretical support, that the dollar and carry factor returns are partly predictable. We exploit this predictability to forecast currency returns. Speci ffically, we estimate factor betas and 1-month ahead dollar and carry factor returns in the time series, and then form expected bilateral currency returns using these estimates. This vector of expected currency returns enters the mean-variance optimizer to produce optimal, currency-speci fic, hedge positions. We update the positions monthly and refer to the approach as Dynamic Currency Factor (DCF) hedging.

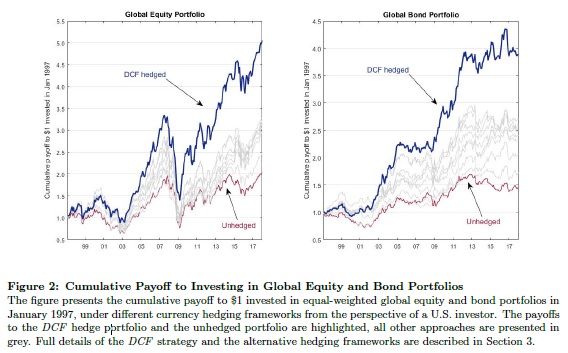

We evaluate the performance of DCF hedging, over a 20-year out-of-sample period, against nine leading alternative approaches ranging from naive solutions in which FX exposure is either fully hedged or never hedged, through to the most sophisticated techniques that also adopt mean-variance optimization. We nd DCF hedging generates systematically superior out-of-sample performance compared to all alternative approaches across a range of statistical and economic performance measures for both international equity and bond portfolios. As a preview, in Figure 2 we show the cumulative payoff to a $1 investment in international equity and bond portfolios in January 1997. When adopting DCF hedging, the $1 investment grows to over $5 by July 2017 for the global equity portfolio, and to almost $4 for the global bond portfolio. These values contrast with $2 and $1.5, which a U.S. investor would have obtained, if the FX exposure in the equity or bond portfolios was left unhedged."

Are you looking for more strategies to read about? Check http://quantpedia.com/Screener

Do you want to see an overview of our database of trading strategies? Check https://quantpedia.com/Chart

Do you want to know how we are searching new strategies? Check https://quantpedia.com/Home/How

Do you want to know more about us? Check http://quantpedia.com/Home/About

Follow us on:

Facebook: https://www.facebook.com/quantpedia/

Twitter: https://twitter.com/quantpedia