Five Small Shards of Insight Hidden in Data

Around a month ago, we launched a series of short videos called “Quantpedia Explains“, in which we plan to show and explain some of the themes out of quantitative finance that we think are worth mentioning. We have started with a quick intro to individual Quantpedia Pro reports, and now, we have expanded our content with a series of short case study articles. Each article uses one Quantpedia Pro report to generate a quick market/portfolio insight, and this blog post will give you a short recapitulation of the first five studies.

Insight nbr.1:

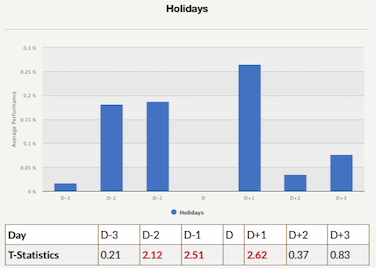

In our first, seasonal case study, we verified a few ideas out the academic research related to seasonality in the stock market (Turn of the Month effect described in “Xu, McConnell: Equity Returns at the Turn of the Month“, FED day effect described in “Tori: Federal Open Market Committee meetings and stock market performance“, etc.). We are often proponents of using academic research as an inspiration to translate a trading idea from one asset class to another. We used this opportunity to analyze the seasonal behaviour of Gold and shown that it displays a strong seasonal tendency in returns in days around US public holidays (which is not widely known).

Insight nbr. 2:

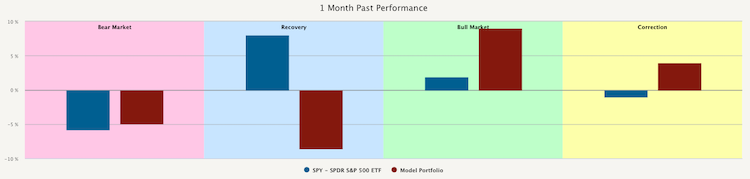

In the Market Phases Analysis case study, we devoted our time to studying how Bitcoin performs during various phases of the market cycle. Some cryptocurrency proponents advocate that Bitcoin can be used as a store of value, mainly during the economic and financial crisis. In the past, we have written a blog post where we argued that it is not necessarily the case as the performance of Bitcoin is usually the worst during the same time as stock market experiences the bear market. The following figure shows the 1 month past performance of SPY (blue bars) and Bitcoin (red bars).

Insight nbr. 3:

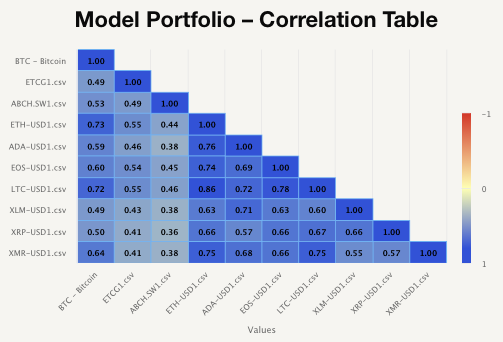

The third case study is related to the Correlation Analysis report, which can be used to analyze any model portfolio. We examined how are cryptocurrencies correlated to other assets and how does the correlation evolved over time. The resulting outcome is that cryptocurrency market correlation slowly increases, and we can’t rule out the financialization of the crypto market (the same process that happened in commodities approximately ten years ago).

Insight nbr. 4:

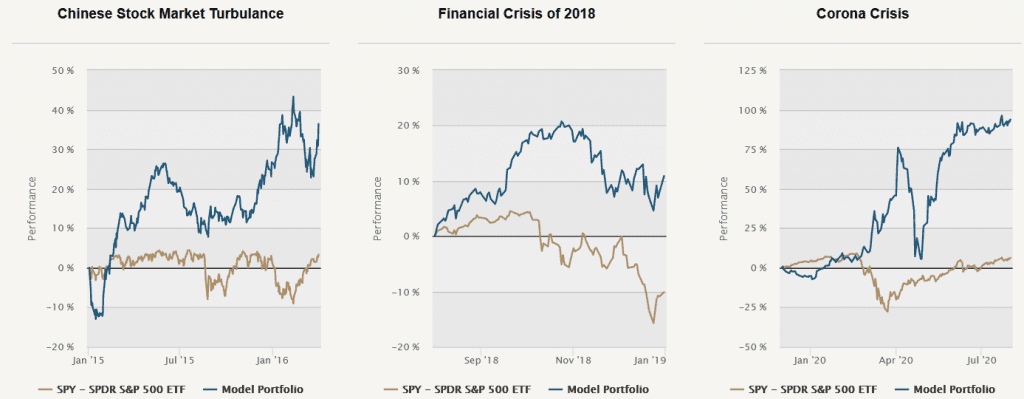

The fourth case study explores the Crisis Analysis report, which we used to analyze the behaviour of three different model portfolios during multiple short-term and long-term crisis periods. The case study confirmed that skewness-based trading strategies could serve as a practical hedge/diversification during stock market drawdowns (as we also described in our older article).

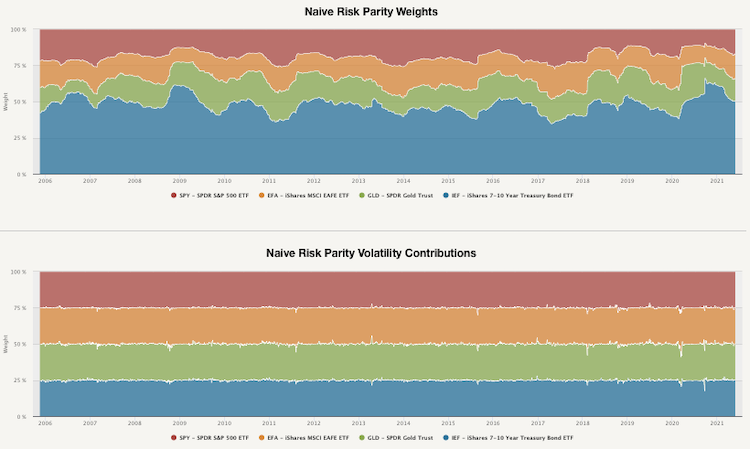

Insight nbr. 5:

The fifth case study shows how to apply the Naive Risk Parity method to the model portfolio that consists of four ETFs. It shows the main attribute of most of the risk parity portfolios – lower total returns but significantly lower risk measures.

Interested? Then subscribe to Quantpedia Pro and try how our analytics and reporting significantly saves time spent on quantitative research.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend