Quantpedia Highlights in September 2021

Hello all,

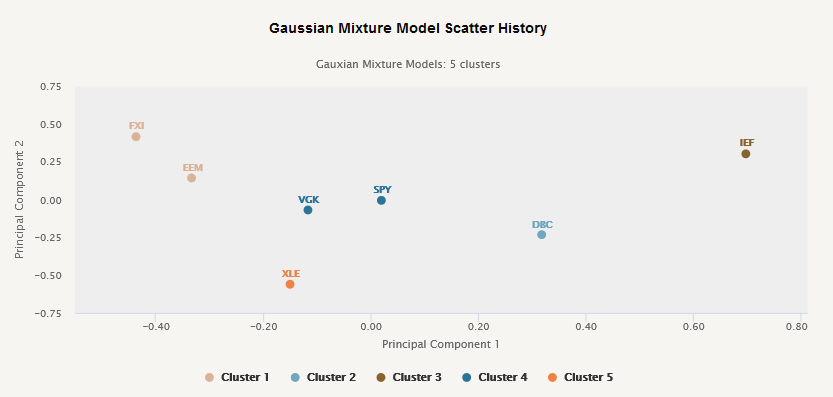

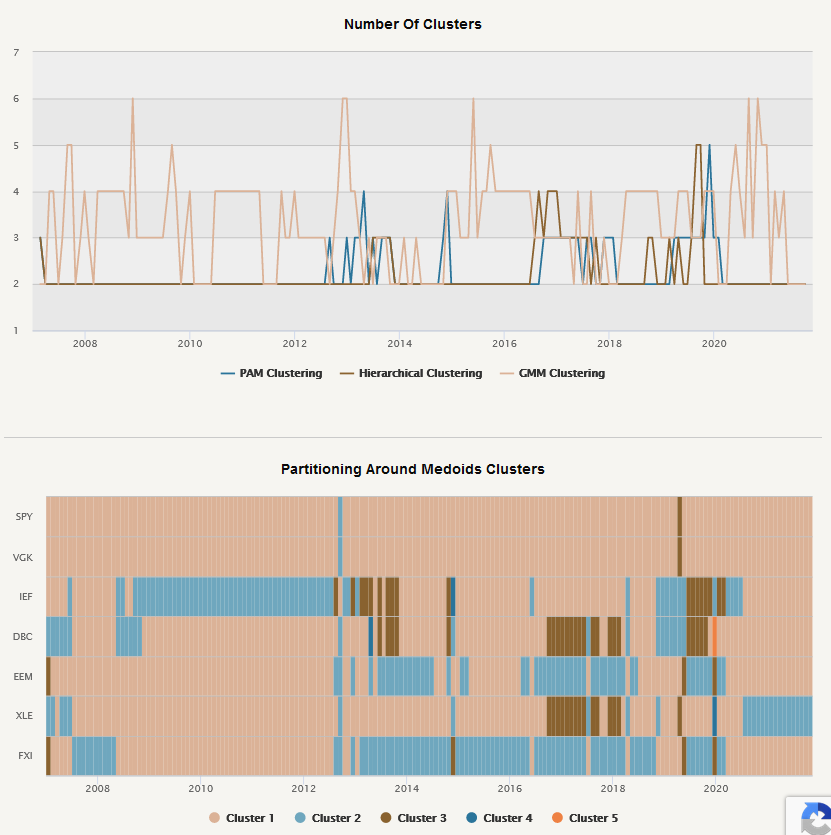

As we have promised, the new report related to clustering methods is now available for Quantpedia Pro clients. It allows to analyze the clustering of the custom model portfolio and observe clusters based on Partitioning Around Medoids (PAM), Hierarchical Clustering, and Gaussian Mixture Model. Complete methodology for all three methods is available in the following article and its 2nd and 3rd continuation.

You can review clusters for various periods (actual 12-months period and the longest available period).

Additionally, you can compare how many clusters are identified in your model portfolio by all three clustering methods. Plus, you can investigate which assets belonged to which cluster over time (in all three methods).

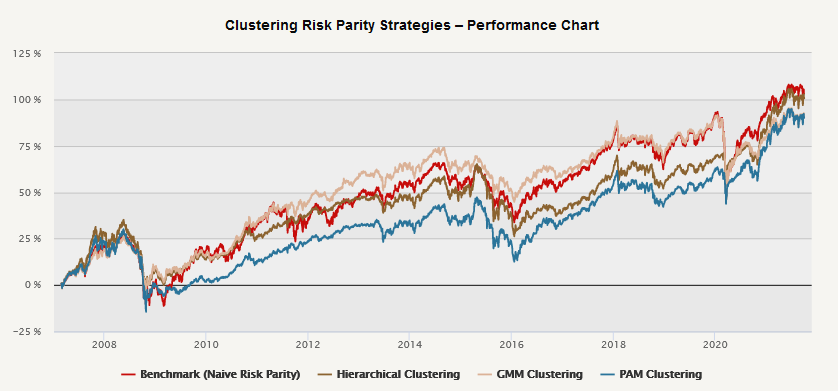

In the end, you can review three Cluster Risk Parity Trading strategies and compare their performance to the naive Risk Parity benchmark. Three Cluster Risk Parity strategies create optimal clusters and then weigh the assets inside the cluster and the clusters between themselves proportionately to the inverse of their volatility, i.e. according to Naïve risk parity. The optimal number of clusters is determined using the silhouette method and portfolio is rebalanced on a monthly basis.

Let’s also quickly recapitulate Quantpedia Premium development:

- 13 new Quantpedia Premium strategies have been added to our database

- 10 new related research papers have been included in existing Premium strategies during the last month

- 10 new backtests were written in QuantConnect code. Our database currently contains over 480 strategies with out-of-sample backtests/codes.

Additionally, apart from our series or articles related to clustering methods, 5 new articles were published on the Quantpedia blog in the previous month.

Asset Pricing Models in China

Authors: Matthias X. Hanauer, Maarten Jansen, Laurens Swinkels and Weili Zhou

Title: Factor models for Chinese A-shares

Community Alpha of QuantConnect – Part 3: Adjusted Social Trading Factor Strategies

Author: Matus Padysak

Title: Community Alpha of QuantConnect – Part 3: Adjusted Social Trading Factor Strategies

Does Gambling Influence Stock Markets Around the World?

Authors: Alok Kumar, Huong Nguyen, and Talis J. Putnins

Title: Only Gamble in Town: Market Gambling Around the World and Market Efficiency

How to Use Lexical Density of Company Filings

Authors: Hanicova, Kalus, Vojtko

Title: How to Use Lexical Density of Company Filings

A New Return Asymmetry Investment Factor in Commodity Futures

Authors: Durian, Padysak

Title: A New Return Asymmetry Investment Factor in Commodity Futures

Stay safe …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend