Quantpedia in January 2026

Hello all,

The wheel of the time doesn’t stop, and as usual, we have a batch of new updates for you.

Firstly, let’s go through the Quantpedia Pro update.

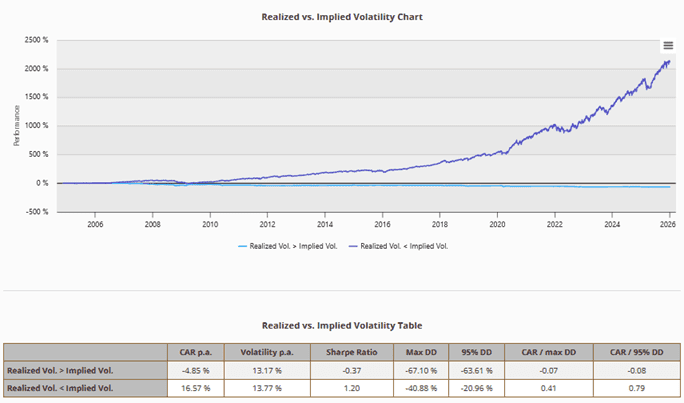

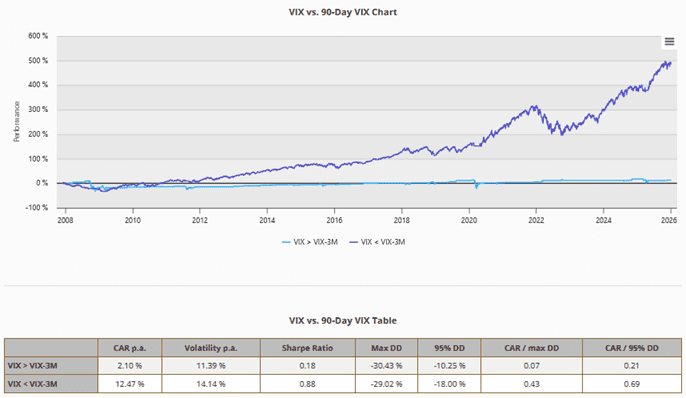

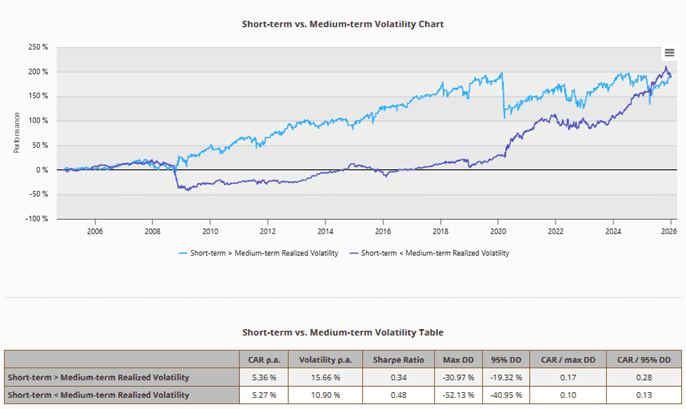

Volatility regimes play a crucial role in shaping the behavior of individual assets as well as quantitative trading strategies. To help investors better understand this relationship, we have extended the Trading Edge Analysis Report with three new volatility-based regime filters: equity realized vs. equity implied volatility, equity short-term implied vs. equity mid-term implied volatility, and model portfolio short-term vs. model portfolio medium-term realized volatility. These filters automatically split market conditions into distinct volatility environments and show how a model portfolio performs in each of them, making it easy to assess strategy sensitivity to volatility expansion, contraction, and risk perception. All three filters, including equity curves and performance tables, are now available directly within the Trading Edge Analysis Report.

Secondly, we would like to invite you to watch the 7th episode of our YouTube video series QuantBeats. Building conviction without emotion is harder than it sounds, and David Kaiser from Methodical Investments walks us through his evolution from fundamental analyst to quant value investor, explaining how rules-based portfolios, fundamental data, and patience help investors survive long periods when value is out of favor.

Listen to this newest Quantbeats episode, and we also sincerely invite you all to follow us on our YouTube, Linkedin, FB, Twitter, and/or Bluesky links.

Thirdly, we have a great announcement for you! The Quantpedia Awards Competition Is Back!

For a quick recapitulation, our Quantpedia Awards 2026 aims to be the premier competition for all quantitative trading researchers. If you have an idea in your head about systematic/quantitative trading or investment strategy, and you would like to gain visibility on the professional scene, then submit your research paper, and you can compete for an attractive list of prizes. All info about the prizes, submission process, expert committee, and our partners are described in detail on our dedicated subpage. There is still a lot of time until the end of the submission deadline, but time flies very fast, and the end of April is here very soon. So do not forget to join our race for a $25.000 prize pool!

And finally, let’s also quickly recapitulate Quantpedia Premium development:

- 11 new Quantpedia Premium strategies have been added to our database.

- 8 new related research papers have been included in existing Premium strategies during the last month

- 9 new backtests were written in QuantConnect code. Our database currently now contains over 880 strategies with out-of-sample backtests/codes.

Additionally, 5 new research articles were published on the Quantpedia blog in the previous month:

The Fallacy of Concentration Risk

Authors: Mark Kritzman and David Turkington

Title: The Fallacy of Concentration Risk

Is The Optimal Long-term Portfolio Share of Bitcoin Negative?

Author: Alistair Milne

Title: The Optimal Long-term Portfolio Share of Bitcoin is Negative (or Zero)

Who Is the Counterparty to the Pro-Cyclical Investors

Authors: Johannes Beutel, Maik Schmeling, and Willy Scherrieble

Title: Who clears the market when pro-cyclical investors trade?

Do S&P500 0DTEs Options Increase Market Volatility?

Authors: Greg Adams et al.

Title: Do S&P500 Options Increase Market Volatility? Evidence from 0DTEs

Pragmatic Asset Allocation Across Market Cycles

Author: David Mesíček

Title: Pragmatic Asset Allocation Across Market Cycles

Yours …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend