Quantpedia in October 2023

Welcome to our October’s recap blog post!

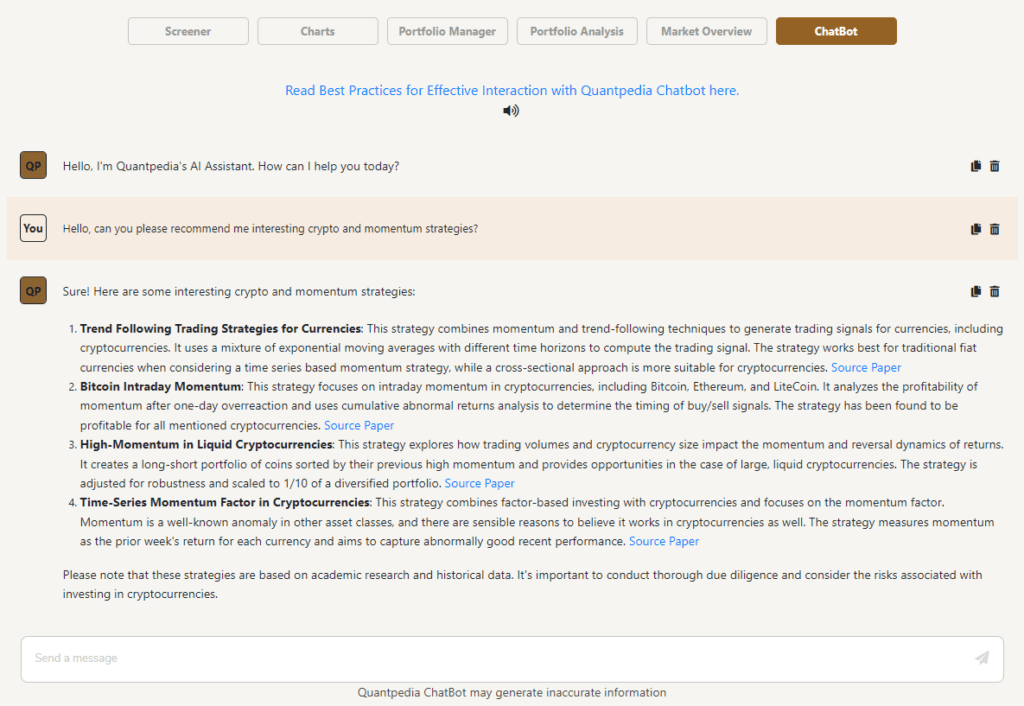

We at Quantpedia are actively monitoring the latest advancements in the field of artificial intelligence and its potential applications in quantitative finance and trading. We are exploring this topic regularly, and here are just a few articles from the last few months – Hello ChatGPT, Can You Backtest Strategy for Me?, An Introduction to Machine Learning Research Related to Quantitative Trading, or Top Models for Natural Language Understanding (NLU) Usage. Internally, we are conducting rigorous testing of various approaches to incorporate this technology into Quantpedia. In the upcoming months, we will gradually introduce new features stemming from these efforts. Today, we are excited to unveil our first such experimental feature – the Quantpedia chatbot for Quantpedia Pro users, which has been trained on our extensive database of Quantpedia strategies. The chatbot can serve as a quick assistant if you want to orientate in our database. It can recommend new strategies and academic papers of interest or converse about the trading rules or performance.

This is our initial practical feature that cradled out from the experimentation with AI technology, but it’s not the last… There are some other projects under the hood, so stay tuned 😉

Let’s also quickly recapitulate Quantpedia Premium development:

- 12 new Quantpedia Premium strategies have been added to our database

- 11 new related research papers have been included in existing Premium strategies during the last month

- 7 new backtests were written in QuantConnect code. Our database currently now contains nearly 720 strategies with out-of-sample backtests/codes.

Additionally, 6 new articles were published on the Quantpedia blog in the previous month:

Time Invariant Portfolio Protection

Authors: Gianluca Baglini, Tony Berrada

Title: Time Invariant Portfolio Protection

What’s the Key Factor Behind the Variation in Anomaly Returns?

Authors: Andrea Tamoni and Stanislav Sokolinski and Yizhang Li

Title: Which Investors Drive Anomaly Returns and How?

Hello ChatGPT, Can You Backtest Strategy for Me?

Authors: Cyril Dujava

Title: Hello ChatGPT, Can You Backtest Strategy for Me?

Which Alternative Risk Premia Strategies Works as Diversifiers?

Authors: Antti Suhonen and Kari Vatanen

Title: Does Alternative Risk Premia Diversify? New Evidence for the Post-Pandemic Era

Estimating Stocks-Bonds Correlation from Long-Term Data

Authors: Roderick Molenaar, Edouard Senechal, Laurens Swinkels, Zhenping Wang

Title: Empirical evidence on the stock-bond correlation

Is It Good to Be Bad? – The Quest for Understanding Sin vs. ESG Investing

Authors: Margareta Pauchlyova, Radovan Vojtko

Title: Is It Good to Be Bad? – The Quest for Understanding Sin vs. ESG Investing

Yours …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend