Quantpedia in September 2022

Hello all,

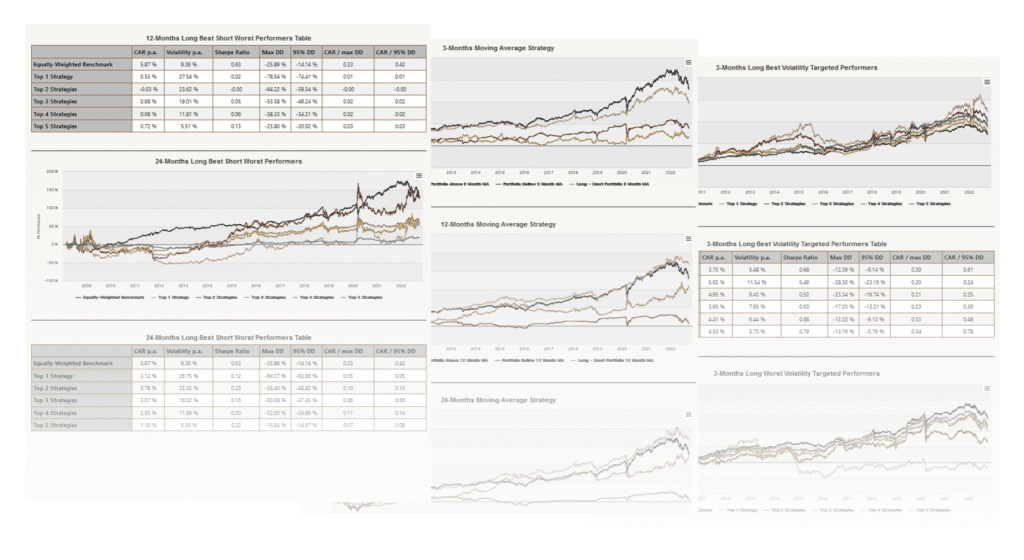

We continue with the automatization of repetitive portfolio management tasks (as we did in August with the Trading Edge report); therefore, we spent September building three new Quantpedia Pro reports that help to accelerate multi-strategy research – Cross-Sectional Momentum Management, Time-Series Moving Average Management, and Cross-Asset Volatility Targeting. As always, users can select any combination of ETFs, custom equity curves, and Quantpedia Premium strategies in the Portfolio Manager section and then look for new strategy allocation overlays.

A Cross-Sectional Momentum Management report applies momentum and contrarian strategy overlay signals based on the performance of the underlying. Suppose the user picks a list of ETFs as his model portfolio. In that case, he can easily automatically recreate and test cross-sectional momentum strategies in the spirit of popular momentum asset allocation or sector rotation academic papers. Or he can select a list of trading strategies as underlying and test factor momentum overlays.

Time-Series Moving Average Management report applies trend and contrarian strategy overlays in the time-series fashion. So if a user selects multiple ETFs as underlying, he can look for new CTA-like strategies or asset class trend-following systems. Or he can again test these rules on a list of individual strategies as overlays.

The last new report, Cross-Asset Volatility Targeting, is similar to the Cross-Sectional Momentum Management report, but we decided to apply the volatility adjustment/targeting because of the possibility of significant differences between the volatilities of our underlying strategies (or ETFs) selected in the Portfolio Manager. Equalizing the volatility contributions allows for the same chances for all strategies (ETFs) to appear in the top/bottom portfolio based on their performance.

The detailed methodology for all three reports is explained in the following article – Multi Strategy Management for Your Portfolio.

Let’s also quickly recapitulate Quantpedia Premium development:

- 9 new Quantpedia Premium strategies have been added to our database

- 13 new related research papers have been included in existing Premium strategies during the last month

- 9 new backtests were written in QuantConnect code. Our database currently contains over 600 strategies with out-of-sample backtests/codes.

Additionally, 5x new analysis of academic research papers were published on the Quantpedia blog in the previous month:

A Study on How Algorithmic Traders Earn Money

Authors: Ricky Cooper, Wendy Currie, Jonathan Seddon, and Ben Van Vliet

Title: Competitive Advantage in Algorithmic Trading: A Behavioral Innovation Economics Approach

Investing in Deflation, Inflation, and Stagflation Regimes

Authors: Guido Baltussen, Laurens Swinkels, and Pim van Vliet

Title: Investing in Deflation, Inflation, and Stagflation Regimes

How Common is Insider Trading? Evidence from the Options Market

Authors: Oleg Bondarenko and Dmitriy Muravyev

Title: A Tale of How Common is Insider Trading? Evidence from the Options Market

Overnight Sentiment and the Intraday Return Dynamics

Authors: Baoqing Gan, Vitali Alexeev, and Danny Yeung

Title: Moods on the Move: Overnight Sentiment and the Intraday Return Dynamics

The Hidden Costs of Corporate Bond ETFs

Author: Christopher Reilly

Title: The Hidden Cost of Corporate Bond ETFs

Yours …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend